Hidden Productivity Gaps an Employee Monitoring Tool Can Reveal

Other |

2026-07-11 05:52:49

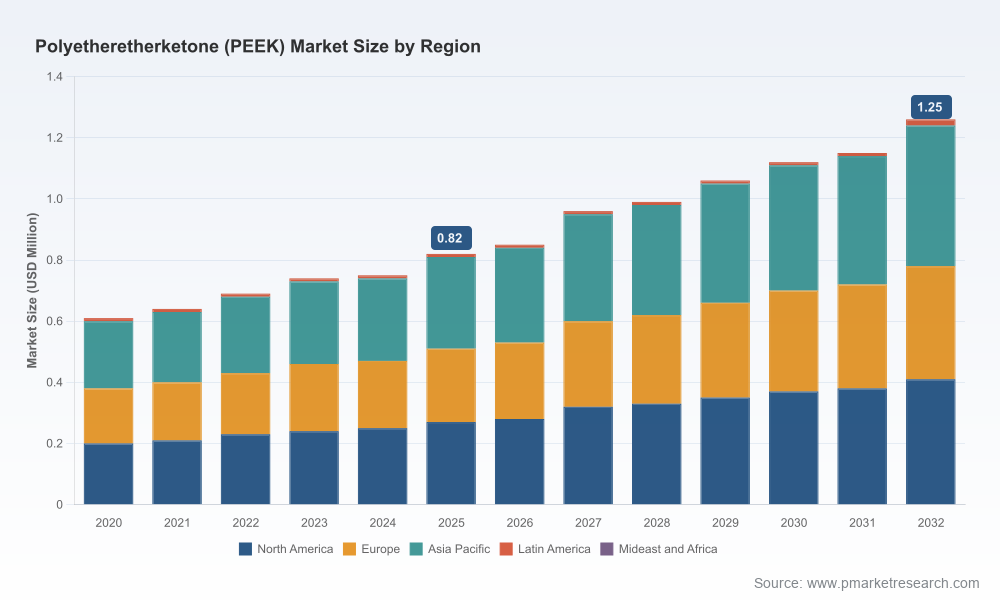

Polyetheretherketone (PEEK) has entered 2026 as a mature but still dynamic specialty polymer market. Our base-year assessment (2025) shows the market at USD 0.82 Million (revenue unit: Million USD), reflecting steady expansion from the 2020–2025 historical period. Under conservative-to-moderate demand scenarios, we model a compound annual growth rate (CAGR) of 6.3% across the 2026–2032 forecast window, with the market approaching roughly USD 1.25 Million by 2032 under the central case. These headline numbers belie important inflection points — material innovation, supply-chain stratification, and end-market reconfiguration — that will determine winners and losers through the next planning horizon.

Polyetheretherketone (PEEK) Market

Timing investment. The current growth profile supports targeted capacity investments and selective vertical integration but cautions against indiscriminate greenfield builds. With demand growth steady rather than explosive, capital deployment must be paired with product differentiation (e.g., lower-melt PAEK variants, medical-grade formulations) and offtake certainty.

Polyetheretherketone (PEEK) Market

Supplier selection and risk management. Raw material geopolitics — notably supply security for the 4,4'-DFBP precursor — continues to favor vertically integrated or long-contracted suppliers. Companies initiating or renewing sourcing contracts in 2026 should build dual-sourcing, buffer capacity, and precursor contingency clauses into contracts.

Polyetheretherketone (PEEK) Market

Technology-led differentiation. New grades that expand processing windows and lower melting points (e.g., LMPAEK variants) materially reduce manufacturing complexity for high-value applications such as aerospace and advanced energy systems. Adopting these materials early can shorten qualification timelines and lower conversion costs.

Commercial strategy for chargeable performance. PEEK’s premium positioning means customers increasingly pay for validated performance, not just raw resin. Go-to-market models that combine technical support, certification roadmaps (especially for aerospace and medical), and local compounding capabilities will capture disproportionate margin.

PW Consulting’s market study is structured to move beyond descriptive market sizing into operational decisions executives must make in 2026. Key practical outputs include:

Top-down and bottom-up market sizing (base year 2025; forecast 2026–2032) with scenario variants tied to aerospace cycle, automotive electrification, and medical implant adoption.

A supplier risk heatmap that quantifies exposure to precursor shortages, single-source dependencies, and logistic chokepoints, together with contractual mitigations and inventory strategies.

Technology adoption playbooks for LMPAEK and other low-melt PAEK variants, including processing parameter windows, expected yield improvements, and qualification timelines for regulated sectors.

Commercial due diligence templates for M&A and joint-venture evaluation — EBITDA sensitivity matrices, working-capital profiles, and integration risk checklists tailored to PEEK producers and compounders.

Competitive profiles and strategic moats for leading suppliers, including capacity trajectories, vertical integration benchmarking, and partnership ecosystems (e.g., additive-manufacturing alliances).

Scenario-based pricing and margin forecasts linked to feedstock shocks, capacity additions in low-cost regions, and product mix transitions toward compounded and functionalized grades.

Actionable recommendations for procurement, R&D prioritization, and commercial pilots that reduce time-to-revenue for new grades and applications.

The PEEK market sits in a moderately concentrated industry structure, with the top three players commanding a strong share of global sales and the top five widening that footprint. High barriers to entry — chain-specific feedstock supply, high-capital polymerization assets, and rigorous application qualifications — preserve incumbent advantages. Key company dynamics to watch in 2026:

Victrex plc — Continues to lead on brand, aerospace-qualified grades, and ongoing material innovation. Recent LMPAEK introductions and award-winning thermoplastic composites work highlight a shift toward lower-processing-cost, higher-performance solutions that accelerate qualification in aerospace programs. Strategic partnerships with additive-manufacturing specialists deepen their systems capability beyond resin supply.

Solvay S.A. — Maintains strength in high-temperature grades and pushes into medical-focused formulations with engineered glass-filled variants emphasizing biocompatibility and radiolucency. Expect Solvay to leverage cross-business synergies to fast-track implant-grade certifications and premium positioning.

Evonik Industries AG — Plays a pivotal role in compounding and regional footprint expansion, especially in Asia. Their focus on tailored compounds and close customer support positions them as a preferred partner for product developers needing engineered semi-finished forms.

Arkema — Competes by broadening the PAEK family offer (e.g., PEKK/Kepstan) and backing additive-manufacturing use cases for extreme-environment applications. Expect Arkema to push for design wins where PEKK/PEEK performance trade-offs favor their portfolio.

Chinese and regional producers — Several China-based players have materially increased capacity and distribution networks, with an emphasis on medical-grade resins and cost-competitive filled compounds. Their scale and proximity to key manufacturing ecosystems are reshaping commercial negotiations.

Specialist compounders and semi-finished providers — RTP, Ensinger and similar players fill an important layer, enabling customers to access bespoke PEEK compounds and CNC/extruded components without upstream polymer investment. These providers are critical partners for OEMs seeking rapid prototyping and small-batch qualification.

Raw material concentration: Precursor supply (4,4'-DFBP) remains a structural risk. Companies that control upstream access or that have hedging mechanisms enjoy a durable cost advantage and fewer production interruptions.

Regulatory and sustainability narratives: PEEK’s status as PFAS-free in unfilled polymer manufacture represents a competitive sustainability claim that can be deployed in regulated procurement (medical, aerospace, certain public tenders).

Processing innovation: LMPAEK-type grades lower the barrier for established plastics converters to run PEEK-like performance materials on conventional equipment. This expands the addressable market by removing processing as the primary gating factor.

Geopolitical shift in capacity: Ongoing expansions in Asia are changing supply economics — Chinese PEEK production exceeded 15,000 tons per year in 2026 — which increases supply flexibility but also introduces pricing pressure on commodity grades and accelerates regional competition for higher-margin compounded products.

Industry concentration: The market exhibits significant concentration among a few global players (the top three and top five have substantial combined shares). This favors strategic partnerships with incumbents for access to certification pathways and advanced grade roadmaps.

Sourcing: Execute flexible long-term agreements with tiered volume/price bands tied to precursor indices and include capacity-release options. Prioritize partners with demonstrated vertical integration or precursor access.

Product strategy: Accelerate trials of LMPAEK and low-melt PAEK variants in applications where qualification time is a barrier. Bundle material supply with design-qualification services to justify premium pricing.

Manufacturing footprint: For OEMs, favor co-located compounding or contract manufacturing to shorten qualification loops. For producers, favor modular capacity additions and third-party compounding partnerships to broaden market reach without full vertical upstream builds.

M&A and alliances: Target compounders, semi-finished providers, or AM specialists to acquire near-term revenue and customer access rather than large, risky polymerization assets unless precursor security can be guaranteed.

Commercial models: Implement value-based contracts in key verticals (aerospace, medical) that reflect certification, traceability, and lifecycle performance rather than per-kilogram pricing alone.

For executives preparing 2026 budgets and three- to five-year plans, the most immediate value of our PEEK study is in converting market signals into operational decisions: which grades to prioritize for qualification, where to secure feedstock and compounding capacity, and how to structure commercial offerings that capture technical premium. Use the report’s scenario models to stress-test capital plans against precursor shocks, new-grade adoption rates, and regional capacity additions. Leverage our supplier risk heatmap when negotiating renewal contracts this year to eliminate blind spots in your supply strategy.

We have deliberately preserved the granular, proprietary splits and detailed financial templates for report subscribers. If your objective is to move from strategic intent to executable plan — supplier contract clauses, sample-qualification roadmaps, and a prioritized list of near-term pilot opportunities — our full market study and supporting workstreams will provide the operational playbooks and models to act in 2026 with confidence.

For detailed analysis of this topic, please visit the official page:Polyetheretherketone (PEEK) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com