Virtual Specialty Consultation Networks Market Overview: Key Drivers and Challenges

Other |

2026-04-30 11:15:58

As companies enter strategic planning cycles for 2026, the viscose staple fiber (VSF) market presents a blend of predictable macro growth and heightened structural uncertainty. Our analysis uses 2025 as the base year and integrates a consolidated historical view (2020–2025) with a forward-looking forecast window (2026–2032). On the macro level, the market expanded from approximately USD 12.3 billion in 2020 to USD 16.2 billion in 2025 (USD Million units), and is projected to rise to roughly USD 17.8 billion in 2026. Over the 2026–2032 forecast horizon the market is expected to grow at a compound annual growth rate (CAGR) of about 6.98%, reaching an estimated USD 25.9 billion by 2032.

Viscose Staple Fiber Market

This preview highlights the strategic implications of that trajectory for 2026 decisions: where to allocate capital, how to prioritize sustainability investments, which value pools to defend or enter, and what competitive responses are most likely to protect margins and market position. In keeping with our “trailer” principle, we demonstrate the depth of analysis available in the full PW Consulting study while intentionally withholding granular segment-level numbers in this introduction to encourage deeper engagement with the full report.

Viscose Staple Fiber Market

Macro momentum: Steady market growth creates room for both organic expansion and value-accretive M&A. Management teams should translate the ~7% medium-term CAGR into scenario-based capacity plans rather than single-point forecasts.

Viscose Staple Fiber Market

Regulatory inflection points: Policy shifts in major consuming regions now reward closed-loop and low-emission technologies. These are not peripheral compliance matters — they are demand multipliers that change product premiums and buyer sourcing behavior.

Feedstock and integration risks: Cellulose feedstock (dissolving pulp) price volatility remains a primary margin driver. Upstream integration, diversified sourcing, and circular feedstock strategies are strategic levers that materially alter competitive economics.

Sustainability as a value driver — not just compliance. Buyers in North America and Europe increasingly favor closed-loop, low-emission VSF solutions. Producers that can credibly demonstrate those attributes capture pricing premiums and longer-term offtake relationships with fashion and FMCG brands.

Specialty fibers and nonwovens as margin stabilizers. Demand for specialty grades (medical, hygiene, technical nonwovens) has become a countercyclical offset to apparel volatility. Firms that can pivot capacity or maintain flexible product lines benefit from higher average realized prices.

Upstream integration and feedstock hedging. Dissolving-pulp price swings materially affect unit economics. Vertical players with integrated pulp supply or long-term contracts have a durable cost advantage; independent producers must deploy hedging and supplier diversification strategies.

Geopolitical and regulatory fragmentation. Recent policy moves — including regulatory changes in India and stronger sustainability mandates in Western markets — create asymmetric competitive advantages and new market-access considerations for 2026.

Capacity dynamics and consolidation. The market structure remains moderately concentrated: the leading few producers command a meaningful share of capacity, with a handful of large-scale expansions announced through 2025. The resulting supply dynamics will shape pricing trajectories and M&A opportunities in 2026.

Lenzing AG (Austria) — Distinctive for closed-loop wood-based viscose production and strong branding through its TENCEL™/LENZING™ platform. Their emphasis on technology partnerships and brand-led sustainability positions them as the premium supplier for brands prioritizing traceability and lifecycle claims.

Birla Cellulose / Aditya Birla Group (India) — A scale-integrated player with a strong upstream pulp position and aggressive capacity expansion strategy. Their combination of integrated supply and cost competitiveness makes them a primary driver of regional supply dynamics.

Sateri Holdings (Singapore/China) — Multi-mill footprint and focus on modernized facilities; competes on scale and operational efficiency while increasingly emphasizing sustainability credentials.

Tangshan Sanyou Group (China) — Differentiates through recycled-content offerings and a significant focused capacity; these attributes make them a strategic choice for buyers seeking circular solutions.

Selected Chinese producers (e.g., NCFC, Xinjiang Zhongtai, Yibin Grace, Jilin Chemical Fibre) — A mix of regional champions and specialty innovators: some prioritize low-cost, large-scale supply while others invest in niche, higher-value grades such as bamboo blends or recycled-content fibers.

Recent strategic moves — a commercial-scale launch of bamboo-recycled blended fiber, major capacity additions in India, and brand partnerships on sustainable product lines — are signals that incumbents are sharpening both scale- and sustainability-driven playbooks heading into 2026.

For executive teams preparing 2026 budgets and strategic plans, the full study contains practical tools and analytics designed to convert insight into action. Highlights include:

Demand-supply model across 2020–2032 with modular drivers you can re-run for custom scenarios.

Pricing sensitivity and margin-impact simulation tied to dissolving-pulp price paths and energy cost assumptions.

Plant-level capacity mapping and technology benchmarking for major producers, plus an operational maturity matrix for closed-loop capability.

Playbook templates: CapEx prioritization, M&A screening scorecards, and contract structures for securing long-term pulp supply.

Commercial strategy tools: buyer segmentation, go-to-market options for specialty fibers, and supplier engagement frameworks for brand partners.

Regulatory and reputational risk checklist, including the implications of policy shifts such as the removal of certain product licensing requirements in key markets and the incentives created by sustainability mandates in Europe and North America.

We recommend that leadership teams structure 2026 decisions around a small set of high-impact scenarios and explicit triggers. Below are three condensed scenarios and suggested strategic moves:

Baseline Growth (most likely): Market follows the ~7% CAGR with steady uptake of sustainability-labelled fibers. Trigger: stabilized pulp prices and no major trade barriers. Actions: accelerate selective capacity upgrades for specialty grades; negotiate long-term pulp contracts; pursue brand partnerships to lock in offtake.

Sustainability Premium Upside: Western procurement policies and retailer commitments create meaningful price premiums for closed-loop fibers. Trigger: certification or policy enforcement that materially raises the value of closed-loop claims. Actions: fast-track closed-loop retrofits; prioritize product lines for premium channels; consider licensing/brand collaborations to monetize sustainability claims.

Feedstock Volatility / Oversupply Downside: Rapid capacity additions in certain regions combine with dissolving-pulp price spikes, compressing margins. Trigger: large-scale capacity ramp-up announcements coupled with pulp-price surges. Actions: conserve cash; deploy flexible production strategies (switchable lines for nonwovens/specialty); evaluate asset-light partnerships or divestitures for underperforming lines.

Feedstock price risk: Use a combination of vertical integration, long-term contracts, and financial hedging to protect EBITDA.

Regulatory/reputational risk: Invest in credible chain-of-custody and emissions monitoring to avoid market exclusion in premium channels.

Demand concentration risk: Diversify end-market exposure (textiles, nonwovens, specialty) to smooth cyclical apparel downturns.

Technology risk: Validate closed-loop and recycling technologies through pilot programs before full-scale conversion; partner for co-development where appropriate.

Competitive overhang: Monitor announced large capacity projects and plan defensive price/marketing strategies; identify consolidation targets where scale gaps threaten margin erosion.

Treat the macro numbers here as directional inputs for scenario planning; use the full model to stress-test balance-sheet implications under different demand, price, and feedstock paths.

Prioritize investments that create asymmetric value: those that reduce feedstock exposure, unlock sustainability premiums, or open non-apparel channels where VSF commands higher, more stable margins.

Engage with strategic partners early. Brand partnerships, technology licensors, and integrated pulp suppliers will be pivotal levers in 2026 — securing them ahead of peer movements often yields disproportionate advantage.

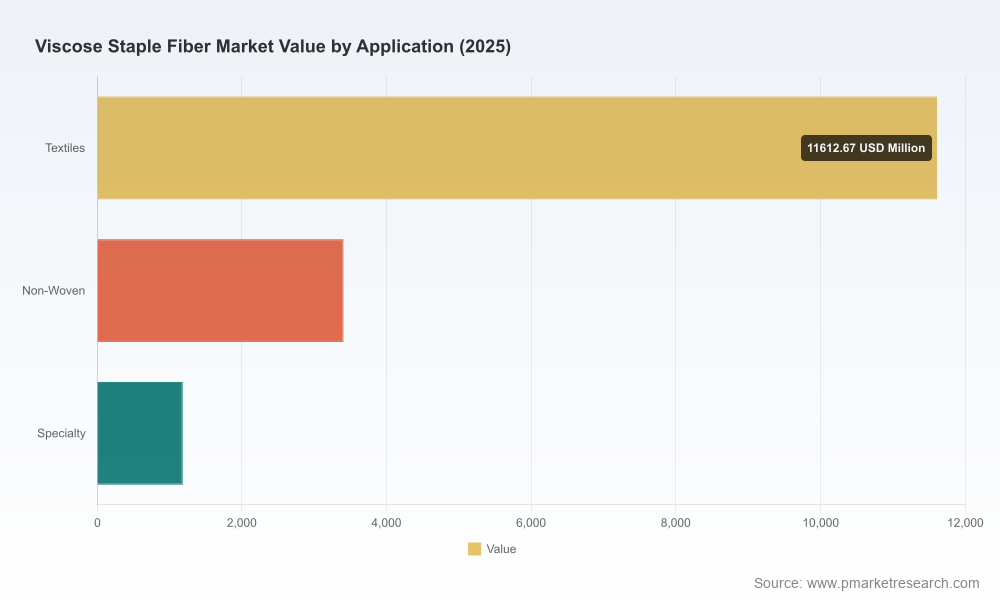

This preview demonstrates the analytic framing and strategic line-of-sight available in PW Consulting’s full Viscose Staple Fiber Market study. The complete report contains the granular segmentation, regional and application splits, competitive share tables, pricing curves, plant-level capacities, and downloadable scenario models that underpin the strategic recommendations summarized above. We intentionally withhold those segment-level figures in this public preview to protect the integrity of our primary research and to invite direct engagement for firms seeking executable intelligence.

For boards, corporate strategy teams, and investment committees preparing for 2026, the full deliverable provides the operational playbooks and quantitative models needed to convert the market’s growth trajectory and structural shifts into clear, prioritized actions.

For detailed analysis of this topic, please visit the official page:Viscose Staple Fiber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com