Is Your Drinks Vending Machine in Fort Lauderdale Meeting Modern Demands?

Other |

2026-04-29 07:21:50

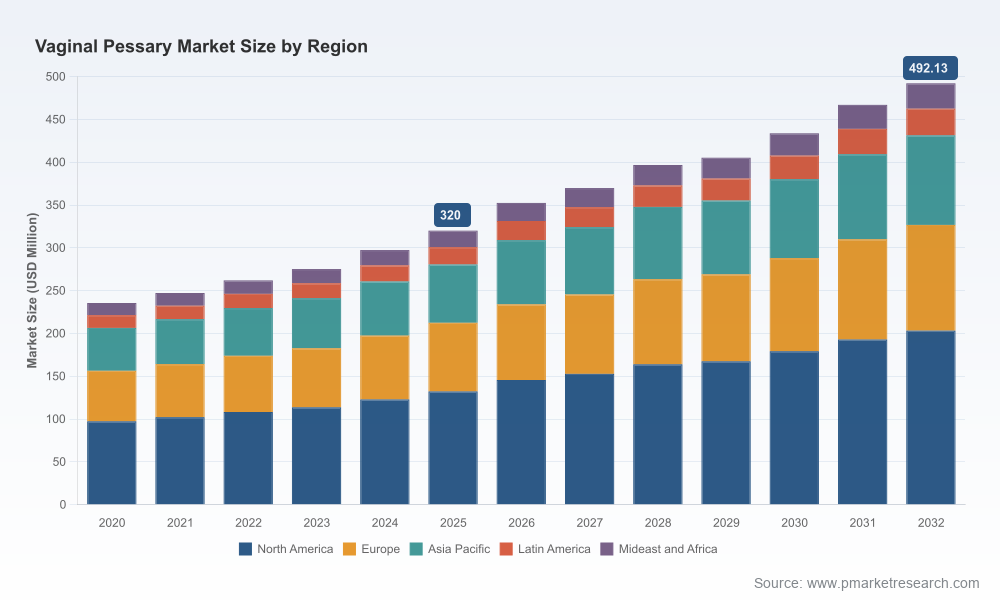

As health systems, device manufacturers, and private equity evaluate priorities for 2026, the vaginal pessary market presents a clear, actionable growth opportunity driven by clinical practice shifts, device innovation, and evolving reimbursement levers. Our PW Consulting market study (base year 2025; forecast 2026–2032) quantifies this trajectory and synthesizes the tactical playbooks leaders will need. At a macro level, the market expanded meaningfully through the first half of the decade — rising from roughly USD 235 million in 2020 to about USD 320 million by 2025 — and PW Consulting’s scenario analysis points to continued expansion through 2032 at a compound annual growth rate of 6.5%, underpinned by product diversification, new distribution models, and incremental reimbursement tailwinds.

Vaginal Pessary Market

Timing and runway: With market growth forecast accelerating in the second half of the decade, 2026 is the pivotal year for companies to convert innovation and regulatory wins into commercial scale. Decisions made in 2026 — on product portfolio, regulatory submissions, and go-to-market investments — will determine market share trajectories across the forecast period.

Vaginal Pessary Market

Clinical and channel inflection: The emergence of physician-prescribed, at-home disposable devices and recent FDA 510(k) activity are shifting how pessaries are delivered, adopted, and reimbursed. Manufacturers that align clinical evidence strategies with new distribution models will shorten conversion cycles and lower acquisition cost per patient.

Vaginal Pessary Market

Reimbursement differentiation: HCPCS Level II codes and procedure coding dynamics materially affect revenue per unit and commercial economics. Understanding the payer landscape and the practical implications of codes for rubber versus non-rubber devices is essential to setting pricing and contracting strategies.

Market sizing and validated growth scenarios — full historical series and three forecast scenarios through 2032 to stress-test investment cases.

Commercial playbooks — go-to-market segmentation by clinician specialty, clinic procurement patterns, and multi-channel distribution strategies for hospital, ASC, and direct-to-consumer pathways.

Regulatory and reimbursement checklists — 510(k) pathway templates, GMP readiness, and payer-claim examples mapping HCPCS and CPT code interactions to revenue outcomes.

Product and materials decision matrix — decision support for PVC vs. silicone and disposable vs. reusable formats, including lifecycle cost, sterilization constraints, and user adherence considerations.

Competitive benchmarking & partner playbook — capability maps, supplier scorecards, and M&A target screening criteria tailored to acquirers or licensing partners.

Clinical-evidence roadmap — prioritized clinical studies and real-world evidence designs to maximize label expansion and prescriber confidence.

Note: The preview intentionally omits detailed segment-level tables (regional/application/type splits and price decks) to preserve the report’s proprietary value. Clients can access the full segmentation matrices, unit forecasts, and price-volume curves via the report download portal.

Product innovation is reconfiguring care pathways. The commercial launch of physician-prescribed, at-home disposable ring pessaries in the U.S. during late 2024 materially changes the adoption calculus: single-use convenience, reduced clinic visit burden, and a pathway for physicians to prescribe rather than fit in-clinic are all now proven commercial options.

Regulatory activity is enabling competition. A wave of 510(k) clearances in 2024 broadened the set of clinically validated device designs, lowering barriers for new entrants and supporting claims that emphasize ease-of-use and reuse safety. Companies that accelerate submissions in 2026 can exploit a window of elevated clinician receptivity.

Reimbursement nuance will determine realized ASPs. HCPCS Level II codes still differentiate rubber from non-rubber devices — with corresponding differences in reimbursement and allergy risk profiles. Procedure and fit coding (CPT 57160 and common billing modifiers) also influence the economics of follow-up and annual care, affecting the total revenue opportunity per patient.

Material choices are a strategic lever. PVC remains attractive for low-cost, high-volume local practice, while silicone products command premium pricing and offer multi-year reuse when intact. Device makers must align material strategy with target channel (e.g., institutional tender vs. consumer-directed) to optimize margins and procurement uptake.

The current market exhibits meaningful concentration among top players (CR3 ~52%; CR5 ~65%), but product breadth and distribution reach matters as much as installed market share. Key players profiled in our analysis include:

CooperSurgical (Connecticut, USA) — strong global distribution and a broad portfolio including multiple styles across ring, gellhorn, cube, and donut designs. Their established clinic supply relationships and payer knowledge make them a benchmark for scale commercialization.

MedGyn Products (Illinois, USA) — differentiated by comprehensive fitting sets used for diagnosis and short-term management; attractive for partners seeking deep clinician touchpoints and training-enabled adoption.

Bioteque America (USA) — niche advantage in silicone devices tailored for long-term reuse and cervical support; a relevant competitor for firms prioritizing premium product lines and durable goods economics.

Panpac Medical (Canada) — notable for FDA-cleared disposable and flexi-shelf options; their regulatory positioning supports cross-border commercialization strategies.

Cetro Medical & ConTIPI Medical (Israel) — examples of innovation-led entrants, with ConTIPI’s ProVate positioning as a physician-prescribed at-home disposable ring exemplifying an alternative route-to-market.

Thomas Medical (Indiana, USA) & Bray Group (UK) — legacy manufacturers with cost-competitive offerings and established regional distribution that matter for local procurement plays and hospital sourcing.

Recent strategic moves to watch: commercialization partnerships (e.g., companies selecting specialized commercialization service partners), targeted 510(k) clearances for novel delivery systems, and product launches oriented to at-home use. Together, these tactics compress time-to-adoption and put pressure on incumbents that rely on traditional clinic-fit models.

Prioritize product pathways by channel. Use our scenario outputs to decide whether to accelerate disposable, at-home formats (faster access, lower clinic friction) or to deepen premium, reusable silicone portfolios for higher ASP and loyalty.

Align regulatory sequencing with commercial launches. Plan 510(k) filings and supporting clinical studies to match target-market access timelines; secure GMP readiness for scale manufacturing prior to commercialization partnerships.

Refine pricing and contracting around coding realities. Model realized revenue under HCPCS and CPT coding permutations and build payer engagement plans that justify pricing differentials based on material, lifecycle, and allergy risk.

Build a distribution playbook for clinician enablement. Training kits, fitting sets, and bundled clinic programs accelerate conversion. Consider partnerships with commercialization specialists to scale physician outreach efficiently.

Evaluate M&A and licensing selectively. Use our supplier scorecards and financial stress-tests to prioritize tuck-ins that expand product breadth, add proprietary delivery systems, or enhance direct-to-consumer capabilities.

To preserve the proprietary value of PW Consulting’s work and to compel informed commercial conversations, this preview omits the granular segmentation tables (regional and application splits by value and volume), per-unit price decks, and detailed distributor margin models. These data sets are included in the full report and form the basis for executable P&L models, go-to-market ROI calculators, and M&A valuation templates we provide to clients.

For leadership teams preparing 2026 roadmaps, the full PW Consulting Vaginal Pessary Market study converts market direction into measurable go-to-market steps: validated demand curves, payer-aware pricing, regulatory milestones, and a competitor response playbook. If your 2026 strategy depends on capturing share in a market projected to grow at ~6.5% CAGR through 2032 — and on converting recent clinical and regulatory momentum into durable commercial advantage — our report is designed to reduce time-to-decision and to operationalize growth.

For detailed analysis of this topic, please visit the official page:Vaginal Pessary Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com