Brain Tumor Diagnosis and Treatment Market Industry Outlook

Health |

2026-05-27 07:01:59

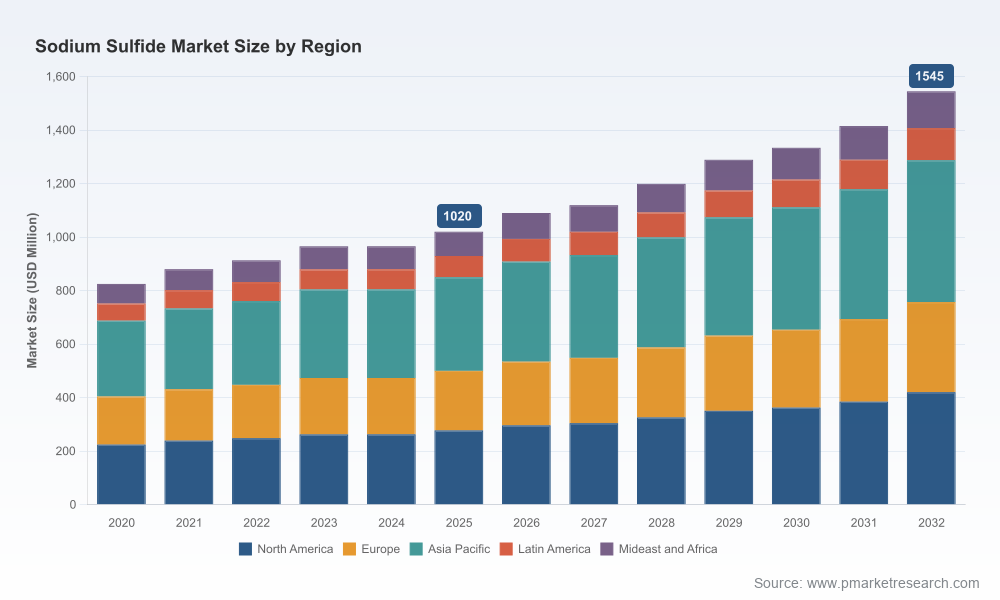

As global value chains normalize after recent supply disruptions, sodium sulfide is re-emerging as a small but strategically important industrial chemical. Our 2026-focused briefing synthesizes macro trajectories, supplier dynamics, regulatory inflection points and pragmatic plays that will determine winners over the next planning cycle. Drawing on PW Consulting’s market model (base year 2025, historical 2020–2025, forecast 2026–2032), the global sodium sulfide market is projected to expand at a compound annual growth rate (CAGR) of 5.75% — moving from a base of roughly USD 1,020 Million in 2025 toward the mid‑to‑high single‑digit growth outcomes embedded in our 2032 projection. This paper highlights the strategic value of that intelligence for corporate decision-making in 2026 while deliberately preserving detailed segment-level figures to encourage staged access to the full study.

Sodium Sulfide Market

Supply volatility and feedstock constraints. Two interlinked forces — feedstock availability (notably sulfur and caustic soda) and regionally asymmetric refinery outputs — are shaping production economics. Recent policy moves and trade restrictions have amplified these sensitivities, making 2026 the first year when many firms will need to operationalize their response plans.

Sodium Sulfide Market

Regulatory tightening. Several jurisdictions have updated screening assessments and hazardous‑substance rules for alkali sulfides. Compliance obligations are becoming more prescriptive around maximum concentrations, storage, transport and waste treatment — moving sodium sulfide from a commodity chemical toward a regulated specialty product in some markets.

Sodium Sulfide Market

Product differentiation pressure. End markets are demanding cleaner, low‑dust and higher‑purity grades (including battery‑grade and prilled variants) that require capital investment and process upgrades. The pace at which firms can introduce differentiated SKUs will determine margin expansion through 2028 and beyond.

At the macro level, our model shows steady growth underpinned by traditional end‑use demand (pulp & paper, leather and detergent/pulp segments) alongside emerging smaller but higher‑value applications (advanced chemicals and battery materials). The overall market size in our model climbs from about USD 1,020 Million in 2025 to just over USD 1,545 Million by 2032, reflecting the 5.75% CAGR. This top‑line movement masks important structural change: mature downstream segments will remain core demand anchors while pockets of premium demand provide the most attractive margin expansion opportunities for producers that can certify and scale higher‑purity production.

Feedstock cost dynamics — sulfur and caustic soda: Production economics are sensitive to sulfur supply derived from refinery streams and merchant sulfur markets. Trade controls and export policies in major producing countries have episodically tightened availability, raising input cost volatility and incentivizing hedging strategies or backward integration.

Regulatory and environmental compliance: National screening assessments and hazardous chemical frameworks are tightening. Operators should expect more stringent limits on handling concentrations, documentation requirements and liabilities for off‑site impacts, which will raise compliance CAPEX and OPEX.

Infrastructure and logistics: Sodium sulfide’s hazardous classification increases logistics complexity and cost. Companies with optimized storage, specialist transport contracts and robust emergency response planning will realize lower total delivered cost and fewer operational interruptions.

Demand-side resilience: Core demand from long‑standing applications remains, but end‑market cyclicality (e.g., pulp & paper capex cycles and leather industry dynamics) requires flexible supply arrangements and contractual structures to smooth utilization.

The sodium sulfide space displays a concentrated supplier structure at the global level, with the largest three commercial groups controlling a substantial share and the top five approaching eight in ten units of market concentration. This concentration profile has strategic consequences: price leadership, differentiated product roll‑outs and selective capacity expansion are concentrated in the hands of a few vertically integrated suppliers and regional champions.

Nouryon (Amsterdam, Netherlands) — A specialty chemicals player with an established footprint in sodium sulfide flakes, Nouryon has been moving toward higher‑grade offerings. Recent investment to establish battery‑grade production under clean‑room conditions signals a strategic pivot toward premium applications and tighter supply control.

Solvay (Brussels, Belgium) — Longstanding supplier of alkali sulfides with diversified end‑use exposure. Their commissioning of an automated low‑dust prill line (Rosignano) indicates a push to reduce logistics costs and expand marketable grades that meet stricter handling standards.

American Elements (Los Angeles, United States) — Positions on high‑purity, research and advanced‑application supply, serving laboratories and specialty industrial customers where certification and form factor (powder, flakes, hydrates) matter.

Gujarat Alkalies and Chemicals Ltd (Vadodara, India) — Industrial‑grade supply with established channels into pulp, dyes and heavy chemicals; represents the classic regional supplier model with cost‑competitive positioning.

Shaanxi Fuhua and Shandong Aojin (China) — High‑capacity regional manufacturers with production scale geared to textiles, leather and chemical processing; represent the supply cushion to global markets and sources of price downward pressure in spot markets.

Kishida and Nagao (Japan) — Niche suppliers offering high‑purity and specialty forms for reagent, laboratory and some battery precursor markets; attractive partners for co‑development in advanced value chains.

Capacity expansions in Asia by multinational and regional players point to strategic intent to lock in downstream contracts and capture incremental demand recovery in pulp, paper and textiles.

Automated prill lines and clean‑room battery‑grade facilities suggest that manufacturing CAPEX is shifting from purely volumetric expansions to quality and safety upgrades that command price premiums.

For C‑suite and commercial leaders preparing 2026 budgets and three‑year plans, the following strategic themes should guide decision making:

Feedstock resilience and procurement sophistication: Move beyond single‑source buying. Deploy multi‑tier supplier pools, long‑dated index‑linked contracts and consider upstream partnerships or minority investments in sulfur suppliers where economically feasible.

Product and process differentiation: Invest selectively in low‑dust prilling, high‑purity processing and packaging innovations that lower logistic friction and unlock new buyer segments (e.g., battery precursors, specialty reagents).

Regulatory and ESG operationalization: Treat compliance as a value driver. Proactive investments in safer storage, waste neutralization and community engagement reduce risk premiums on asset deployment and can speed permitting for expansions.

Selective M&A and JV approaches: Market concentration means strategic acquisitions — particularly in regional supply hubs — can be accretive quickly. Look for targets that bring product form, logistics capabilities or regulatory approvals that are hard to replicate.

Commercial contracting sophistication: Use hybrid contracts that blend take‑or‑pay, flex options and quality premiums to balance utilization and margin risks across cycles.

The comprehensive PW Consulting study provides a buyer‑and‑seller oriented toolkit designed for operational execution in 2026. Highlights include:

Top‑line forecasting and scenario models (base 2025, forecast 2026–2032) with sensitivity testing on feedstock pricing and regulatory shocks.

Supplier capability matrices and technology readiness assessments to prioritize capital deployment.

Regulatory tracker and compliance heatmaps for key markets, including updated screening assessments and transport/storage mandates.

Commercial playbooks: contracting templates, margin stress tests and go‑to market recommendations for launching premium grades.

Risk register and mitigation roadmaps covering logistics, feedstock, permitting and reputational scenarios.

Note: the full report contains granular segmentation and regional/applications breakdowns that are intentionally omitted from this preview. Those detailed splits and raw numerical tables are accessible in the full study for clients and registered users.

Run a procurement stress test: model your FY26 exposure to sulfur and caustic price shifts and identify minimum hedging or contracting actions to limit margin erosion.

Audit product portfolio: nominate one SKU for quality upgrade (e.g., low‑dust prills or battery‑grade) and scope CAPEX needs and payback under conservative demand scenarios.

Regulatory gap assessment: establish a cross‑functional task force to validate storage, transport and disposal practices against the newest screening assessments in your operating jurisdictions.

Pursue partnership scouting: identify 2–3 suppliers or technology partners for JV or off‑take discussions focused on feedstock assurance or high‑purity production.

For executive teams, the sodium sulfide market offers a classical consultative paradox: a modest absolute market size but outsized strategic implications, because feedstock volatility, regulatory shifts and product differentiation interact to compress or expand supplier margins rapidly. Our 2026‑centered analysis equips leaders with the top‑line growth trajectory (CAGR 5.75% to 2032) and the implementation playbook required to convert forecasted volume growth into sustained margin improvement. Firms that move early on feedstock resilience, regulatory compliance and product premiumization will capture disproportionate value in this concentrated market.

PW Consulting’s full Sodium Sulfide Market report contains the detailed regional and application segmentations, supplier scorecards, and executable templates referenced in this preview. To obtain the complete dataset, scenario files and tailored advisory options for 2026 planning, visit our research portal or contact our industry team for a confidential briefing.

For detailed analysis of this topic, please visit the official page:Sodium Sulfide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com