Doorbell Market 2026: Strategic Imperatives from PW Consulting’s Market Preview

As organizations prepare strategies for 2026, the video doorbell market presents a classic intersection of rapid technology adoption, regulatory re‑balancing, and fragmented competition. PW Consulting’s Doorbell Market research (base year 2025) synthesizes a multi‑year market trajectory—from the mid‑single‑hundreds (USD Million) in the early 2020s to a projected expansion through the forecast window—driven by converging forces in home automation, last‑mile logistics, and edge AI. With a compound annual growth rate of 13.45% from 2026 through 2032, the sector is far from mature: it is scaling, segmenting, and inviting both incumbent expansion and new‑entry disruption.

Doorbell Market

Market snapshot and trajectory

Between 2020 and 2025 the market moved from an emergent niche into a recognizable product category within broader smart‑home and security portfolios. The 2025 baseline that informs our 2026 strategic guidance reflects this maturation and validates a multi‑year acceleration that continues into the 2026–2032 forecast. That acceleration is not linear; it is concentrated around technology inflection points—higher resolution imaging, hybrid wired/battery power models, on‑device AI, and standards‑driven interoperability—that raise the IMU (importance, monetization, urgency) for corporate decision‑makers.

Doorbell Market

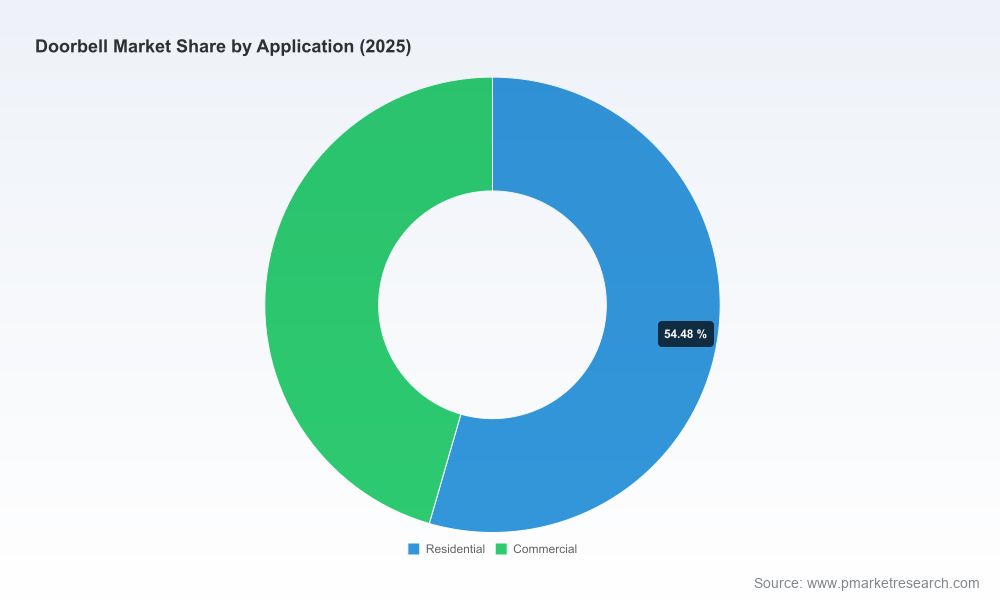

Two facts matter for near‑term decisions: first, the market size and trajectory deliver both scale and runway for investment; second, competitive concentration remains modest—our concentration metrics show a low single‑digit top‑tier capture relative to the overall market—signaling persistent fragmentation and opportunity for curated scale plays, platform consolidation, and vertical integration.

Doorbell Market

Why the 2026 decision window is pivotal

- Product roadmap acceleration: 2026 is the first full year post‑rollout of updated interoperability standards that materially impact device behavior and integration. Suppliers who embed these standards now will shorten time‑to‑value for channel partners and reduce integration friction with major ecosystems.

- Monetization model choices: Consumers increasingly demand privacy‑forward options (local storage, on‑device AI) while subscription services remain an important ARPU lever. Choices made in 2026 about hybrid monetization (one‑time hardware premium vs. optional cloud tiers) will determine long‑term customer lifetime value.

- Channel reconfiguration: The balance between pro integrators, retail, and direct‑to‑consumer shifts as products offer more enterprise‑grade features. Companies that map differentiated SKUs to the right channel will unlock faster adoption curves.

- Regulatory and certification risk: The evolving telecommunications and certification landscape means 2026 is the year to invest in compliance, not react to enforcement. Early investment reduces market entry friction and reputational exposure.

What the report delivers to practitioners

PW Consulting’s Doorbell Market study is designed as a decisioning toolkit, not a passive read. The report blends quantitative market modeling with prescriptive, executable outputs that leadership teams can operationalize in 90–180 day cycles. Key deliverables include:

- Proprietary market model (2020–2032) with scenario planning and sensitivity testing tied to pricing, channel mix, and feature premium assumptions.

- Go‑to‑market playbooks for three strategic archetypes—volume OEMs, privacy‑first challengers, and enterprise/security integrators—with launch checklists and KPIs.

- Technology roadmap synthesis that maps camera resolution, AI inference placement (cloud vs. edge), power architectures, and interoperability (Matter/HomeKit/others) against adopter segments.

- Commercial models demonstrating subscription vs. one‑time revenue outcomes across realistic adoption curves and churn assumptions.

- Supply‑chain and sourcing risk matrix, including semiconductor exposure, PCB supplier concentration, and logistics scenarios tied to pricing shocks.

- Regulatory impact analysis and certification checklist tailored for North American, European, and multi‑jurisdiction certification strategies.

- Competitor playbooks and a shortlist of acquisition targets for roll‑up strategies—scored by technology, route‑to‑market, and integration complexity.

Competitive landscape — who matters and why

The doorbell market is populated by a mix of consumer electronics brands, smart‑home specialists, traditional security vendors, and nimble challengers. Each group pursues distinct value propositions:

- Platform and ecosystem players (e.g., Google’s Nest line) use seamless assistant integration and brand reach to convert existing ecosystem users into doorbell upgrades. Their strategic asset is the platform hook that increases switching costs.

- Mass‑market connectivity vendors (e.g., TP‑Link) emphasize affordability, broad retail distribution, and smart‑home compatibility, making them go‑to choices for value seekers and large volume channels.

- Privacy‑first challengers (e.g., Eufy) compete on local storage, no‑subscription messaging, and on‑device AI—positioning that resonates with privacy‑sensitive segments and certain enterprise micro‑markets.

- High‑feature innovators (e.g., Arlo, Reolink) push resolution, battery longevity, and advanced AI features (package detection, head‑to‑toe views) to justify premium price points and pro‑grade deployments.

- Traditional security and industrial suppliers (e.g., Hikvision, Bosch) target commercial and professional install bases, leveraging system interoperability, PoE solutions, and enterprise‑grade analytics.

- Specialist integrators (e.g., Signify/Philips Hue) bring unique cross‑product integration—lighting plus motion—creating differentiated value propositions for use cases like automated illumination during detection events.

Collectively these players have pushed rapid feature parity (2K video, AI motion alerts, wired/battery flexibility) while retaining strategic separations: ecosystem anchoring, privacy posture, distribution strength, and enterprise integration. Notably, the market’s top three and five players account for a relatively modest share of total sales—confirming fragmented dynamics and opportunities for carve‑outs and roll‑up strategies.

Recent product and regulatory shocks to watch (2025–2026)

- Product innovations: Several vendors launched or announced notable doorbell products in the 2025–2026 cycle—advances in battery life, solar charging options, 2K/4K imaging, multi‑camera arrangements, and radar‑enabled motion detection. These launches reset customer expectations around runtime, low‑light performance, and package/person detection.

- Interoperability standards: Matter 1.5.1 (released March 31, 2026) introduced refinements specific to doorbell device types and streaming efficiency. For product teams, this is a turning point: certified devices gain a measurable integration advantage with major smart‑home ecosystems.

- Certification and enforcement activity: Regulatory agencies and standards bodies have sharpened scrutiny of equipment authorization and certification integrity. Public enforcement actions and government rulemaking in recent periods underline the importance of robust compliance workflows for both market access and brand protection.

Strategic playbook: recommended priorities for 2026

- Embed standards early: Prioritize Matter 1.5.1 compliance where feasible—this reduces integration cost for channel partners and accelerates time‑to‑deployment in smart‑home bundles.

- Design for hybrid monetization: Offer modular subscription bundles while preserving a compelling no‑subscription core feature set (local storage, basic AI). This hedges against regulatory pressure on recurring charges while enabling ARPU expansion.

- Invest in edge AI and power efficiency: Differentiation through longer battery life and high‑quality on‑device analytics reduces cloud costs and addresses privacy‑conscious buyers.

- Build certification and compliance as a capability: Bring forward resources for testing, third‑party certification, and supply‑chain traceability to mitigate the risk of fines and market access delays.

- Segment channel strategy: Map SKUs to channels—simple, low‑price SKUs for retail; premium, integrator‑friendly SKUs for pro installs; and platform‑integrated SKUs for ecosystem lock‑in.

- Prepare M&A and partnership playbooks: With fragmentation remaining high, targeted acquisitions (software analytics, regional distribution, manufacturing scale) can buy time and capacity at a defensible cost.

Conclusion — the opportunity for 2026

For executives defining 2026 strategies, the doorbell market balances scale and openness: the category is large enough to support meaningful revenue growth (supported by the market’s multi‑year expansion), yet fragmented enough to reward decisive product, channel, and M&A moves. Companies that act now—by aligning product roadmaps with interoperability standards, by operationalizing certification and compliance, and by choosing monetization strategies that respect privacy and channel economics—will capture disproportionate share of the upside through 2032.

PW Consulting’s full Doorbell Market report contains the detailed segmentation, model outputs, competitor scorecards, and executable playbooks that underpin the strategic recommendations summarized here. Access the complete study on PW Consulting’s website to download the granular datasets, scenario models, and bespoke advisory options tailored to vendor, investor, or integrator needs.

For detailed analysis of this topic, please visit the official page:Doorbell Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com