Ceiling-mounted Supply Pendants with Column Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s senior industry analyst, I present a forward-looking primer on the Ceiling-mounted Supply Pendants with Column market designed to orient procurement leaders, OEM strategy teams, facility planners, and investors as they set priorities for 2026. This piece is a high-fidelity “trailer” of our full market study: it demonstrates the depth of analysis and the strategic questions we answer, while preserving the granular segment-level tables and proprietary forecasts to encourage direct engagement with the complete report.

Ceiling-mounted Supply Pendants with Column Market

Why this market matters for 2026

Ceiling-mounted supply pendants with integrated columns are a quiet but critical enabler of modern acute-care workflows. As hospitals intensify efforts to maximize room utilization, minimize infection vectors, and improve clinician ergonomics, these systems increasingly influence both capital planning and clinical outcomes. For 2026, decisions about which platforms to standardize on — and how to spatially configure theatres and ICUs — will materially affect procurement cycles, installation timelines, and lifecycle service contracts across regional health systems.

Ceiling-mounted Supply Pendants with Column Market

Our study frames the market not as an equipment purchase but as a systems decision that touches clinical protocols, building infrastructure, regulatory compliance, and biomedical service models. That perspective is essential for executives considering multi-year capital programs or suppliers designing 360-degree service propositions.

Ceiling-mounted Supply Pendants with Column Market

Market snapshot (high-level)

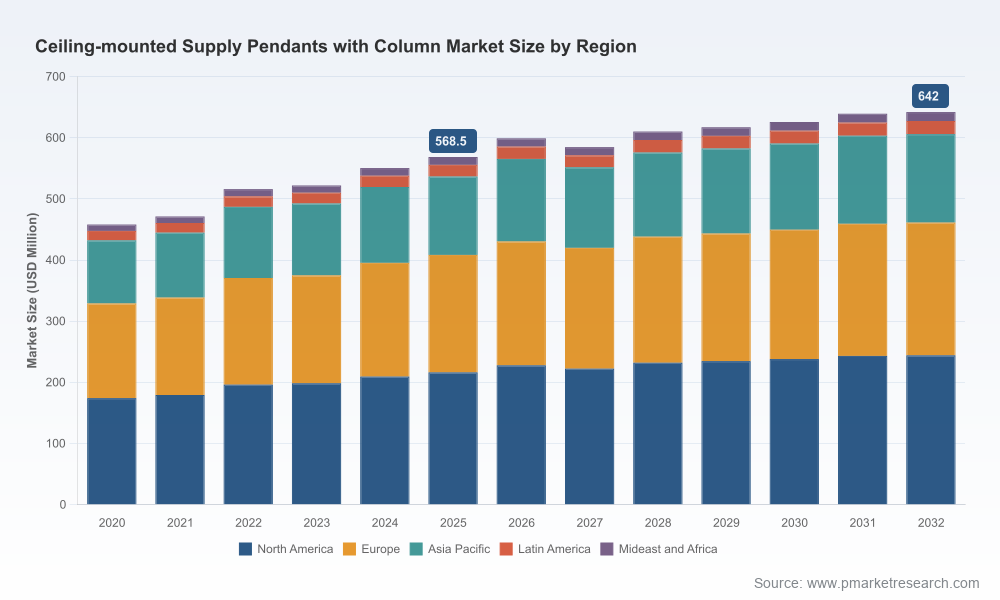

Using 2025 as the base year, the global market for ceiling-mounted supply pendants with columns has shown modest but steady expansion through the early 2020s, reflecting steady hospital investment in acute-care modernization. The market reached a mid‑single‑hundred‑million USD scale by 2025 and is projected to continue growing through the 2026–2032 forecast window at a compound annual growth rate of approximately 1.88%.

Key takeaways from the headline figures:

- Growth is steady rather than explosive—this is a replacement and optimization market driven by clinical needs and hospital capital cycles, not a nascent technology surge.

- Market concentration is moderate: the top three players account for under half of market revenues, and the top five approach roughly half the market, leaving space for focused regional and specialist entrants to compete on features and services.

- Forecasting through 2032 suggests incremental revenue expansion rather than a structural redefinition of the category; upside comes from modularization, retrofit demand, and integrated digital services rather than raw device unit growth alone.

Principal dynamics shaping 2026 decisions

Four broad forces will determine winners and losers in procurement and product strategy next year:

- Regulatory and safety standards. The recent updates to NFPA 99 (2024) influence how manufacturers design gas and vacuum routing in ceiling pendants, impacting installation scope and compliance costs. Procurement teams must factor regulatory rework into total project timelines.

- Clinical workflow optimization. Evidence-based room layouts and the drive to reduce floor clutter continue to push facilities toward ceiling-mounted systems. Decisions are increasingly driven by multidisciplinary teams (clinicians, architects, biomedical engineers) rather than purchasing alone.

- Materials and longevity. Corrosion-resistant alloys and refined finishings have become baseline expectations in acute-care environments. Suppliers that can demonstrate lifecycle resilience and low maintenance overhead capture preference among facilities operating constrained service budgets.

- Reimbursement and procurement incentives. Hospital procurement policies show a clear bias toward modular systems that enable flexibility across care settings. Bundled procurement — equipment plus long-term maintenance — is becoming the dominant contracting model for larger health systems.

Technology and product trends to watch

The next 18–36 months will see several convergent product trends:

- Modular and motorized movement: Systems offering motorized vertical travel, flexible articulation, and modular accessory ecosystems reduce installation complexity and enable faster room reconfiguration.

- Integrated service platforms: Value-add comes from integrated electrical, gas, data, and light systems that reduce coordination risk during installation and lower downstream service touchpoints.

- Sensorization and IoT readiness: Sensor-integrated pendants that provide usage data, preventive maintenance alerts, and compatibility with hospital asset-management systems will differentiate higher-end offerings.

- Space-optimized designs: For facilities with retrofitting constraints, compact column configurations and non-rail motorized solutions are attractive for reducing ceiling penetrations and construction work.

Competitive landscape — who is shaping supply and innovation

The category combines established medical-equipment players with specialized manufacturers focused on pendants and service columns. Our assessment of public and primary-source intelligence highlights the following strategic profiles:

- Drägerwerk AG & Co. KGaA (Lübeck, Germany): Offers modular ceiling-mounted supply units optimized for acute care and surgical workstations. Their Ambia® and Polaris® families emphasize integration and clutter-free setups, targeting customers prioritizing system consistency and regulatory compliance.

- Tedisel Medical S.L. (Badalona, Spain): Known for motor-column and non-motorized pendants with motorized vertical movement and space-saving designs that avoid ceiling-track constraints — a strong choice for retrofit projects and modular ICU configurations. (Notably launched a new Galaxy system in March 2025 aimed at modular ICU setups.)

- Starkstrom (Germany): Focused on clinically robust pendants with mechanical reliability (e.g., pneumatically braked lateral movement) and service column designs that appeal to critical-care and OR environments where durability and predictable movement are essential.

- Novair Medical (Spain): Competes on flexible configurations for space-constrained facilities and integrates medical gas management to streamline installations in older buildings.

- Brandon Medical (UK): Brings sensor-integrated options and project experience in complex hospital builds; recently supported a major NHS surgical unit project in 2025, illustrating their capability in turnkey theatre deliveries.

- KLS Martin SE & Co. KG (Germany): Positions for OR flexibility with swiveling pendants and high maneuverability, a good fit for surgical suites with demanding positioning requirements.

- Maquet (Getinge AB — Sweden/Germany): Leverages integration with surgical lights and workstation systems, appealing to large hospital groups seeking consolidated vendor partnerships.

These vendors differ in their go-to-market: some compete on hardware robustness and service reliability, while others emphasize modularity and integration with digital asset-management systems. Market concentration metrics reinforce that while established players capture significant shares, there remains room for niche innovation and targeted regional strategies.

Strategic implications for OEMs, hospital systems, and investors

- For OEMs: Prioritize modular platforms that minimize installation time and provide clear total-cost-of-ownership (TCO) advantages. Developing retrofit-friendly solutions and scalable service plans will accelerate adoption in mature markets.

- For hospital systems: Treat pendants and columns as systems investments linked to operational workflows. Early involvement of clinical engineering and facilities in vendor selection reduces downstream change orders and compliance risk.

- For investors: Focus on companies with recurring-service revenue models and demonstrable strength in retrofit projects or large-scale system integrations—those attributes correlate with higher margins and defensible pipelines.

What the full PW Consulting report delivers (practical, actionable content)

Our comprehensive study equips decision-makers with tools they can deploy immediately during 2026 planning cycles:

- Multi-year demand model with scenario sensitivity for retrofit versus new-build pathways across the forecast period.

- Supplier benchmarking with feature-capability scoring, installation footprint analysis, and service-cost comparison frameworks (note: granular market-split tables are reserved for the full report).

- Procurement playbook templates: RFP structure, evaluation scoring matrices, and sample contract language for bundled maintenance agreements.

- Case studies and implementation timelines for representative hospital archetypes (tertiary surgical centre, regional hospital, modular ICU deployments).

- Technical appendix: compliance checklist mapped to NFPA 99:2024 changes, materials selection guidance, and recommended interoperability tests for sensorized pendants.

How to use these insights in 2026 planning

Leaders crafting 2026 capital budgets should treat ceiling-mounted supply pendants with columns as a near-term lever to improve clinician throughput and reduce operational friction. Recommended next steps:

- Run a rapid room-assessment pilot in two facility types (one retrofit, one new-build) to quantify installation variability and actual downtime exposure.

- Solicit vendor proposals that include lifecycle service pricing and IoT-integration pathways; compare offers on TCO rather than upfront price alone.

- Map regulatory compliance tasks early: assign responsibility for NFPA 99 validation and document readiness as part of any procurement timeline.

Where this trailer leads

The analysis above surfaces the macro drivers, competitive archetypes, and practical actions that will matter in 2026. The complete PW Consulting report contains the proprietary segment-level figures, pricing benchmarks, and region-by-application breakdowns that operational teams require to finalize supplier selection and capital commitments. If you are preparing an RFP, designing a retrofit plan, or assessing M&A targets, the full report provides the granular inputs and executable templates to move from strategy to procurement rapidly.

To obtain the detailed datasets and the full strategic playbook, please contact PW Consulting. Our specialists are ready to support tailored briefings, model custom scenarios, and integrate findings with your existing capital and clinical plans.

For detailed analysis of this topic, please visit the official page:Ceiling-mounted Supply Pendants with Column Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com