Medication-Assisted Treatment (MAT) Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-14 08:04:14

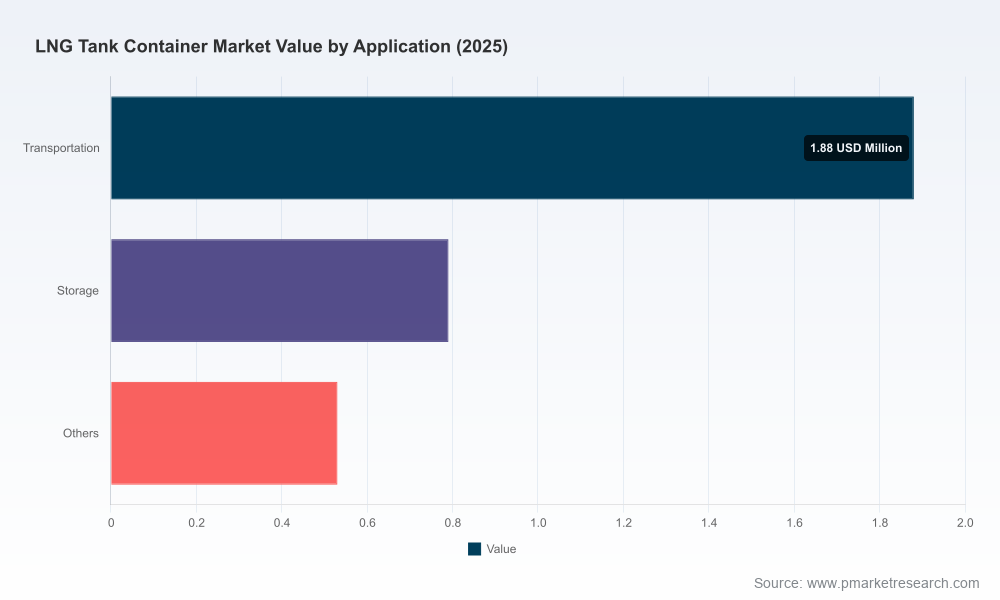

The LNG tank container market has moved from niche to strategic infrastructure in under a decade. Our PW Consulting study—anchored on a 2025 base year, with historical analysis covering 2020–2025 and an outlook spanning 2026–2032—shows a clear, sustained expansion: global market revenues rose from USD 2.23 Million in 2020 to USD 3.20 Million in 2025 and are projected to reach approximately USD 5.31 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.5% across the forecast window. That trajectory is more than academic: it is a mandate for boardrooms, mid-market operators, and financiers to redesign strategies for sourcing, manufacturing, deployment, and risk management in 2026 and beyond.

LNG Tank Container Market

Transition dynamics are accelerating. Energy policy drivers, decarbonization commitments and the economics of "virtual pipelines" have raised demand for flexible, multimodal LNG transport and storage solutions. That increases both short-term procurement pressure and long-term capital planning needs.

LNG Tank Container Market

Supply-side constraints are materializing. Specialized materials (cryogenic-grade steels, high-vacuum insulation components) and certified fabrication capacity are concentrated and skill-dependent. This raises lead times and creates strategic sourcing risk for new-build programmes and fleet expansions.

LNG Tank Container Market

Regulatory harmonization and class certification requirements are tightening across routes and modalities. Compliance is non-negotiable and creates both a barrier to entry and a moat for incumbents with proven certs and audit trails.

Commercial models are diversifying. Leasing and asset-light models are growing alongside owner-operator fleets, altering revenue streams for manufacturers, lessors and logistics providers.

Our report is designed as an operational intelligence package for decision-makers who cannot afford ambiguity. Highlights include:

High-resolution market sizing: end-to-end historical (2020–2025) and forward-looking (2026–2032) revenue curves, base-year (2025) normalization, and scenario-driven forecasts reflecting alternative adoption and regulatory paths.

Demand scenario modelling: three validated demand trajectories (conservative, base, accelerated) that capture commodity-price sensitivity, policy shocks, and infrastructure roll-out timetables—ready to be stressed with client-specific inputs.

Supplier and capability mapping: an actionable vendor map, manufacturing footprint analysis, and a modular capability scorecard to evaluate prospective partners and acquisition targets.

Commercial tools and templates: procurement playbooks, lease vs. buy financial models, EBITDA and total cost of ownership (TCO) calculators tailored for LNG ISO containers, and contract clauses to mitigate lead time and certification risk.

Engineering and compliance dossiers: a distilled regulatory matrix (ISO, IMDG, ADR, RID, ASME, DOT and class societies), material specification notes, and an operations-quality checklist for cryogenic fabrication and assembly.

Competitive intelligence and M&A watch: a ranked list of strategic targets, strengths/weaknesses of market players, and likely consolidation vectors—sufficient for transaction screening or defensive planning.

Aftermarket and services playbook: modular service revenue levers (maintenance, lease management, retrofits) and margin-protection strategies for OEMs and lessors.

The LNG tank container industry displays meaningful concentration: our report quantifies a top-three concentration (CR3) at approximately 57% and a top-five concentration (CR5) near 68%. In practice, that means a handful of manufacturers and leasing specialists control the bulk of certified capacity, with a trailing cohort of regional players and new entrants addressing niche applications and lower-volume markets.

CIMC Enric Holdings Limited (Shenzhen) — strengths lie in scale, broad product families and multi-jurisdiction certifications. Their global standardization plays make them a default partner for large OEM-to-shipper programs.

Zhangjiagang Furui Group (Zhangjiagang) — specialist cryogenic designs and expanding export activity; recent deliveries to North American projects demonstrate tactical moves into higher-margin, international supply chains.

TransWorld Equipment (United States) — acts as a regional anchor for hazardous and high-pressure ISO tanks, coupling global OEM reach with local sales, service and aftermarket support across the Americas.

Chart Industries, Inc. (United States) — recognized for transportable tanks and T75-class intermodal containers; strategic emphasis on virtual pipeline applications and exhibition-led business development reinforce market visibility.

Srisen Energy Technology (China) — niche verticals and broader capacity ranges position them as options for unconventional or bespoke projects where standard ISO recipes are insufficient.

MCM Management, Control & Maintenance (Switzerland) — leasing-first model and innovative designs (e.g., baffle-equipped tanks) indicate rising service-orientation and fleet diversification among lessors.

Recent industry moves are instructive: a January 2026 delivery by Zhangjiagang Furui into the U.S. market signals accelerating cross-border demand, MCM’s mid-2024 product launch demonstrates leasing platforms expanding technical differentiation, and Chart’s exhibition presence highlights the marketing of virtual-pipeline use-cases. These tactical signals suggest vendors are pursuing a blend of scale, certification breadth, and service-led differentiation rather than pure price competition.

How conservative or aggressive should your demand assumptions be when sizing procurement and manufacturing capacity given a 7.5% CAGR baseline?

Where will you anchor certification and class partnerships to minimize time-to-deploy risk across major trade lanes?

Which parts of the value chain should be insourced (e.g., cryogenic welding, vacuum systems) versus outsourced to scale quickly?

What’s your operating mix between owned fleet and leased containers, and how will that affect balance sheet, working capital and uptime guarantees?

Which vendors provide the best trade-offs across lead time, certification, geographic footprint and service capability—based on your risk tolerance?

Run a demand-scenario workshop to stress-test capital plans against the three PW Consulting demand paths and create a contingency capex envelope.

Audit your certification roadmap: secure pre-approvals and class society engagement to avoid last-mile delays in deployment.

Lock strategic supply agreements for critical raw inputs and high-value assemblies; build dual-sourcing for insulation and inner-vessel components where possible.

Negotiate phased manufacture contracts with milestone-based payments to transfer lead-time and technology risks to suppliers.

Pilot a mixed ownership model: pair a leased fleet tranche (to meet near-term demand spikes) with a managed build-out of owner assets for long-term margin capture.

Invest in workforce readiness: certify in-house welders and QA technicians to reduce dependency on scarce external labour pools.

Prepare an M&A screening list aligned to capability gaps—manufacturing, certification, or regional access—and fund a diligence sprint.

Raw material price and availability shocks for cryogenic-grade steels and insulation materials.

Regulatory changes affecting pressure ratings, modal compliance, or class society requirements.

Certification bottlenecks at key class societies and notified bodies delaying commercial roll-outs.

Geopolitical trade measures that could alter manufacturing economics or input flows.

Labour-market constraints for specialized cryogenic fabrication skills, increasing lead times and capitalizing labour costs.

For executives in procurement, manufacturing, logistics, and corporate development, the PW Consulting LNG Tank Container study is engineered to convert market insight into decisions. It combines granular engineering and regulatory intelligence with commercial models, vendor benchmarking, and a service-and-maintenance playbook—delivering both the strategic context and the operational templates that drive execution.

We intentionally present this preview to demonstrate the depth and rigor of our analysis while preserving the detailed segmentation and proprietary vendor scores that power bespoke decision-making recommendations. The full report includes the complete product-, application- and regional-split datasets, downloadable financial models, vendor scorecards, and a market-concentration dashboard tailored to facilitate board-level approvals and capital allocation exercises for 2026.

To access the full dataset, scenario workbooks and procurement templates necessary for immediate execution in 2026, visit the PW Consulting report page and request the comprehensive study. Our team is available to brief executive committees and run a targeted, one-day strategy sprint to translate the findings into your operational plan.

For detailed analysis of this topic, please visit the official page:LNG Tank Container Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com