NBPT Market 2026 Strategic Outlook: A PW Consulting Brief

Executive snapshot — why this study matters for 2026 decisions

As companies prepare budgets and strategic roadmaps for 2026, N-(n-butyl) thiophosphoric triamide (NBPT) sits at an inflection point between steady commercial demand and accelerating regulatory and technological change. Our market model — built on a 2025 base year and a historical run from 2020–2025, with a forecast horizon to 2032 — shows a resilient market trajectory with a compound annual growth rate of approximately 4.23% across the forecast period. PW Consulting’s topline projection traces the market from the early‑decade baseline through the 2025 checkpoint and on to a materially larger market in the early 2030s, providing a quantified envelope for capacity planning, pricing strategy, and M&A prioritization.

N-(n-butyl) Thiophosphoric Triamide (NBPT) Market

Structural characteristics matter: the NBPT market exhibits moderate concentration, with the three largest suppliers commanding a notable share of industry volumes and the top five firms consolidating a dominant proportion of capacity. For 2026, this translates into a market where supply‑side moves — new plant capacity, capacity reallocation, or distributor agreements — can quickly reshape local pricing and availability. Decision‑makers who align procurement, product development, and regulatory readiness to these structural realities will preserve optionality and reduce execution risk.

N-(n-butyl) Thiophosphoric Triamide (NBPT) Market

What the PW Consulting NBPT Market Study delivers (practical, execution‑oriented)

- Transparent market sizing and growth drivers: validated historical series (2020–2025) and a granular forecast through 2032, with scenario variants and sensitivity testing to raw material and policy shocks.

- Demand archetypes and commercial use cases: differentiated buyer profiles (fertilizer reformulators, formulators, distributors, and niche industrial users), with purchase triggers, contract structures, and recommended margin mechanics for each archetype.

- Pricing & cost‑to‑serve playbook: input cost mapping, pricing elasticity estimates, and negotiation levers for procurement teams and commercial managers.

- Supply‑chain mapping and resilience analysis: producer and distributor footprints, logistics chokepoints, dual‑sourcing templates, and inventory policy recommendations for 2026 disruptions.

- Regulatory & standards tracker: implications of TSCA listings, draft standards (e.g., standards addressing urease inhibitors), and patent activity for product adoption and labeling requirements.

- Competitive intelligence & supplier scorecards: verified profiles, capability matrices, and strategic intent assessments for active market players.

- M&A and partnership target shortlists: screened candidates by strategic fit, geography, and technology, with integrated valuation sensitivities.

- Implementation toolkit: executive dashboards, negotiation scripts, procurement RFP templates, and 90‑day tactical checklists to convert strategy into measurable outcomes in 2026.

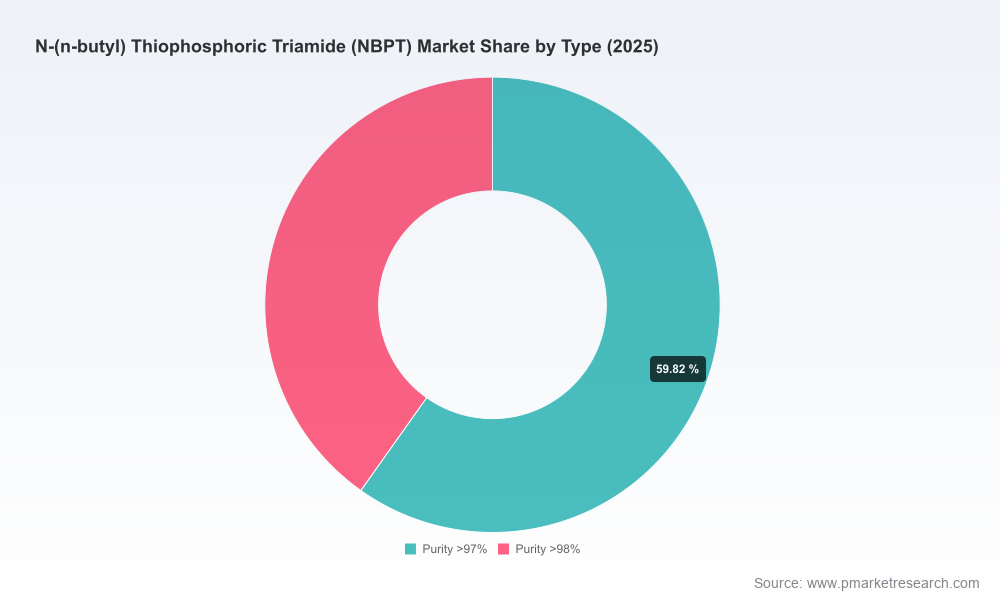

To maintain this brief’s role as a strategic teaser, the report intentionally withholds detailed sub‑segment tables and regional/application split tables — those granular data and supplier scorecards are available in the full study.

N-(n-butyl) Thiophosphoric Triamide (NBPT) Market

Market dynamics shaping strategy in 2026

Several converging dynamics will influence competitive outcomes for NBPT in 2026:

- Performance economics: demand continues to be driven by the value proposition of NBPT as a urease inhibitor—improving nitrogen efficiency, reducing ammonia volatilization, and enabling higher fertilizer ROI for farmers and formulators. This keeps total addressable demand stable and growing.

- Regulatory and standards momentum: NBPT’s listing on inventories and evolving standards for urease inhibitors are lowering barriers in some markets while raising compliance requirements in others. Draft standards and patent activity are shaping formulation requirements and inspection expectations for industrial and agricultural products.

- Supply‑side geography and channel dynamics: a mix of North American suppliers, global distributors, and Chinese technical manufacturers creates differentiated value chains — from bulk active producers to formulators who deliver finished agrochemical additives. Trade and logistics trends, especially for formulated products and intermediate chemicals, will influence lead times and working capital needs.

- Intellectual property and product innovation: new patents filed on urea compositions and application methods affect route‑to‑market choices. Firms that pair formulation know‑how with regulatory compliance enjoy a commercial moat that can be monetized through licensing or premium pricing.

- Market concentration: with the top three and five players holding a meaningful share of capacity, strategic alliance formation, distribution exclusivity, or targeted bolt‑on acquisitions are powerful levers to secure market access and control localized price dynamics.

Competitive landscape — who to watch and why

In 2026, a small set of active suppliers and specialists will continue to define go‑to‑market dynamics:

- Silver Fern Chemical (United States): positions itself as a bulk supplier with a dedicated commercial focus on agricultural and industrial urease inhibition applications. Their visible trade show presence underscores an ambitions to deepen commercial relationships in premium markets.

- Valudor Products, LLC (United States): a supplier/formulator with an emphasis on compliance and product integration for fertilizer additives — a profile attractive to customers prioritizing regulatory certainty and formulated finished goods.

- Wego Chemical Group (United States/global reach): serves as a distribution and supply‑chain solutions partner, enabling international market access for producers without in‑market infrastructure — a critical intermediary for downstream players expanding across regions.

- Shangyu Sunfit Chemical Co., Ltd. and AVF Chemical (China): active technical‑grade manufacturers that underpin global supply, particularly for formulators and OEMs that source active ingredients in bulk. Their cost and scale economics matter to buyers seeking competitive input prices.

Recent industry moves — exhibitor activity by leading suppliers, updated safety‑datasheet filings confirming regulatory listings, and new product literature announcing NBPT‑containing stabilizers — signal an industry in market development mode: consolidating regulatory clarity, validating product claims, and building route‑to‑market infrastructure ahead of broader adoption cycles.

2026 decision playbook — concrete priorities for executive teams

Leaders who treat 2026 as a year to lock in structural advantage should focus on a tightly sequenced set of initiatives:

- Immediate (0–6 months)

- Secure conditional second‑source agreements for key raw materials and active NBPT supplies; include force‑majeure and volume flex provisions to limit exposure to supplier concentration.

- Run a regulatory gap assessment mapped to planned markets and products — confirm TSCA, local inventories, and draft standards compliance before scaling production or distribution.

- Pilot formulation trials with at least two NBPT purity tiers to test margin sensitivity and customer willingness to pay for differentiated performance.

- Medium term (6–18 months)

- Pursue targeted partnerships with formulators or distributors who offer on‑the‑ground channels in priority markets; prioritize partners with traceable compliance and product stewardship capabilities.

- Invest in product claim substantiation — field trials, agronomic partnerships, and third‑party validations — to support premium pricing and label claims.

- Conduct focused M&A diligence on bolt‑on producers or formulation specialists that can accelerate market access or improve margin capture.

- Strategic (18–36 months)

- Design a vertically integrated play where economics justify — consider integrating formulation, packaging, and localized distribution to capture downstream value.

- Develop IP strategy aligned with evolving patents in urea formulation methods; consider licensing, cross‑licensing, or defensive patenting where appropriate.

Risk matrix and contingency guidance

Key downside and upside scenarios for 2026 include raw material price surges, accelerated regulatory restrictions in specific jurisdictions, or a breakthrough formulation that reduces NBPT loading rates. Each scenario requires a predefined playbook — from hedging and inventory accumulation to rapid commercialization of alternative technologies. The full PW Consulting report includes quantitative scenario tables and prescriptive management responses for each material risk.

Why PW Consulting’s NBPT study is indispensable for 2026

Our analysis synthesizes validated historical data, forward‑looking forecasts through 2032, concentration metrics, supplier intelligence, and pragmatic implementation tools into a single deliverable designed for executives who must translate insight into locked‑in outcomes in 2026. The study’s layered approach — from topline market trajectories to tactical procurement RFP templates and supplier scorecards — gives teams both the narrative to persuade stakeholders and the operational artifacts to act.

If your 2026 agenda includes supply‑chain resilience, profitable route‑to‑market expansion, or M&A in speciality agrochemicals, PW Consulting’s NBPT Market Study is engineered to convert uncertainty into a prioritized action plan. For access to the detailed sub‑segment tables, regional and application splits, supplier scorecards, and downloadable datasets referenced here, please consult the full report available through PW Consulting’s market intelligence portal.

For detailed analysis of this topic, please visit the official page:N-(n-butyl) Thiophosphoric Triamide (NBPT) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com