Hot Stamping Foil Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As companies plan capital allocation, product development and supply-chain adjustments for 2026, the hot stamping foil market presents a mix of steady market expansion, discrete consolidation and intensifying regulatory pressure. This preview summarizes the strategic value of our full Hot Stamping Foil Market study (base year 2025; historical 2020–2025; forecast 2026–2032) and explains how leading and fast-follower firms can translate macro trends into competitive advantage. The analysis is driven by the market’s trajectory — a projected compound annual growth rate (CAGR) of 5.7% over the forecast window — and a detailed review of technology, raw-material exposure and regulatory headwinds shaping supplier economics and buyer choices.

Hot Stamping Foil Market

Market trajectory in context

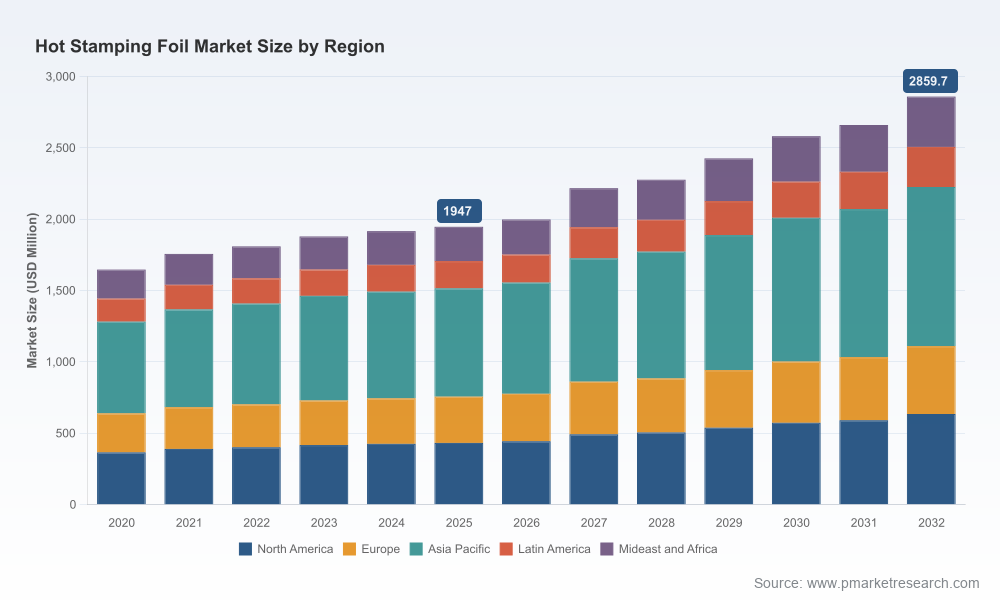

Measured in USD million, the industry expanded from a 2020 base and reached approximately 1,947 million in 2025. Under our central forecast — which incorporates price, mix and volume dynamics across packaging, graphics and industrial applications — the market is projected to continue its steady climb, approaching a substantially higher run-rate through 2032. The 5.7% CAGR embedded in our baseline scenario reflects combined tailwinds from premiumization in packaging, growing demand for decorative and security foils, and incremental adoption of specialized grades across textiles and technical markets.

Hot Stamping Foil Market

Two implications are immediate for decision-makers planning in 2026:

Hot Stamping Foil Market

- Volume growth is predictable but not uniform. While aggregate demand expands at mid-single-digit rates, product-level growth and margin sustainability will depend on mix shifts toward recyclable and specialty formulations.

- Price and margin compression risk exists where raw-material pass-through is weak and competition for commoditized metallized grades intensifies. Firms with differentiated formulations or proprietary carrier technologies are better positioned to capture upside.

Why this report matters to 2026 decision-makers

Our full study is designed as a practical playbook for 2026 choices — not just a descriptive market snapshot. It synthesizes historical performance (2020–2025), a robust forecast (2026–2032), and scenario analysis to stress-test investment options under regulatory and input-cost variability. Key deliverables you will find in the full report include:

- Demand-modeling outputs at the product-family level, integrating volume, price and mix drivers to quantify near-term revenue and margin paths.

- Supply-side mapping that identifies capacity nodes, proprietary process differentiators (e.g., metallization, holography, pigment dispersion) and likely bottlenecks under various demand scenarios.

- Raw-material sensitivity analyses for aluminum coatings, adhesives and carrier films (polyester/PE), including break-even price curves and inventory hedging strategies.

- Regulatory impact modeling focused on circularity mandates and recycled-content requirements, with quantified cost-to-compliance for common retrofit options (thinner carriers, solvent-free adhesives, bio-based films).

- Commercial playbooks and supplier scorecards for sourcing teams that prioritize sustainability, technical capability and geographic risk exposure.

- M&A and partnership scoping: valuation implications of vertical integration, bolt-on targets and technology licensing opportunities.

Note: this preview intentionally omits granular regional and application splits to protect the proprietary modelling that makes the full study actionable. Access to the complete segmentation, supplier shares and product-level economics is available via the full report.

Competitive landscape: who moves first, who follows

The industry exhibits moderate concentration. Our competitive analysis shows that the three largest firms hold a meaningful share of global revenues, and the five largest firms increasingly shape technological and sustainability trajectories. This concentration creates both barriers and levers: scale enables investment in low-emission carrier technologies and digital foiling solutions, while nimble regional players compete on speed-to-market and formulation flexibility.

Highlights from our company-level analysis:

- Leonhard Kurz Stiftung & Co. KG (Fuerth, Germany) — A long-established innovator with a broad portfolio spanning metallized, pigment and aluminum-free LUMAFIN® offerings. Kurz’s emphasis on recyclable PET carriers and its historical R&D depth position it as the market technology leader. Expect Kurz to push premium, circular solutions and to set technical benchmarks that large-brand buyers will reference when updating packaging specifications.

- API Foilmakers Limited (Sheffield, UK) — Focused on metallic and pigment foils for packaging and labels, API has consolidated assets to build scale in recyclable formulations. Their strategy is to trade up in specification and capture label and luxury-pack markets where recyclability is increasingly mandated.

- UNIVACCO Technology Inc. (Tainan, Taiwan) — A global supplier with diversified transfer technologies (hot, cold and holographic). Univacco’s strength lies in substrate-specific formulations — paper, plastic and synthetic leather — making it an attractive partner for converters seeking cross-substrate solutions.

- ITW Foils and CFC International (ITW Foils) (USA) — With a strong presence in pigmented and metallized foils, ITW’s portfolio serves graphics, labels and industrial markets. Its integration of laminates and medical-grade transfer capabilities opens higher-margin specialty niches.

- Wenzhou Fuxing Packaging (Wenzhou, China) — A high-volume manufacturer with significant roll output and advanced coating capabilities. Its scale provides a competitive cost base for mainstream metallized and holographic grades; however, differentiation will depend on progress toward recyclable carriers.

- Murata Kimpaku (Tokyo, Japan) — A premium-decorator supplier with a long history in high-end metallic and holographic applications. Their premium positioning dovetails with markets where aesthetics and brand protection are critical.

- Foilco Limited and Washin Chemical Industry Co., Ltd. — A recent strategic development (April 2026): Foilco’s acquisition by Washin expands Washin’s color catalog and automatic stamping capabilities, accelerating its push into global plastic decoration. Expect additional integration of Washin’s metallic expertise with Foilco’s channel presence to create near-term growth opportunities in plastic-focused decoration segments.

- Crown Roll Leaf, Inc. — A vertically integrated U.S. manufacturer that can accelerate time-to-market for bespoke laminates and technical foils, supporting industrial applications where end-to-end control is a procurement advantage.

Regulatory and raw-material dynamics: short-term disruption, long-term re-shaping

Two regulatory themes will materially influence supplier economics and buyer specifications in 2026:

- Circularity mandates (notably in key export markets) are elevating requirements for recyclability and recycled content in packaging, pushing demand toward thinner, mono-material carriers and solvent-free adhesives. These rules require operational and formulation changes that translate into capital and R&D expenditure.

- Extended Producer Responsibility (EPR) schemes and national recycling targets are prompting brands to prefer suppliers that can demonstrate end-of-life performance. This creates a commercial premium for foils that facilitate recyclability without sacrificing appearance or performance.

From a supply-side perspective, hot stamping foils continue to rely on aluminum-based coatings, specialty pigments, adhesives and polyester or polyethylene carriers. Leading manufacturers collectively invested an estimated USD 180–220 million in 2025 into R&D programs for sustainable carrier materials and digital foiling solutions. For 2026, expect R&D intensity to correlate strongly with market leadership: firms that convert investment into scalable, recyclable product lines will command premium pricing and preferred supplier status with sustainability-conscious brands.

Strategic recommendations for 2026

- For manufacturers: Prioritize pilot deployments of thin mono-material carriers and solvent-free adhesive systems. Establish recycling pilots with key converters and brand partners to translate regulatory compliance into commercial advantage. Use targeted R&D spend to defend margins in premium segments rather than competing on bulk metallized grades alone.

- For converters and brands: Re-assess supplier scorecards to weigh sustainability credentials and technical compatibility with existing recycling streams. Implement joint development agreements to de-risk carrier transitions and lock in favorable terms as scale-up reduces per-unit cost over 2027–2030.

- For investors and acquirers: Monitor consolidation opportunities among mid-sized producers that can gain distribution scale through bolt-on transactions. Assess target portfolios for proprietary carrier technologies or validated recyclable formulations, which are likely to command valuation premiums as compliance requirements tighten.

- For procurement teams: Build raw-material hedging strategies tied to aluminum and polymer inputs, and introduce KPIs that reward supplier investments in digital foiling and recyclability testing.

How to use the full PW Consulting study

The full Hot Stamping Foil Market report supplies the granular data and modelling that underpin the strategic guidance summarized above. It includes scenario outputs, supplier scorecards, technology adoption timelines and a prioritized roadmap for capital allocation and go-to-market initiatives through 2032. If you are evaluating capacity investments, supplier changes, or M&A targets in 2026, the report transforms market intelligence into executable options with quantified risk-return profiles.

We intentionally preserve segmentation granularity and proprietary modelling within the full report to ensure that subscribers and clients get the actionable insights required for confident 2026 decision-making. For comprehensive market breakdowns, supplier-level financial proxies, and downloadable forecast tables, please refer to the PW Consulting Hot Stamping Foil Market publication.

For detailed analysis of this topic, please visit the official page:Hot Stamping Foil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com