Reliable Energy Storage Applications Sustaining Market Relevance

Networking |

2026-06-10 10:08:42

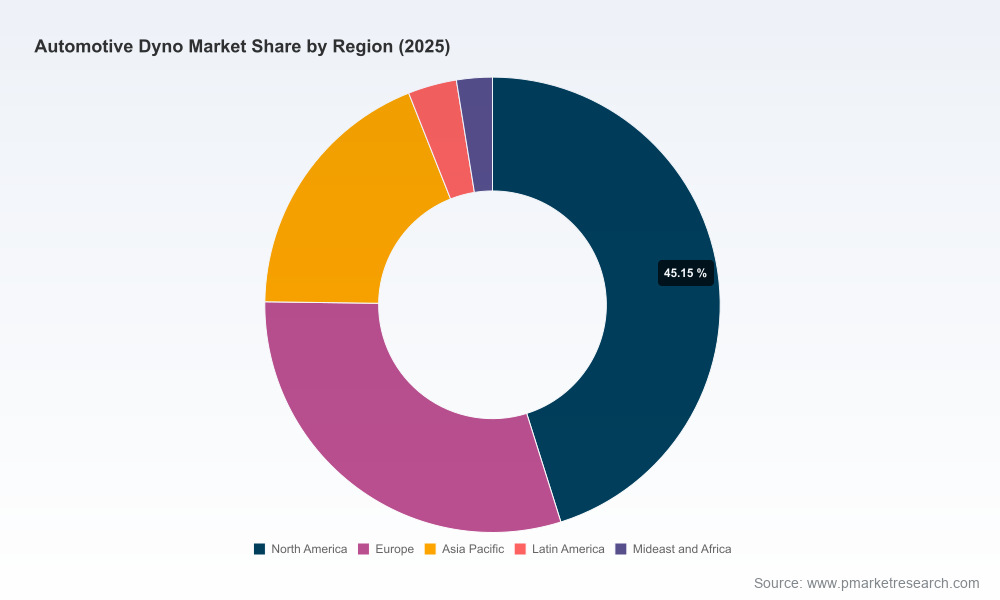

The automotive dyno market has moved from a specialized testing niche into a strategic infrastructure layer for powertrain validation, EV/hybrid transition, emissions compliance and high-performance tuning. Between 2020 and 2025 the market expanded from roughly USD 1.4 billion to USD 2.0 billion, and our base-year model (2025) indicates a compound annual growth rate (CAGR) of 5.21% through the 2026–2032 forecast window, reaching an expected market size of nearly USD 2.84 billion by 2032. For executives making allocation decisions in 2026—whether in R&D capital, manufacturing footprint, service networks or M&A—this research functions as a decision-grade playbook that translates market dynamics into prioritized options and quantified risk vectors.

Automotive Dyno Market

Timing capital investments: Test capacity and types (e.g., chassis, engine, hub-coupled and electric motor stands) have materially different capex profiles and utilization trajectories as OEMs accelerate EV and hybrid programs. Understanding medium-term demand growth and utilization scenarios is essential to avoid stranded test assets or, conversely, missed validation windows.

Automotive Dyno Market

Structuring supplier and partnership strategies: Dyno platforms are increasingly modular and software-defined; decisions about vertical integration, long-term service contracts and digital twin partnerships will determine test cycle speed and cost per validated vehicle.

Automotive Dyno Market

Regulatory preparedness: Evolving emissions and real-driving test requirements continue to shape the specification set of dyno systems. Leaders must map compliance timelines into procurement and retrofit schedules to keep product validation on-path.

M&A and bolt-on opportunities: Moderate market concentration (top-3 players holding a meaningful share and top-5 expanding reach) creates acquisition opportunities that can rapidly expand capability sets (e.g., automated test cells, EV motor test benches, hub dyno expertise) while producing scale advantages in after-sales service.

The market’s expansion from approximately USD 1.4 billion in 2020 to USD 2.0 billion in 2025 is not merely volume growth; it reflects a qualitative shift in product architecture and buyer intent. The underlying CAGR of 5.21% through 2032 embodies a blended outcome: steady investment from OEM validation programs, episodic aftermarket and motorsports demand, and periodic large-ticket procurements for high-capacity EV test benches. For 2026 strategy cycles, leaders should treat the projected mid-decade growth as a base case—preparing parallel response options for upside scenarios driven by accelerated EV mandates or downside scenarios tied to macro-driven capex deferral.

Electrification & powertrain diversity: Battery electric vehicles and hybrid systems are stretching validation requirements—demanding high-power hub dynos, modular electric motor stands, and combined thermal-powertrain test capabilities. Customers seek test benches that can be reconfigured as vehicle architectures evolve.

Regulation and compliance cycles: New test protocols and real-driving-emission (RDE) cycles increase the need for automated, repeatable test procedures and data traceability, favoring suppliers who provide integrated software, accreditation support and long-term calibration services.

Serviceability & uptime: Global OEM and fleet service networks reward suppliers with rapid spare parts logistics and remote diagnostic capability. Investment in distributed service centers and digital monitoring is as important as the test hardware itself.

Supply-chain raw material and components: Durability-critical components (e.g., braking systems for eddy-current dynos) are influenced by alloy availability and pricing. Manufacturers with diversified sourcing and design-for-supply resilience will de-risk delivery schedules.

Automation & data-centric testing: Test-cell automation platforms and integration with vehicle-in-the-loop (VIL) and hardware-in-the-loop (HIL) solutions are becoming standard expectations for large validation programs.

The market structure combines global engineering powerhouses, specialist dyno manufacturers and agile regional providers. A moderate concentration among the top vendors means that competitive advantage is being built through differentiated test-system architectures, software ecosystems and integrated services rather than pure price competition.

AVL List GmbH (Graz, Austria): Known for high-precision electric and hybrid test systems and modular powertrain validation platforms. AVL’s strength is in end-to-end validation architectures for OEMs—this positions it well for large validation programs where integration and precision are prioritized.

HORIBA Ltd. (Kyoto, Japan): Offers broad chassis and engine dyno lines, including systems designed for high-volume simulated-distance testing. HORIBA’s capability to support large annualized test kilometer simulations speaks to customers with extended durability and regulatory test requirements.

Mustang Dynamometer (Twinsburg, OH): Specialist in eddy-current chassis dynos, with a strong performance and AWD emphasis. Mustang’s recent product refreshes reinforce its position in performance, aftermarket and motorcycle segments.

SuperFlow and Dynojet Research: These companies continue to dominate performance-tuning and workshop-focused dyno segments, with differentiated braking technologies and user ecosystems adopted by tuners and specialty shops.

Rototest and Meidensha: Focused on high-power hub-coupled systems and permanent magnet solutions for EV/HEV validation, addressing the growing need for in-wheel, high-power road-load simulation.

Power Test, SAKOR/Dyno One, Taylor and others: These vendors have demonstrated momentum through facility investment, brand integrations and product-line consolidation—moves that expand production capacity, service reach and automation capabilities.

Facility investments and capacity expansions announced in 2025 indicate supply-side confidence in mid-term demand—an early signal for procurement teams to plan multi-year test program pipelines and negotiate lead-time protections.

New product catalogs and brand integrations reflect faster product refresh cycles and consolidation; OEM procurement teams should treat vendor roadmaps as part of their supplier selection criteria, not just present-spec price lists.

Interoperability with industry automation standards (e.g., STARS for RDE cycles) and the rise of integrated test automation platforms mean buyers should insist on compatibility and upgrade paths when specifying new dyno purchases.

Prioritize modularity and software maturity: Procure test systems that decouple mechanical capacity from software control. This reduces the risk of obsolescence as validation protocols evolve.

Adopt a staged-capex approach: For large validation centers, phase investments with conversion-ready footprints (allowing for additional motor stands or power modules) rather than monolithic single-purpose builds.

Lock in service-level agreements and spare-parts contracts early: Given extended lead times for specialized dyno components, a strong aftermarket agreement materially reduces downtime risk for program schedules.

Negotiate data and IP terms: Ensure that test-data ownership and rights for model training are clearly specified—data-centric services are rapidly becoming a monetizable asset for both vendors and customers.

Consider bolt-on acquisitions for capabilities gaps: Target firms offering test automation, EV motor stands or regional service networks where rapid capacity ramp-up is critical.

Stress-test validation pipelines against regulatory and supply shocks: Use scenario planning to test the resilience of test schedules and procurement lead times under accelerated regulation or material shortages.

Detailed market-sizing models and transparent methodology spanning 2020–2025 (historical) and 2026–2032 (forecast), including scenario runs and sensitivity analyses.

Vendor heatmaps and scoring frameworks that evaluate technical breadth, software capability, service footprint and supply resilience to support RFP shortlists.

CapEx and TCO templates tailored for chassis, engine and hub-dyno deployments—designed for procurement and finance teams to plug into business case models.

Operational playbooks: workshop layouts, test-cell automation architectures, calibration and accreditation checklists.

Strategic M&A screening criteria and a short list of target archetypes for bolt-on growth by capability and geography.

Risk register and mitigation options for raw-material exposure, regulatory timing, and technology obsolescence.

Note: This preview outlines directional insights and practical tools. The full report contains the granular segmentation, regional and application-level forecasts, and vendor share tables that operational teams require to execute procurement and investment plans—access details are available on our publication page.

For organizations making 2026 decisions, the question is no longer whether to invest in dyno-capability—but when, where and how to structure those investments to maximize flexibility and limit obsolescence. The market’s steady mid-single-digit growth masks pockets of rapid change driven by electrification, regulation and automation. Senior leaders should treat dyno infrastructure as a strategic asset: align procurement cycles with product roadmaps, secure service and data contracts up-front, and prioritize vendors with demonstrable upgrade paths for EV and automated test platforms. PW Consulting’s full study provides the granular templates, vendor scorecards and scenario outputs needed to convert these strategic imperatives into procurement-ready decisions.

To obtain the full dataset, vendor matrices and forecast-by-segment, please consult the report landing page for subscription and licensing options.

For detailed analysis of this topic, please visit the official page:Automotive Dyno Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com