Missile Interceptor Market Forecast 2034: US Maintains the Largest Share

Other |

2026-05-19 08:54:36

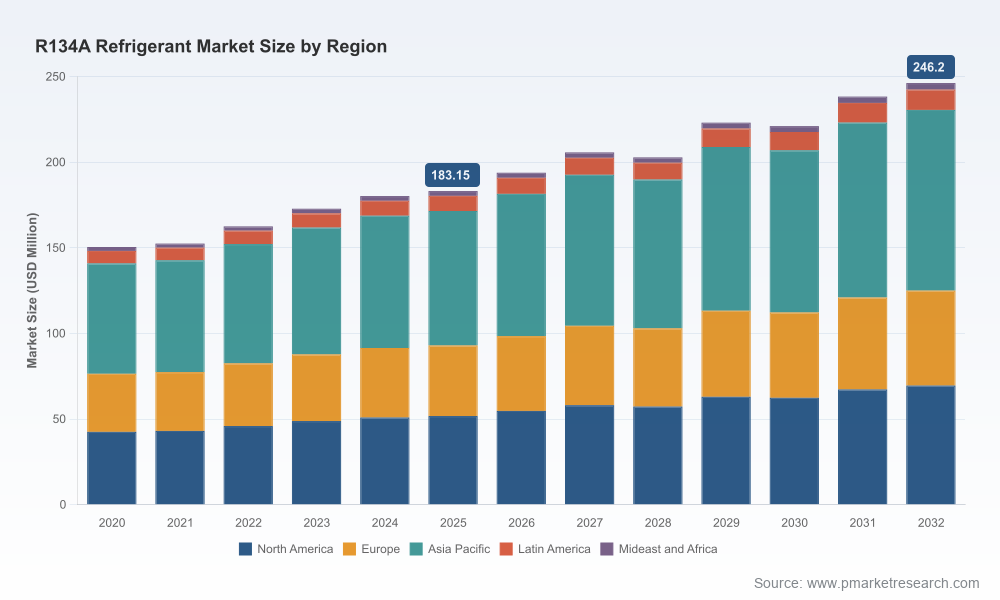

As global refrigerant markets enter a decisive phase of regulatory enforcement, technology transition and supply-chain rebalancing, senior executives must align 2026 choices with multi-year outcomes. PW Consulting’s R134A Refrigerant Market study — built on a 2020–2025 historical series and a 2026–2032 forecast horizon — shows a market that is stable but shifting. At a base-year market size of approximately USD 183.15 Million (2025), and a compounded growth trajectory of about 4.3% through the forecast window, the shape of value is changing faster than headline volumes alone suggest.

R134A Refrigerant Market

Regulatory inflection points are forcing near-term operational choices: new U.S. EPA restrictions and labeling mandates, plus expanded reclamation thresholds under the AIM Act, make compliance a design parameter for product, logistics and aftermarket strategies in 2026.

R134A Refrigerant Market

Technology substitution is accelerating: legacy R134a remains indispensable to significant installed bases and aftermarket service flows, even as low‑GWP alternatives and retrofit technologies begin to migrate value away from virgin HFC volumes.

R134A Refrigerant Market

Supply-side dynamics are tightening margins: feedstock and intermediate price movements, regional manufacturing footprints, and reclaimer economics all layer onto procurement risk and inventory strategy for next 12–24 months.

Commercial opportunities are bifurcating: players who treat R134a as a declining-volume asset will pursue circularity, reclamation and retrofit services, while players who treat it as a transitional feedstock will optimize cost, scale and regulatory compliance.

Quantitative market model: annual historical (2020–2025) and granular forecast (2026–2032) demand and revenue pathways, underpinned by our 4.3% CAGR baseline and alternative scenario runs that stress regulatory tightening and accelerated substitution.

Regulatory impact framework: detailed mapping of EPA actions, AIM Act implications, and likely enforcement timelines — translated into compliance cost curves and operational triggers for supply, labeling and reclamation practices.

Supply‑chain and feedstock risk matrix: supplier footprint assessment, single‑point failures, and a forward-looking raw material sensitivity analysis tied to price and availability shocks.

Profitability & pricing model: margin simulations for different customer cohorts (OEMs, aftermarket service providers, large cold chains), including scenarios for increased reclamation and retrofit uptake.

Competitive landscape & capability scorecards: benchmarking of incumbent producers, regional manufacturers and specialty players across production, distribution, retrofit technologies and service capability.

Commercial playbooks: tactical guidance for procurement renegotiation, inventory hedging, retrofit program commercialization and reclamation network design.

M&A and partnership screening tool: rapid filters to identify acquisition targets or collaborators that accelerate market access, green-transition capability or circularity scale.

Note: this preview intentionally omits the detailed regional and application revenue splits included in the full report. Those granular tables and downloadable datasets — which underpin the models and commercial playbooks above — are available from PW Consulting’s published research portal.

The R134A market remains fragmented and competitive. Incumbent fluorochemical producers and regional manufacturers play distinct roles across manufacturing, aftermarket supply and emerging retrofit solutions. Several strategic themes stand out:

Legacy supply stewardship vs. low‑GWP transition: established players that historically supplied R134a are bifurcating their offerings — maintaining legacy supply chains for service markets while investing in retrofit or alternative refrigerant portfolios. Recent corporate activity illustrates this dual-track strategy: a major producer announced a low‑GWP retrofit approach for automotive systems in late 2024, enabling safer transitions from legacy R134a to newer chemistries without wholesale system replacement; another supplier extended its lower‑GWP portfolio via a commercial arrangement that broadened its Forane™ line in 2025.

Geographic manufacturing scale matters: manufacturers with large-scale production capacity in Asia and localized export networks retain margin flexibility, while regional players in Europe and North America compete more on service, reclamation and regulatory compliance credentials.

Aftermarket and reclamation are strategic battlegrounds: as regulatory regimes enlarge the role of certified reclaimers and labeling requirements, companies that can offer certified reclaimed product, tight chain‑of‑custody and retrofit kits will capture higher-margin aftermarket flows.

Market concentration is relatively low versus many specialty chemical markets, leaving room for nimble entrants, regional champions and service‑oriented aggregators to win pockets of value.

Regulatory enforcement timing: U.S. EPA technology transition restrictions that became effective at the start of 2025 have already started to redirect flows away from certain HFC uses. From January 1, 2026, additional labeling requirements for reclaimed refrigerant containers materially change distributor and reclaimer processes and traceability obligations.

Policy trajectory under the AIM Act: a proposed expansion of reclamation and emissions controls to systems holding 15 pounds or more of HFC refrigerant signals a longer-term shift toward more regulated end-of-life handling — a factor that recalibrates asset valuations for refrigerant inventories and reclamation businesses.

Commercial retrofit and partnership moves: industry players are actively rolling out retrofit solutions and strategic arrangements to expand low‑GWP portfolios — a pattern that increases strategic optionality for OEMs and large end-users but raises investment hurdles for smaller suppliers.

Feedstock and input-price dynamics: incremental upward pressure on feedstock prices and supply volatility in key production nodes requires buyers to adopt active hedging, supplier diversification and reclaimed‑product strategies.

For producers: adopt a dual‑track product strategy. Secure legacy R134a contracts to fund transition investments, while selectively co‑investing in low‑GWP retrofit kits and reclamation capacity to capture aftermarket margins as volumes shift.

For distributors and reclaimers: convert regulatory compliance into a market advantage. Invest in certified labeling, traceability systems and a visible chain‑of‑custody product line — then commercialize reclaimed R134a as a differentiated offering to price‑sensitive buyers.

For OEMs and equipment manufacturers: specify retrofit‑ready designs and tighten service networks. Design choices made now will determine retrofit economics and warranty exposure over the next decade.

For large end‑users and fleet operators: build an internal decision framework that evaluates total cost of ownership for retrofit vs. replacement, incorporating compliance risk, fuel/energy impacts and long‑term refrigerant availability.

For private equity and M&A teams: prioritize targets that add circularity scale (reclaimers, service networks) and retrofit IP rather than bets on stand‑alone virgin production absent diversification into low‑GWP alternatives.

Cross‑industry action: establish collaborative reclamation hubs in high-density markets and co‑develop retrofit certification programs to reduce friction and create shared standards that accelerate adoption.

Scenario-ready models that translate regulation into cash‑flow: use the report’s scenario suite to stress‑test budget assumptions and capital allocation choices for 2026–2028.

Commercial playbooks you can deploy this quarter: procurement negotiation templates, inventory rebalancing checklists and retrofit commercial pilots designed to be operationalized within 90–180 days.

Deal‑screen templates: immediate M&A filters to identify targets that accelerate circularity, retrofit capability or geographic market access.

Regulatory compliance roadmap: an implementation timetable that aligns labeling, reclaiming and reporting requirements with practical supply‑chain actions and cost estimates.

This preview frames why 2026 is the decision year for many organizations exposed to R134A dynamics. The full PW Consulting R134A Refrigerant Market report contains the granular regional and application splits, supplier-level intelligence, downloadable data tables and model access that boards and executive teams need to convert these strategic imperatives into executable programs. For decision-makers preparing capital budgets, procurement strategies or M&A screens in 2026, accessing the complete dataset and proprietary playbooks will materially shorten the path from insight to implementation.

Contact PW Consulting’s market intelligence team to arrange a briefing, receive the full dataset and explore a tailored workshop that aligns the report’s outputs to your 2026 strategic planning cycle.

For detailed analysis of this topic, please visit the official page:R134A Refrigerant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com