North America Copper Cathode Industry Outlook Through 2034

Other |

2026-06-19 10:23:00

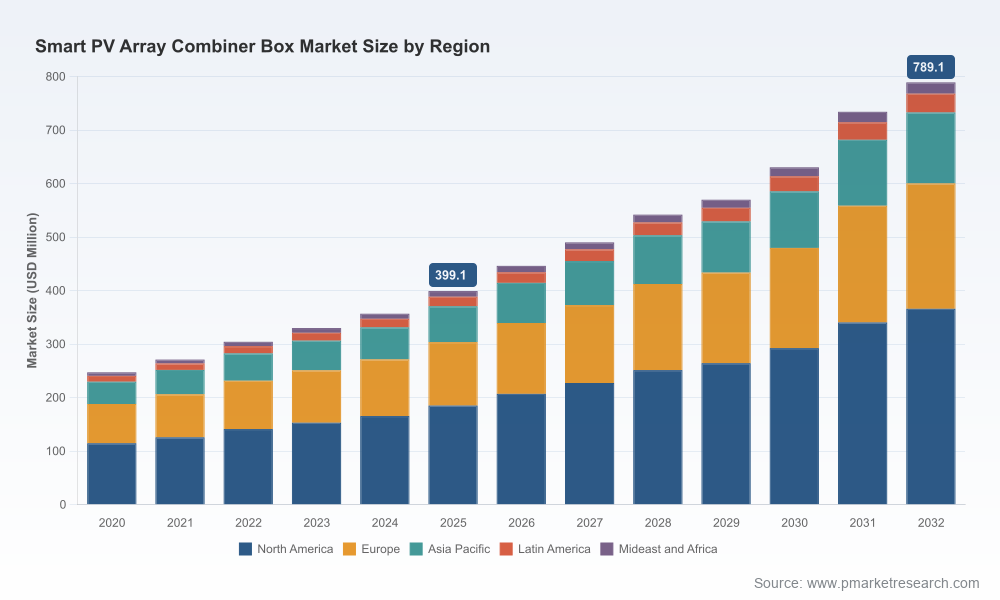

As PV projects accelerate from distributed rooftops to utility-scale arrays, the combiner box has evolved from a passive junction point into a focal node for safety, monitoring and edge intelligence. PW Consulting’s new Smart PV Array Combiner Box Market study (base year 2025; historical 2020–2025; forecast 2026–2032) quantifies this transformation and translates it into the strategic choices executives must make in 2026. The market expanded materially through 2020–2025 and—driven by regulatory tightening, digital O&M adoption and product innovation—is projected to sustain strong growth across the forecast window (2026–2032) at a 10.3% CAGR, moving total industry revenues from the mid-hundreds of USD Million in 2025 toward a substantially larger market by 2032.

Smart PV Array Combiner Box Market

Decision clarity under competing pressures: procurement teams face a mix of rising materials/labor costs, new trade measures, and heightened certification expectations. Our study distills how these forces compress margins and shift sourcing priorities—so you can prioritize supplier relationships, localization and contractual protections.

Smart PV Array Combiner Box Market

Product roadmaps with commercial inflection points: R&D and product management must reconcile feature creep (AI, module-level monitoring, arc-fault detection) with cost sensitivity in utility tenders and rooftop projects. The report maps which capabilities are driving pricing premium and which represent table stakes by 2026.

Smart PV Array Combiner Box Market

M&A and partnership origination: corporate strategy teams can use our benchmarking to identify potential acquisition targets, co-development partners or manufacturing JV locations that accelerate market entry without untenable capex.

O&M and EPC contracting alignment: operations teams can quantify how combiner box selection impacts plant-level availability and lifecycle costs—information critical to structuring long-term O&M agreements and performance guarantees.

Between 2020 and 2025 the smart combiner box market recorded steady expansion as solar deployment diversified and O&M digitization accelerated. By the 2025 base year the industry’s revenue base had grown markedly compared with 2020, reflecting both increased unit shipments and higher ASPs driven by integrated monitoring and safety features. Looking forward, the 2026–2032 forecast period reflects a sustained compound annual growth rate of 10.3% as the market scales toward multi-hundred-million dollar annual revenues, with cumulative investments in smarter BOS (balance-of-system) hardware and embedded software contributing meaningfully to vendor margins and aftermarket services.

Standards and certification are non-negotiable. Compliance with DC-switch and combiner unit standards (including IEC 60947-3 annex D and IEC 61439-2 ed.3) is increasingly enforced by utilities and financiers. Projects without documented compliance face procurement delays or higher insurance costs.

Operational efficiency now drives procurement decisions. Empirical studies show integrated monitoring and smart combiner functionality can improve plant operational efficiency—our synthesis of public and proprietary data highlights efficiency uplifts of up to 25% in specific deployments. For owners and lenders, that uplifts NPV and shortens payback for systems that internalize higher upfront cost.

Cost stacks are shifting. Integrating string-level monitoring and bespoke enclosure requirements typically adds a material premium to unit cost—our field work indicates that customization and enhanced monitoring can increase unit-level costs meaningfully versus basic units, prompting buyers to trade off features versus lifecycle savings.

Trade policy and sourcing risk. A new tariff regime under certain frameworks takes effect in 2026 and will affect import economics for photovoltaic components. Procurement teams must model landed costs with these measures incorporated and consider near-shore manufacturing or alternative suppliers to preserve competitiveness.

Fragmented competitive structure. Market concentration metrics show a fragmented supplier base; no single vendor dominates. This creates room for rapid share shifts driven by product differentiation, certification status and channel strength.

Edge intelligence and predictive maintenance: Vendors bundling IoT connectivity with ML-driven fault prediction are gaining traction in projects that prioritize uptime. These architectures shift value from one-time hardware sales to recurring analytics and service revenue.

Modularity and customization: Modular combiner designs that permit rapid configuration on-site reduce lead times for EPCs and lower inventory risk—especially relevant as project schedules compress.

Safety-first innovations: Arc-fault detection, rapid shutdown compatibility and enhanced enclosure ratings are moving from differentiators to procurement filters—safety compliance is a gating criterion for many large-scale tenders.

Interoperability: Open communication protocols (e.g., Modbus/RS485 and other industry-standard interfaces) and compatibility with inverter and EMS ecosystems determine whether a combiner box is adopted as part of an integrated plant-level solution or used as a stand-alone component.

The vendor field combines legacy electrification champions, inverter/platform specialists and regional system integrators. Each cluster brings distinct strategic advantages:

Schneider Electric SE (France) — leveraging broad electrification expertise to deliver next-generation combiner boxes that combine IoT connectivity with predictive maintenance; appeals to utilities and industrial customers requiring global support.

Eaton Corporation plc (Ireland) — focuses on safety-first product architectures and smart monitoring tailored to utility-scale and commercial systems; strong in protection and switchgear integration.

Sungrow Power Supply Co., Ltd. (China) — emphasizes modular designs and rugged IP ratings for fast deployment across diverse conditions; competitive on unit economics for large-scale builds.

Huawei Technologies Co., Ltd. (China) — pursues AI-driven combiner solutions with machine learning for predictive fault detection and plant-level optimization, positioning products within a broader digital energy stack.

ABB Ltd (Switzerland) — differentiates on advanced protection (including arc-fault detection) and integration with established electrification platforms used by utilities.

SolarEdge Technologies, Inc. (Israel) and Enphase Energy, Inc. (United States) — bring system-level optimization and inverter-combiner integration, respectively, which can simplify procurement and reduce integration risk for EPCs and distributed projects.

Regional specialists and OEMs (China, Australia, Germany etc.) — a large cohort of vendors competes on customization, lead time and price, often owning EPC relationships or local manufacturing that matters for regional tenders.

Recent product launches and capacity investments signal how vendors are translating strategy into execution: leading suppliers expanded IoT and AI-enabled product lines during late 2024 and early 2025, while some producers announced new regional manufacturing capacity to capture near-term demand.

Procurement & supply-chain: Implement dual-sourcing for critical components and build tariff-aware landed-cost models. Where feasible, seek regional production partnerships to mitigate trade measures and accelerate certification.

Product strategy: Prioritize a modular portfolio that separates core safety features (must-haves) from premium analytics (value-adds). This enables tiered pricing and tailored value propositions to residential, commercial and utility customers.

Partnerships & integration: For inverter manufacturers and EMS vendors, integrate combiner functionality into broader system offerings to capture higher share of plant-level value. For EPCs and asset owners, prefer vendors with proven interoperability and a clear roadmap for remote diagnostics.

Certification roadmap: Accelerate compliance testing and third-party validation against IEC standards and relevant national codes. Certification can be a decisive procurement filter for large buyers and financiers.

Commercial models: Shift commercial conversations from component pricing to lifecycle cost and uptime guarantees. Use measured O&M uplift data to justify step-changes in procurement decisions and to underwrite performance-based contracts.

M&A & capital allocation: Target regional system integrators and niche OEMs that can rapidly add technical features or manufacturing scale. Look for targets whose certifications and local presence de-risk market entry.

This introduction highlights the structural forces and tactical levers that will define combiner box strategy in 2026. In keeping with the “trailer” principle, we have intentionally withheld granular segment-by-region and by-application financial breakdowns, detailed vendor share tables and discreet unit-price schedules—content that buyers and competing vendors routinely use to craft winning bids. PW Consulting’s full report contains the complete dataset, including segmented forecasts, vendor scorecards, ballpark ASP ranges, procurement-side playbooks and scenario-driven sensitivity models calibrated to tariff, material cost and regulation scenarios.

For executives preparing 2026 budgets and strategic plans, the actionable insight is clear: prioritize compliance and interoperability; model lifecycle value, not just unit cost; and hedge supply risk through diversified sourcing or regional production. Those who align R&D, procurement and commercial teams to these priorities will capture a disproportionate share of the value created as the smart combiner box becomes central to digitally managed PV assets.

Engage PW Consulting for a tailored briefing that overlays our segment-level forecasts against your project pipeline and supplier roster.

Request the vendor scorecard and supplier risk matrix to prioritize qualification and pilot programs for 2026.

Commission a tariff-sensitivity and landed-cost analysis to inform sourcing decisions as new trade measures come online.

For detailed analysis of this topic, please visit the official page:Smart PV Array Combiner Box Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com