Compression Stockings Market — Strategic Preview for 2026 Decision‑Makers

As healthcare providers, manufacturers, and investors position for the next wave of demand and regulation, the compression stockings (elastic stockings) market presents a blend of steady expansion, concentrated incumbency and emergent tactical risks. This preview summarizes the strategic takeaways from PW Consulting’s full market study and explains why our findings should be a core input to 2026 planning cycles. In keeping with the “trailer” principle, we demonstrate the analytical depth and practical guidance you will find in the full report while deliberately withholding proprietary segment‑level tables and price‑by‑channel models that are available through our portal.

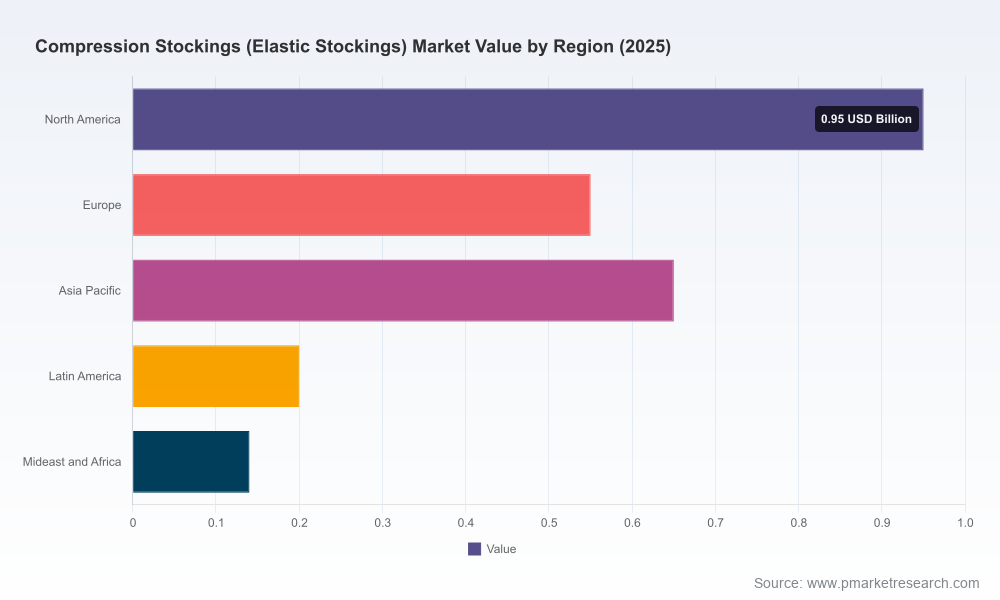

Compression Stockings (Elastic Stockings) Market

Market trajectory: steady growth with structural tailwinds

The global market has moved from a modest base in 2020 to a substantially larger industry by the mid‑2020s. Our model tracks the market at approximately USD 2.49 billion in the 2025 base year, and projects a continuation of expansion through the 2026–2032 forecast window, reaching roughly USD 3.69 billion by 2032. That trajectory corresponds to a compound annual growth rate (CAGR) of about 5.8% across the forecast period. The growth is neither hyper‑cyclical nor perfectly linear: it reflects steady demand driven by chronic disease prevalence, aging populations, expanded reimbursement in certain markets, and incremental product innovation (materials, knit technologies and comfort features).

Compression Stockings (Elastic Stockings) Market

For executives, the implication is clear: this is a growth market that rewards targeted investment and nimble commercialization. However, the pace of opportunity requires disciplined prioritization — advantages accrue to firms that align product development, channel strategy and regulatory readiness concurrently rather than sequentially.

Compression Stockings (Elastic Stockings) Market

Why the 2026 planning cycle matters

- Reimbursement windows are tightening. Recent and imminent updates to reimbursement codes and documentation rules require firms to be reimbursement‑ready as new policies take effect. For suppliers and distributors, missed coding or documentation shifts can translate immediately into lower uptake at the point of care.

- Certification and device classification are non‑negotiable. Compression garments are regulated as medical devices in major markets; FDA registration, ISO 13485 quality systems and CE marking are table stakes for broader market access and institutional procurement.

- Sustainability and circularity are emerging operational constraints. Regulations on textile waste and collection in certain markets create both compliance obligations and public relations opportunities for vertically integrated players and brands investing in closed‑loop programs.

- Product differentiation matters, but so does manufacturing agility. Knit technologies, fabric mixes and fit solutions are differentiators; yet the ability to scale new SKUs, manage lead times and maintain quality at volume will define winners.

What our full report delivers (practical, actionable content)

The study is designed as an execution guide — not merely an academic forecast. Highlights include:

- Market sizing and validated forecast models for 2026–2032, including scenario analyses that stress test demand under different reimbursement and supply‑disruption scenarios.

- Segmentation frameworks by product type, clinical application and region with elasticized models you can re‑run with your assumptions (note: segment‑level figures are reserved for report subscribers).

- Competitive benchmarking and capability heatmaps covering manufacturing, distribution reach, certifications and recent product initiatives.

- Regulatory and reimbursement playbooks, mapping the immediate actions needed to comply with major market updates and to capture reimbursement‑driven demand.

- Go‑to‑market playbooks for direct‑to‑clinic, retail and e‑commerce channels — including pricing levers, patient acquisition cost benchmarks and sample P&L scenarios.

- Supply chain and sourcing analysis, with risk scoring for critical inputs and partner‑selection criteria for nearshoring versus offshore manufacturing.

- M&A and partnership pipeline recommendations with prioritization criteria and a short list of capability gaps most likely to be value‑accretive.

- Appendices containing our primary research questionnaire, interview summaries, and the proprietary financial model used to produce the published forecasts.

Competitive landscape: incumbents, innovators and private‑label plays

The market exhibits moderate concentration: the three largest firms control a meaningful share of market value, and the top five amplify that concentration further. This structure produces a competitive environment where scale delivers negotiating power with distributors and payors, yet niche innovation can still capture premium segments.

Key profiles and strategic posture:

- Sigvaris Group (Switzerland) — An established medical device manufacturer emphasizing both flat‑knit and circular‑knit systems. Sigvaris positions itself around clinical efficacy and compliance; their product refresh cycles and portfolio investments are timed to retain institutional procurement relationships. Recent product introductions underscore a continued focus on clinical support and patient comfort.

- Medi USA (United States) — A market leader in therapeutic compression garments and a strong distributor in clinical channels. Medi’s approach blends clinical credibility with consumer‑oriented color and fit updates to broaden non‑prescription appeal while maintaining medical‑grade lines.

- Juzo (Julius Zorn Inc.) (Germany/US) — Known for knit innovation and latex‑free options, Juzo’s investments in proprietary knit technologies are illustrative of a strategy to reduce fitting returns and improve patient adherence.

- Bossong Hosiery (United States) — A private‑label manufacturer that serves retailers and healthcare channel partners. Their domestic manufacturing profile provides flexibility for buyers prioritizing near‑sourced supply, and they can be an attractive partner for firms seeking private label or capacity buffering.

- SUN POLAR (Taiwan) — A regionally competitive manufacturer with certifications and credentials aimed at export markets. Their recent customer satisfaction initiatives and quality emphasis are a playbook for OEMs targeting value‑sensitive institutional buyers.

Recent developments (selected): product launches and knit‑technology introductions across multiple vendors; customer satisfaction reporting focused on quality; monthly policy moves and annual reimbursement code updates that collectively change the near‑term commercial rhythm for suppliers and providers.

Regulatory and reimbursement dynamics to factor into 2026 decisions

- Compression garments are treated as medical devices in major jurisdictions — registration, ISO 13485 compliance and CE marking are prerequisites for institutional access and many supply agreements.

- Reimbursement policies are evolving: in several markets, coverage rules now explicitly require documentation and physician prescriptions for certain pressure ranges, and some payors introduced updated HCPCS codes effective with the 2026 policy cycle. Firms must align coding, instructions for use and clinician education to preserve capture rates.

- Waste and circularity regulations in targeted European markets are forcing players to adopt new packaging, collection and take‑back practices; manufacturers with early investments in circular design will find procurement doors opening in regulated municipalities.

Decision playbook — actions to take in 90 days, 12 months and 36 months

- 90 days (tactical): conduct a certification and reimbursement readiness audit; prioritize SKU and documentation updates for products affected by 2026 codes; engage top payors with evidence packages; and lock short‑term capacity options to hedge supplier disruption risks.

- 12 months (operational): roll out fit‑and‑comfort enhancements to reduce returns; deploy clinician education programs to increase adherence and prescribing; pilot direct‑to‑consumer channels for cosmetic/fashion lines while preserving clinical channels for medical‑grade garments.

- 36 months (strategic): assess manufacturing footprint optimization for nearshoring, acquire or partner to gain proprietary knit technologies or digital sizing capabilities, and implement circularity programs aligned to jurisdictional waste requirements to secure preferred procurement status in regulated public tenders.

Investment and M&A signals

Valuation discipline should emphasize profitable scale in direct clinical channels, IP around fit and materials, and capabilities in regulatory/compliance management. Targets that help compress time‑to‑market for new knit technologies, reduce fitting returns through sizing analytics, or provide payor access (e.g., distribution agreements with major rehabilitation networks) are high‑impact candidates. Private‑label capacity providers with domestic footprints are also strategic buys for manufacturers seeking resilience and shorter lead times.

Final observations — what distinguishes the winners

In a market that grows at a mid‑single‑digit CAGR, executional excellence is the differentiator. Winners will combine clinical credibility (evidence, certifications and clinician engagement), product differentiation that improves adherence (comfort, knit tech and fit), and operational resilience (flexible manufacturing and payor readiness). Sustainability and circularity will shift from optional to competitive advantage in select markets as regulatory burdens increase.

PW Consulting’s full study provides the validated data, playbooks and model‑ready spreadsheets that let leadership teams move from strategy to execution quickly. We intentionally limit the granular segmentation tables and proprietary scenario outputs in this preview — those elements are available to subscribers and enterprise clients who require the full analytical toolkit to underwrite investments, contracts and go‑to‑market commitments in 2026.

To convert the high‑level findings above into a 2026 action plan tailored to your organization (product roadmap, reimbursement tactics, or M&A prioritization), access the full report and model package on our research portal or contact PW Consulting’s Compression Stockings practice lead for a briefing.

For detailed analysis of this topic, please visit the official page:Compression Stockings (Elastic Stockings) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com