Tetrabromobisphenol‑A (TBBPA) Market — Strategic Outlook for 2026 Decision‑Makers

PW Consulting’s Tetrabromobisphenol‑A (TBBPA, CAS 79‑94‑7) market study is designed as a decision‑grade tool for corporate leaders making capital, procurement, regulatory and portfolio choices in 2026. Anchored on a base year of 2025 and a forecast window through 2032, the analysis synthesizes historical movement (2020–2025), supply‑side dynamics, regulatory inflection points, and scenario‑based demand modelling. At the macro level, the market is on a steady upward trajectory — expanding from a mid‑single‑hundreds figure in 2020 to a base‑year position in 2025, and continuing to grow at a compound annual growth rate of 5.1% through the forecast period to 2032 — underlining durable end‑market demand even as input costs and regulatory attention rise.

Tetrabromobisphenol-A (TBBA) (CAS 79-94-7) Market

Why this study matters for strategic decisions in 2026

- Timing of investment and capacity: Procurement teams and manufacturing planners need granular, forward‑looking signals to decide whether to secure long‑term supply, accelerate localised capacity, or lean on contract manufacturing.

- Regulatory and compliance risk: With fresh regulatory moves in major jurisdictions, companies require an integrated compliance roadmap that aligns testing obligations, reporting cadence and product stewardship with commercial timelines.

- Margin and pricing strategy: Volatile upstream costs and fluctuating spot markets mean commercial leaders must adopt hedging, indexed pricing and supplier diversification strategies to protect margins.

- M&A and partnership prioritisation: The market’s structure and the competitive map indicate targeted opportunities for bolt‑on acquisitions and strategic partnerships; analysts and corporate development teams need valuation drivers and a shortlist of operational gaps to pursue.

Market trajectory and key dynamics

Our model combines historical observations and bottom‑up supply modelling to map the TBBPA value chain from bromine feedstock through finished flame‑retardant formulations. After a period of steady recovery and demand growth in the early 2020s, the market reached a substantial base in 2025 and is projected to continue expanding at c.5.1% CAGR through 2032. Growth is being driven by continued electrification, high‑performance plastics demand, and ongoing fire‑safety regulations in electronic and automotive systems.

Tetrabromobisphenol-A (TBBA) (CAS 79-94-7) Market

That positive demand backdrop is being tested by three contemporaneous forces:

Tetrabromobisphenol-A (TBBA) (CAS 79-94-7) Market

- Regulatory momentum and uncertainty. European and North American regulators have taken differing stances: the European Commission concluded its RoHS deliberations and withdrew proposals to restrict TBBPA late in 2024, while the US EPA issued a final TSCA test rule in mid‑2025 requiring manufacturers and processors to perform chemical fate and transport testing. Separately, the European Food Safety Authority updated its 2024 opinion and reported no dietary exposure health concern based on revised occurrence data. These outcomes create a mixed regulatory landscape — reduced restriction risk in certain regions but heightened testing and reporting obligations in others.

- Upstream feedstock pressure. Interrupted brine extraction and logistical constraints tightened bromine availability in 2024, producing a notable year‑over‑year price increase for bromine feedstock and wide volatility in finished TBBPA spot levels. The result: compressed differentials and squeezed producer margins during cycles of high utilisation.

- Supply‑side configuration and capacity moves. The value chain shows a blend of vertically integrated incumbents and regional exporters. Producers with bromine integration or diversified bromine derivatives portfolios tend to manage margin volatility better and prioritize low‑emission product grades for sensitive applications such as electronics and polycarbonates.

Competitive landscape — who matters and why

The TBBPA industry is characterised by a modest degree of concentration: the largest three producers capture a significant but not dominant share of the market, and the top five raise that aggregate only incrementally — a structure that favours both regional champions and specialised exporters. This mix creates both competitive intensity and pockets of stable supply for buyers prepared to invest in long‑term contracts.

- Albemarle Corporation (Charlotte, NC, USA) — Offers vertically integrated bromine‑to‑TBBPA supply with tiered product grades aimed at electronics and polycarbonate users. Their emphasis on lower‑emission grades and multi‑regional production provides a risk‑mitigating model for global OEMs.

- ICL Industrial Products (Israel) — One of the largest bromine‑based producers with strategic capacity expansions in Israel and Europe. ICL’s scale and breadth of bromine derivatives make it a pivotal supplier for customers seeking continuity across multi‑site manufacturing footprints.

- Jordan Bromine Company (Safi Valley, Jordan) — Notable for bromine recovery initiatives and facility expansions focused on electronics and plastics markets. Its resource‑centric position provides competitive feedstock economics and long‑term security for customers sourcing from the Middle East.

- Shandong Moris Tech Co., Ltd. (Weifang, Shandong, China) — A Chinese manufacturer and exporter serving epoxy resin and PCB markets. Their cost structure and export orientation make them a go‑to partner for regional converters and downstream formulators.

- Shandong Tianyi Chemicals Co., Ltd. (Weifang, Shandong, China) — An integrated producer of TBBPA and related bromine derivatives with global supply relationships in electronics and automotive flame‑retardant chains; notable for its vertical integration and proactive product development.

Each of these players exhibits different strengths — integration, scale, low‑emission product development, or regional cost advantages — and the choice of supplier should align with a buyer’s tolerance for regulatory risk, logistical exposure and sustainability requirements.

What the full PW Consulting report delivers (practical, actionable content)

- Macro market sizing and trajectory (2020–2025 historical series and 2026–2032 forecast), with scenario variants tied to regulatory and feedstock shocks.

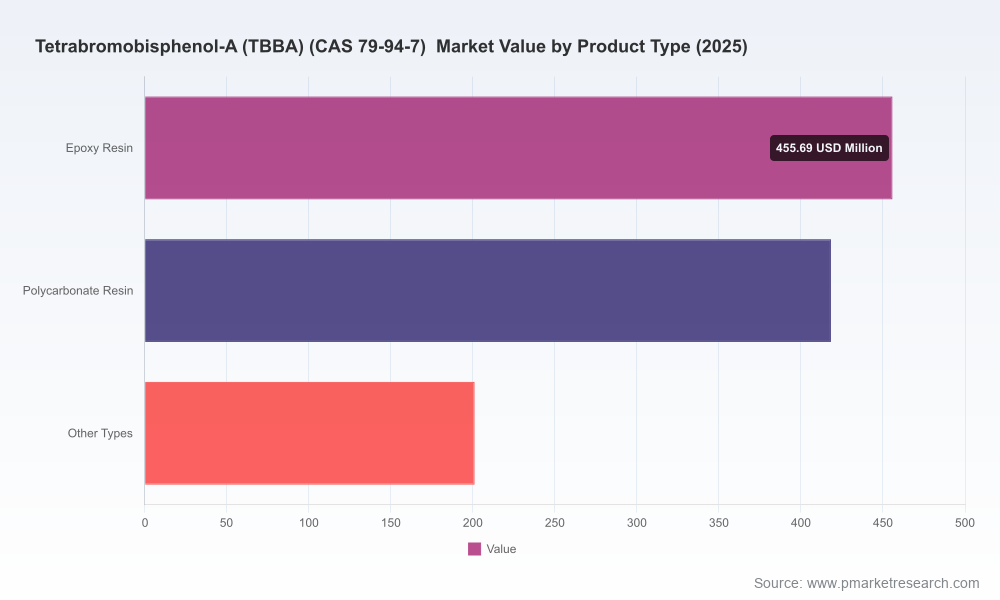

- Detailed segmentation by region, product type and application — including a downloadable data appendix with tables and charts. (Note: segment‑level tables are available in the full report.)

- Price and margin models integrating spot, contract and feedstock price paths, plus sensitivity analyses to test price pass‑through strategies.

- Supply‑side modelling: plant‑level capacity, utilisation forecasts, and a supplier risk heatmap covering geopolitical, logistics and environmental exposures.

- Regulatory tracker and compliance playbook: timelines for TSCA testing obligations, implications of the EC decision on RoHS deliberations, and how EFSA’s update affects reputation risk management.

- Competitive benchmarking and M&A screening: valuation levers, operational synergies, and an actionable shortlist of targets and partners for bolt‑on growth.

- Commercial playbooks for procurement, pricing, and product portfolio management, including play‑by‑play actions for 90‑, 180‑ and 365‑day horizons.

- R&D and substitution risk assessment: where low‑halogen alternatives create disruption risk and which applications are most exposed over the medium term.

How to use this research to shape 2026 corporate actions

- Procurement and hedging: use our forward price decks and feedstock scenarios to set contract tenors and indexation formulas that minimise cost exposure through 2027–2028.

- CapEx and footprint decisions: align greenfield or debottleneck investments to forecasted demand nodes and supplier availability, and apply PW’s capacity stress tests to defend timing decisions.

- Regulatory preparedness: incorporate the TSCA testing timetable into product development and compliance budgets, and treat the EFSA and EC outcomes as inputs to regional go‑to‑market priorities.

- M&A and partnerships: prioritise targets that fill capability gaps (e.g., bromine integration, low‑emission grades, regional distribution networks) and use our valuation sensitivity matrices to set bid/ask ranges.

- Product and portfolio strategy: segment downstream customers by substitution risk and regulatory exposure; target premium, low‑emission formulations for high‑value electronics while planning for longer‑term transitions in exposed applications.

- ESG and disclosure: prepare investor‑facing narratives that reconcile product stewardship, testing commitments and circularity initiatives, using PW’s compliance roadmap as a starting point for external disclosures.

Final perspective — opportunity, risk, and the next move

TBBPA remains a strategically important flame‑retardant in several high‑growth industrial ecosystems. The market’s steady CAGR and projected upwards trajectory through 2032 signal commercial opportunity, but real value in 2026 will accrue to organisations that marry supply‑chain resilience with regulatory foresight. Pw Consulting’s study is structured to move beyond descriptive analysis — it prescribes precise actions for procurement, regulation, investment and portfolio management while preserving detailed segment intelligence behind the paywall to protect decision advantage.

For supply chain directors, corporate development teams, and product leaders, the central question in 2026 is not whether TBBPA demand persists, but how to balance longer‑term strategic positioning against near‑term cost volatility and regulatory testing obligations. Our report translates those trade‑offs into concrete operational steps and a prioritised roadmap so your organisation can act with speed and confidence.

Next step

Access the full PW Consulting TBBPA market study to retrieve the segment‑level tables, regional and application breakdowns, producer price decks, and the supplier heatmap that inform the strategic playbooks summarised here. The full dataset and appendices contain the granular inputs you’ll need to operationalise these recommendations and to validate investment and procurement scenarios for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Tetrabromobisphenol-A (TBBA) (CAS 79-94-7) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com