Rhinoplasty in Riyadh for Functional Breathing and Cosmetic Improvement

Health |

2026-07-08 06:16:07

As PW Consulting’s lead industry analyst, I present a focused strategic primer designed to orient senior executives, product leaders, and corporate strategists as they plan investments and go-to-market moves in 2026. Our full market research report delivers a granular, actionable blueprint — but this article will outline the critical strategic themes, macro trajectory, competitive dynamics, and decision levers that should shape near-term choices.

Balanced-armature Magnetic Speakers Market

Low-growth, high-importance market: The balanced-armature magnetic speaker market exhibits modest compound annual growth (CAGR ~1.5%) through the forecast horizon, with year-to-year oscillations that reflect product refresh cycles, macro demand shifts, and pockets of premiumization. For incumbents and challengers alike, steady growth masks decisive inflection points in technology, supply chain positioning, and regulatory posture.

Balanced-armature Magnetic Speakers Market

Strategic timing: 2026 is a year when product roadmaps, supplier contracts, and M&A windows opened in 2024–2025 begin to deliver outcomes. Our study provides the timing intelligence to align capital allocation with those windows — whether for sourcing, product upgrades, or acquisitive scale.

Balanced-armature Magnetic Speakers Market

Structural opportunity beyond headline growth: When top-line growth is modest, margin expansion, product differentiation, and channel optimization become primary returns generators. This report shows how to extract disproportionate value through premium multi-driver architectures, integration of crossovers, IP-led differentiation, and selective vertical integration.

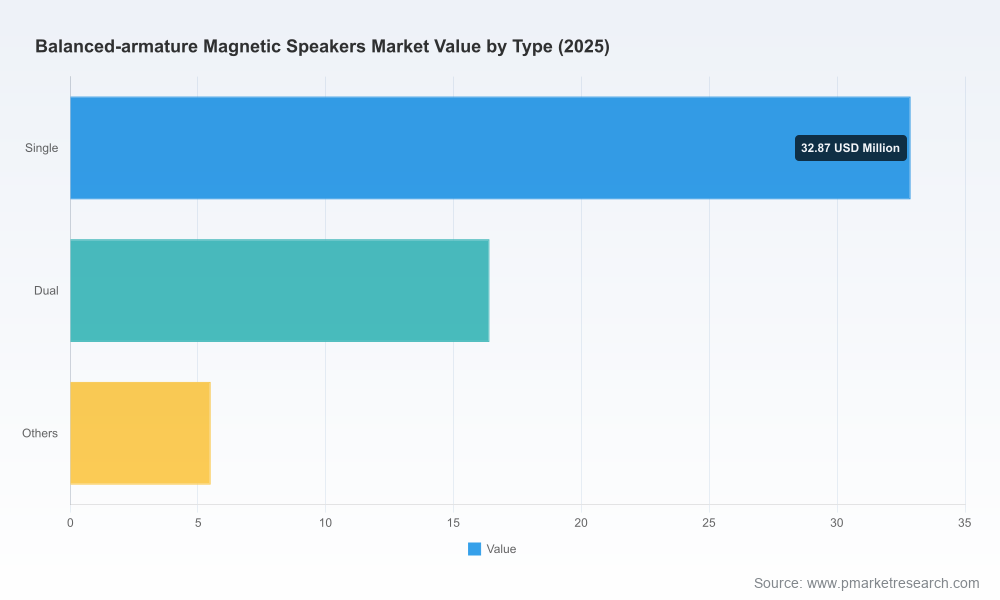

Across the 2020–2025 historical period the market hovered in a narrow band indicative of mature demand with episodic uplifts tied to device cycles. The 2025 base year anchors our view: the market sits near the mid‑fifties in USD million terms and, absent major structural shocks, the forecast through 2032 projects a low-single-digit expansion consistent with a ~1.5% CAGR. The path is not monotonic; you will see short dips and rebounds reflecting supply constraints, OEM design cycles, and pockets of premium product adoption. By 2030–2032 the aggregate market is modestly higher than the mid-2020s, presenting steady, risk-managed upside for disciplined players.

Top-line market sizing and robust forecast models (2026–2032) with scenario stress-testing for recessionary and fast-innovation outcomes.

Segmentation frameworks by form-factor, driver architecture, and end-use case — each paired with demand drivers, supplier risk matrices, and pricing elasticity models. (Note: we deliberately withhold granular segment allocations in this preview — full breakdowns are available in the report.)

Actionable supplier maps, including tiering of manufacturers by capability (miniaturization, multi-driver integration, and regulatory compliance), lead-time profiles, and capacity elasticity analyses.

Product and engineering playbooks for optimizing driver mixes in premium TWS earbuds, IEMs, and hearing devices, including cost vs. performance trade-off curves and BOM optimisation tactics.

Commercial strategy modules: channel prioritization, pricing architecture, bundling and hybrid product strategies for maximizing ASPs and margins.

M&A and partnership scorecards: targets, integration risk assessments, accretion/dilution modeling, and cultural-fit heuristics specific to the balanced-armature supply ecosystem.

Regulatory and IP risk assessment: compliance checklists for hearing-health applications, and scenario playbooks for import/export friction and IP disputes.

The market shows a clear leader set and a strong tier-two cohort, producing a moderately concentrated competitive structure where the top players control a significant share. That concentration implies meaningful signaling from the actions of the leading suppliers: new product families, strategic OEM wins, and IP enforcement activity materially reallocate value across the supply chain.

Knowles Corporation — A proven leader in multi-way and premium drivers, actively commercializing pre-configured multi-driver combinations with integrated crossover circuitry. Recent product introductions and strategic OEM selections demonstrate Knowles’s playbook: accelerate time-to-design-win by offering pre-validated driver modules that reduce engineering friction for premium TWS and IEM applications.

Sonion A/S — A specialist in miniature receivers with deep penetration in regulated hearing applications. Sonion’s advantage lies in tight integration with hearing-aid OEM requirements and long-term regulatory pedigree — a critical asset as hearing-health regulations evolve and over-the-counter categories expand.

Etymotic Research — A niche player focused on high-performance micro-drivers and acoustic fidelity for in-ear monitors and professional applications. Etymotic’s R&D orientation supports premium channel strategies where audio quality commands price premiums.

Bellsing Acoustic Tec. Co., Ltd. — An important high-volume supplier with strong manufacturing scale. Its presence underscores the geopolitically sensitive nature of the supply chain; previous trade and IP disputes have had ripple effects on OEM sourcing choices and risk premiums.

Product launches of multi-way families and integrated driver/crossover modules sharpen time-to-market advantages for players that can commoditize complex acoustic design work. For OEMs, these modules reduce engineering costs and accelerate premium product cycles.

Notable OEM selections of established suppliers validate the premiumization path in the TWS/IEM segments — if your product roadmap targets the high end, supplier selection and design-in timing are decisive.

IP and trade frictions involving replica designs raise the cost of uncertainty for OEMs that rely on single-source or geopolitically concentrated supply chains. Strong IP portfolios and compliance track records are now premium procurement criteria.

Geopolitical and trade risk: Sourcing concentration in certain geographies increases exposure to export restrictions and IP-related investigations. Mitigation: diversify qualified suppliers, structure dual-sourcing contracts with performance SLAs, and maintain contingency inventory for critical components.

Regulatory risk: Hearing health and over-the-counter device rules can change product certification needs. Mitigation: prioritize suppliers with proven regulatory compliance, and embed regulatory checks into product development timelines.

Technology risk: Rapid adoption of hybrid architectures (balanced armature + dynamic drivers) and embedded electronics shifts design complexity. Mitigation: secure partnerships with suppliers offering pre-integrated modules or co-development agreements.

Concentration risk: Market concentration among a few suppliers increases bargaining power asymmetries. Mitigation: invest in supplier development programs and evaluate strategic equity or partnership arrangements to align incentives.

For executives preparing 2026 budgets and roadmaps, prioritize actions that convert limited top-line growth into sustainable margin and market-share gains:

Lock in design wins early in the product cycle using supplier-provided pre-configured modules to reduce NRE and time to market.

Reassess procurement KPIs to include IP and regulatory compliance as core dimensions, not just price and lead time.

Run a targeted supplier diversification program for critical miniaturized drivers, focusing on dual-sourcing and capability redundancy.

Explore bolt-on acquisitions or strategic JV opportunities that add complementary IP (e.g., crossover design, micro-electronics) rather than just capacity.

Deploy scenario-driven margin models that stress-test product plans against longer lead times and modest demand shocks — the full report includes downloadable financial templates tuned to the market’s dynamics.

We designed the report to convert market intelligence into executable choices. It pairs rigorous market-sizing and forecast models (historical baseline 2020–2025, base year 2025, forecast 2026–2032) with practitioner tools: supplier scorecards, product-architecture playbooks, and M&A target filters. The objective is to help clients make defensible investments in sourcing, product architecture, and inorganic growth during a period characterized by low-but-stable growth and concentrated supplier power.

This article profiles the decision levers and strategic implications without disclosing the granular segment allocations and revenue-by-application detail that many teams require to execute. For access to the full data matrices, downloadable financial models, supplier maps, and the competitive-dashboard with scenario toggles — visit the PW Consulting report page and download the complete Balanced-armature Magnetic Speakers Market brief. The full deliverable is the working toolkit your 2026 strategy team needs to move from insight to implementation.

Balanced-armature technology remains central to modern in-ear audio and regulated hearing solutions. In an environment of modest aggregate growth, 2026 will favor organizations that convert engineering-led differentiation and supplier strategy into defensible commercial advantage. The right combination of supplier selection, regulatory readiness, and product architecture will determine who captures the best margins in the next cycle. PW Consulting’s market study is structured to be the operational playbook that helps you do exactly that.

For detailed analysis of this topic, please visit the official page:Balanced-armature Magnetic Speakers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com