Automotive Steel Piston Market: Strategic Outlook for 2026 Decision‑Makers

Executive summary

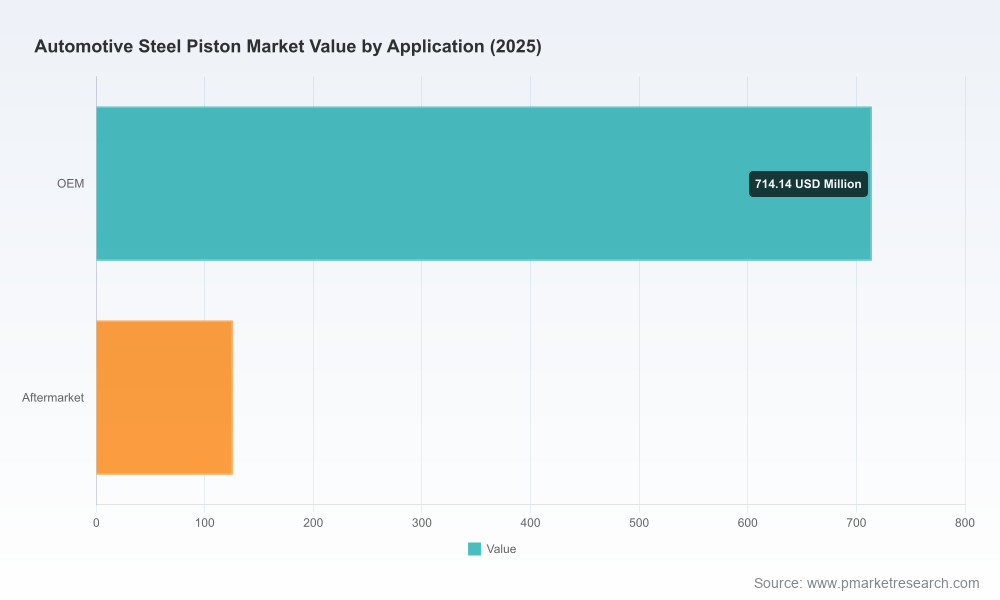

The Automotive Steel Piston market has entered a period of measured, structurally supported growth. Using 2025 as our base year, the global market stood at roughly USD 840 million and is projected to expand at a compound annual growth rate (CAGR) of 4.2% through the forecast horizon of 2026–2032, reaching roughly USD 1.11 billion by the end of that period. This trajectory reflects a mix of legacy demand in heavy‑duty diesel platforms, incremental adoption of advanced steel piston concepts in passenger‑car applications where ICEs persist, and ongoing product innovations that deliver lifecycle cost and emissions advantages versus alternative materials.

Automotive Steel Piston Market

For executives preparing strategic plans in 2026, the choice is not whether the market will grow — it will — but how to position resources across product development, manufacturing technology, channel strategy, and risk mitigation. The full PW Consulting study provides the granular inputs required to make those choices with confidence; this preview outlines the strategic levers and operational playbook that should shape boardroom decisions in the coming 12–36 months.

Automotive Steel Piston Market

Why 2026 is a pivotal planning year

Three timing facts make 2026 materially important for firms active in or considering entry to the steel piston space:

Automotive Steel Piston Market

- Policy and OEM roadmaps are crystallizing around emissions targets and heavy‑vehicle lifecycle requirements; product development cycles initiated in 2026 will align with Tier‑1/2 procurement windows in 2028–2030.

- Manufacturing investments — whether in friction‑welding, laser‑welding, high‑precision forging, or coating lines — have lead times and capital profiles that require decisions in 2026 to impact supply in the second half of the decade.

- Market growth is steady but not runaway (mid‑single digits CAGR); this makes timing and efficiency of execution decisive. First movers on validated CO2 reduction claims and demonstrable durability will capture outsized commercial opportunities while others compete on price.

Market dynamics: technical, regulatory and commercial drivers

- High‑pressure capability and durability. Modern steel piston designs are engineered to withstand peak cylinder pressures approaching the highest levels required by heavy‑duty diesel applications. This capability is a non‑negotiable for engine platforms targeting maximum efficiency and compliance with stringent emissions regimes.

- Measured emissions and efficiency gains. Optimized steel piston systems — combining material choice, surface treatments and thermal management — can deliver meaningful CO2 improvement through friction reduction and enhanced cooling. For OEMs pursuing fleet‑level reductions, these gains are additive to powertrain electrification strategies.

- Manufacturing technologies as differentiators. Friction‑welding, laser‑welding and one‑piece forged constructions each create unique performance and cost trade‑offs. Laser‑welded solutions can support minimum compression heights with superior cooling, while friction‑welded concepts excel in large‑bore durability applications.

- Proven field longevity. Field testing and OEM validations show service lives well into fleet‑scale thresholds for commercial vehicles. Long wear‑free intervals change the economics of total cost of ownership and aftermarket demand dynamics.

- Materials and regulatory risk. Steel price volatility, alloy availability, and tightening emissions/efficiency standards will shape sourcing strategies and product specs. Suppliers that pair material strategy with scalable production will be advantaged.

Competitive landscape: capability map and strategic moves

The competitive set mixes global component groups, OEM‑affiliated suppliers, and regional specialists. Several themes emerge from company capabilities:

- Technology leaders with system depth. Established players that combine multiple steel piston concepts with engineering services (e.g., welded variants for both passenger and commercial segments) hold competitive advantage when customers demand tailored solutions for high‑pressure combustion systems.

- One‑piece and large‑bore specialists. Suppliers focused on large‑bore engines leverage friction‑welded and one‑piece constructions to serve marine, locomotive and heavy‑truck platforms where diameter and service life are differentiators.

- OEM‑integrated suppliers. Manufacturers embedded in OEM and aftermarket supply chains can accelerate validation and scale but must continually demonstrate cost and weight parity with competing materials to retain share.

- Regional champions. Local manufacturers with strong ties to commercial‑vehicle ecosystems can win fleet business through proximity, tailored warranties, and fleet management services — especially in regions where diesel remains dominant.

From a strategic perspective, the market remains moderately fragmented: established tier‑1s lead on engineering breadth, but there is room for focused challengers with differentiated manufacturing techniques, superior cost structures, or demonstrable CO2 and TCO improvements to gain share.

Strategic implications for 2026 decision‑makers

- Prioritize technology bets. Choose 1–2 manufacturing technologies to master (e.g., laser‑welding for passenger‑car derivatives; friction‑welded one‑piece for large‑bore diesel). Depth of capability will be more valuable than superficial breadth.

- Lock the value proposition to CO2 and TCO. Translate technical improvements into verified fleet‑level CO2 and lifecycle cost metrics. Buyers will pay for validated emissions and cost advantages, not for abstract technical claims.

- Optimize supply chain and raw‑material strategy. Secure alloy supply lines, invest in recycling/secondary sourcing where feasible, and hedge price exposure for critical inputs to protect margin across the forecast period.

- Adopt a dual‑track go‑to‑market. Preserve OEM partnerships for design‑in opportunities while deploying aftermarket/service strategies that monetize long piston life and fleet maintenance cycles.

- Pursue targeted partnerships and M&A. Consider bolt‑on acquisitions for missing manufacturing capabilities or licensing agreements for proven piston architectures to accelerate time‑to‑market without linear capital burn.

- Plan for EV coexistence. Build scenario plans that balance investments in steel piston technologies with contingencies for accelerated ICE decline in passenger cars — prioritize commercial and industrial ICE platforms with longer lifetimes.

Operational playbook: actions for the next 12–36 months

- 0–12 months (fast moves). Run targeted pilot projects with lead OEMs or fleets to validate CO2 and TCO claims under real‑world cycles; establish a materials hedge; and prototype production lines for priority welding or forging methods.

- 12–24 months (scale‑up). Finalize engineering forering and tooling, negotiate multi‑year supply contracts tied to quality and volume discounts, and set up service agreements with fleet operators to capture aftermarket value of high‑durability products.

- 24–36 months (commercialization). Ramp manufacturing to capture forecasted demand, deploy warranty and diagnostic services that monetize long service life, and evaluate strategic acquisitions if capacity scaling faster than organic options becomes necessary.

What the full PW Consulting report delivers

This introduction highlights strategic themes and operational priorities. The full PW Consulting Automotive Steel Piston Market report provides the decision‑grade detail you will need to execute in 2026:

- Comprehensive historical and forecast market model (2020–2032) with scenario alternatives and sensitivity to steel pricing and ICE fleet evolution.

- Granular segmentation by product type, application channel, and region — including supply/demand balances and gap analysis (note: segmentation details are available in the full report).

- Supplier benchmarking and scorecards that compare engineering capabilities, manufacturing footprints, product portfolios, patent positions, and go‑to‑market strategies for incumbent and emerging players.

- Cost models and margin simulations for competing manufacturing technologies, enabling boardroom trade‑offs between capex, unit economics, and time to revenue.

- Actionable 36‑month implementation roadmaps, KPI templates, and a negotiation playbook for OEM design‑ins and fleet contracts.

Conclusion: a disciplined play wins

The steel piston market offers a classic strategic paradox: stable, mid‑single‑digit growth that rewards the timing and quality of investment rather than sheer scale. For firms preparing 2026 plans, the imperative is to pick a clear technology and market focus, validate performance claims with rigorous field data, and lock supply chains to preserve margin. Those who act now — pairing focused manufacturing capability with verified CO2 and TCO credentials — will convert a modest market expansion into outsized commercial returns.

PW Consulting’s full report converts the insights above into the practical, quantitative tools executives need to make those 2026 choices with conviction. For the complete datasets, segmented forecasts and supplier scorecards, please consult our full study available on the PW Consulting publication page.

For detailed analysis of this topic, please visit the official page:Automotive Steel Piston Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com