U.S. Beauty And Personal Care Products Market Reinforces Skincare Dominance

Other |

2026-02-19 09:51:02

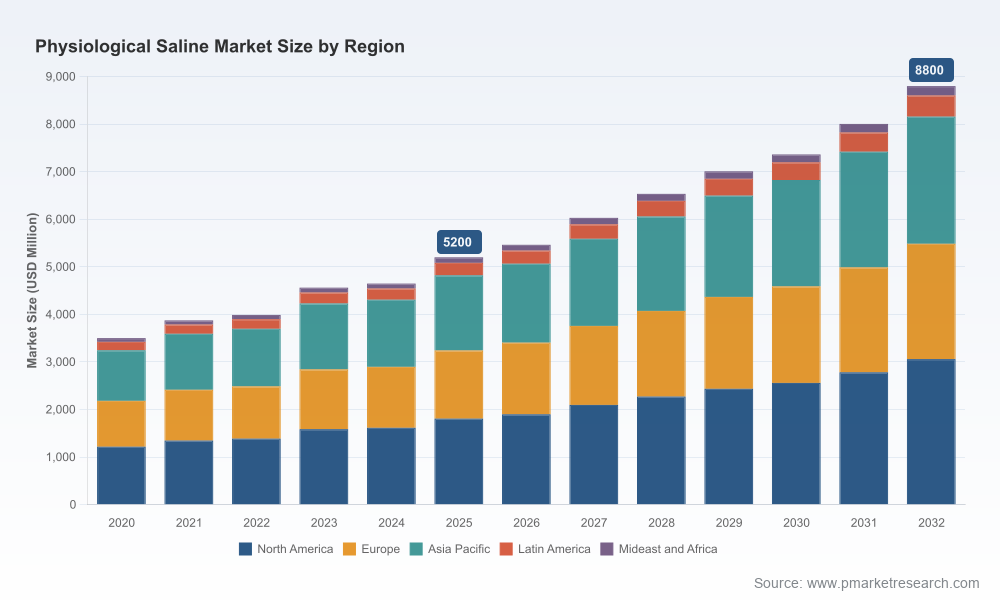

As healthcare systems stabilize following the systemic disruptions of recent years, the physiological saline market is entering a phase of renewed, predictable growth. PW Consulting’s forthcoming in‑depth study — grounded in a 2025 base year and projecting through 2032 — shows the global market expanding at a compound annual growth rate (CAGR) of 7.4% from 2026 onward. Measured on a revenue basis (USD million), the market grew materially between 2020 and 2025 and is forecast to continue that trajectory toward nearly USD 8.8 billion by 2032. For executives planning investments, procurement strategies, or competitive moves in 2026, this trajectory signals both opportunity and a need for disciplined strategic choices.

Physiological Saline Market

Macro clarity at the right moment: With a clear 2025 baseline and a seven‑year forecast horizon, the analysis provides the temporal scope required for capital budgeting, capacity expansion, and M&A timeline decisions.

Physiological Saline Market

Operationally actionable: Beyond headline growth, the study dissects supply chain fragilities, regulatory shifts, and reimbursement dynamics that will translate directly into procurement and pricing levers for hospital systems, wholesalers, and manufacturers in 2026.

Physiological Saline Market

Risk‑calibrated scenarios: We couple market growth expectations with scenario planning — from stable supply to episodic shortages — allowing decision makers to stress‑test investment cases and contract negotiations.

The saline market’s steady expansion reflects a combination of demographic demand, rising procedure volumes in emerging markets, and the re‑establishment of routine elective care in developed economies. From a strategic vantage point, a 7.4% CAGR implies that capacity and logistics decisions made in 2026 will influence a firm’s ability to participate in the majority of incremental value created through 2032. Companies that act early to secure raw material access, optimize packaging choices, and lock in distribution partnerships will realize outsized returns relative to late movers.

For hospitals and integrated healthcare purchasers, the growth curve requires a reassessment of stocking strategies: flat cost‑plus procurement is increasingly insufficient. Dynamic contracting that ties price to service-level guarantees, contingency supply, and product traceability will be essential to manage both cost and continuity of care.

Clinical demand stability: Saline remains foundational across IV fluid replacement, medication reconstitution, irrigation, and hydration. Clinical protocols and inpatient utilization patterns continue to anchor baseline demand.

Packaging and material shifts: There is a clear industry tilt toward flexible, non‑PVC containers and prefilled solutions that reduce contamination risk and improve workflow efficiency. Manufacturers already investing in alternative polymer systems and single‑use delivery formats are benefiting from differentiated procurement conversations.

Regulatory tailwinds and headwinds: The FDA officially declared the nationwide shortage of 0.9% sodium chloride injection resolved in August 2025 — a pivotal moment that normalizes supply but also resets buyer expectations for approved sources. Simultaneously, coding changes and reimbursement considerations (e.g., HCPCS and CPT updates implemented in 2025–2026) are reshaping revenue capture for infusion services and will affect unit economics across care settings.

Reimbursement dynamics: Medicare and payer practices influence hospital purchasing power and private payer negotiations. For example, HCPCS pricing for large‑volume saline infusions remains a material factor in infusion center economics, with typical Medicare reimbursement bands that buyers and sellers must understand to structure sustainable contracts.

The market exhibits moderate concentration: the top three players account for a majority share, and the top five exceed six in ten of total market value. This concentration creates a strategic environment where scale, regulatory compliance, and distribution reach are decisive. Key incumbent players include:

Baxter International Inc. (Deerfield, Illinois, United States) — A leading supplier of IV isotonic solutions in flexible containers; recent geographic expansion efforts aim to broaden commercial availability and secure procurement pathways.

B. Braun Melsungen AG (Melsungen, Germany) — A major European supplier with broad IV fluid portfolios designed for extracellular fluid replacement and hospital formularies.

Fresenius Kabi AG (Bad Homburg vor der Höhe, Germany) — Strong in bagged saline and medication vehicle applications; recent distribution partnerships have reinforced access in growth markets.

ICU Medical, Inc. (San Clemente, California, United States) — Differentiated by flexible non‑PVC/non‑DEHP containers and collaborative manufacturing arrangements; positioned to capture procurement mandates emphasizing material safety and compatibility.

Grifols, S.A. and related entities (Barcelona, Spain) — Known for polypropylene bag solutions tailored to hospital and plasma‑donation use cases, with established channel relationships.

Otsuka Pharmaceutical Co., Ltd. (Tokyo, Japan) and AdvaCare Pharma (Philadelphia, Pennsylvania, U.S.) — Important regional manufacturers and suppliers with targeted product lines and manufacturing footprints that serve specialized segments of demand.

Recent corporate moves — exemplified by Baxter’s market expansion in early 2026 and a distribution partnership announced by Fresenius SE & Co. KGaA — illustrate two strategic playbooks: consolidate via geographic expansion or secure reach via channel partnerships. Both are effective, but they require different operational investments (owned capacity vs. channel agreements) and risk profiles.

Secure multi‑tiered supply contracts: Lock in primary and secondary suppliers with clear SLAs and contingency clauses. Include audit rights and penalty structures that reflect the value of continuity in clinical settings.

Invest selectively in packaging innovation: Prioritize non‑PVC materials where clinical and procurement requirements align, and build product roadmaps that simplify transitions for hospital buyers.

Align pricing to total cost of care: Move negotiations beyond unit price to consider infusion time, administration labor, and waste. Reimbursement changes mean the end‑to‑end economic model matters more than ever.

Monitor and model regulatory changes: Integrate the latest coding and shortage‑resolution developments into financial models and contract assumptions to avoid surprise margin compression.

Plan capacity with scenario buffers: Given the market’s growth rate, allocate capital to ramp capacity only where lead times and raw-material risk justify it; otherwise, prioritize flexible partnerships and toll manufacturing.

Our complete study is designed as a decision‑support toolkit for 2026 and beyond. It contains:

Quantified market sizing and validated growth trajectories (historical 2020–2025, base year 2025, forecast 2026–2032) with sensitivity analyses across demand and supply scenarios.

Regulatory timeline and implications matrix covering shortage resolution status, coding updates, and approval pathways that affect market access.

Competitive capability maps and strategic profiles of incumbent and challenger players, including manufacturing footprints, packaging technologies, and partnership networks.

Operational playbooks for procurement, manufacturing, distribution, and portfolio management — each with KPIs, cost drivers, and risk mitigants.

Deal screening framework and valuation heuristics for M&A and JV opportunities, calibrated to market concentration metrics and growth drivers.

Interactive scenario models and downloadable templates that teams can use to run bespoke sensitivity analyses tied to their own P&L and balance‑sheet assumptions.

Procurement leads: Use our supplier risk heatmaps and the reimbursement sensitivity table to rework contracts and inventory triggers in Q1–Q2 2026.

Commercial leaders: Align go‑to‑market plans with packaging and material preferences highlighted by regional formularies; leverage channel partnerships where owned distribution is not cost‑effective.

Corporate development teams: Employ our deal screening heuristics to prioritize targets that complement scale, fill regional gaps, or accelerate access to non‑PVC technologies.

R&D and operations: Map capital decisions to scenarios that balance steady CAGR expansion with low‑frequency, high‑impact supply disruptions.

PW Consulting’s preview delivers the strategic scaffolding executives need to make confident 2026 decisions: clear market sizing and growth expectations, scenario‑based risk assessments, and a set of prioritized playbooks focused on continuity, compliance, and commercial advantage. In keeping with our “trailer” approach, this overview intentionally demonstrates the depth and practical orientation of the complete study while withholding certain granular segmentation data here; those details — including targeted regional and application-level analyses and exact segment shares — are provided in the full report to preserve their contextual integrity and enable precise commercial action.

For executives ready to translate the market’s 7.4% CAGR and near‑term regulatory and reimbursement shifts into concrete plans for 2026, PW Consulting’s full Physiological Saline Market report is the operational blueprint that turns insight into execution.

For detailed analysis of this topic, please visit the official page:Physiological Saline Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com