PW Consulting: Digital Valve Positioner Market to Hit $2.73B by 2032 at 5.2% CAGR

Other |

2026-07-09 08:27:19

As PW Consulting’s senior industry analyst, I present a targeted, decision‑focused preview of our full Gibberellin Acid (GA) Market study. This briefing synthesizes the macro trajectory, competitive dynamics, and regulatory inflection points that will shape boardroom decisions in 2026. It is designed to demonstrate the depth and practical utility of the full report while reserving the granular segmentation tables and proprietary scenario worksheets for subscribers.

Gibberellin Acid (GA) Market

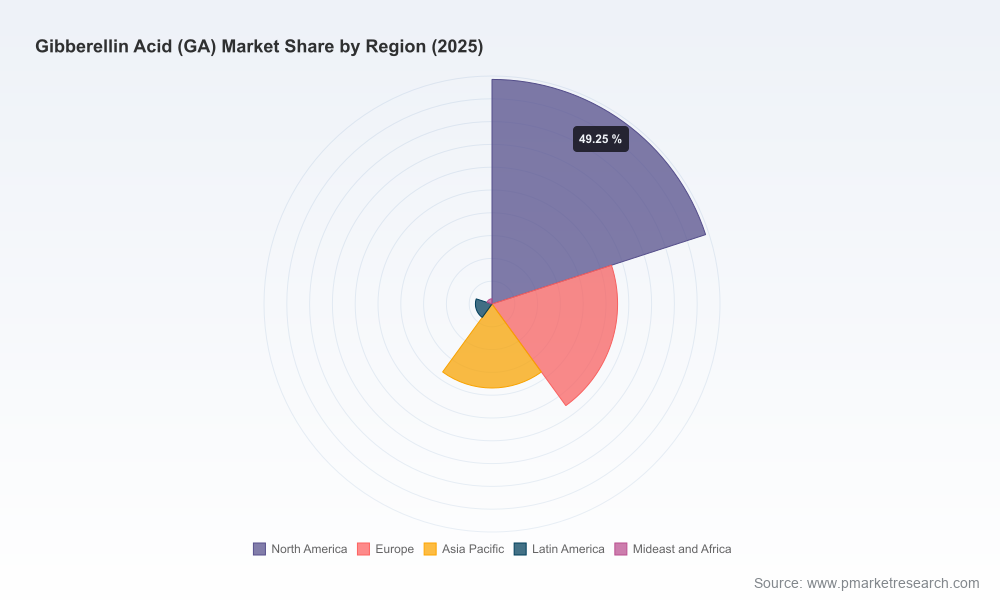

The GA market has exhibited steady growth through the early 2020s and accelerates into the late 2020s. On the demand side, the market moved from an estimated USD 712.45 Million in 2020 to USD 981.45 Million in 2025. Under our baseline forecast, the market is projected to reach approximately USD 1,080.02 Million in 2026, and expand further to about USD 1,689.02 Million by 2032—an implied compound annual growth rate of roughly 8.15% across the forecast window. These macro kinetics reflect a combination of gradual adoption in established crop applications and faster uptake in new formulations, organic‑compliant offerings, and precision agriculture use cases.

Gibberellin Acid (GA) Market

For executives evaluating capital allocation, the headline implication is clear: GA is a growth platform with enough scale and predictable expansion to warrant near‑term investment in production capacity, regulatory strategy, and downstream commercial differentiation. However, the path to outsized returns is not uniform—value will accrue to players who execute along distinct vectors described below.

Gibberellin Acid (GA) Market

Timing of investments: Our 2026 lens identifies a narrow window where incremental capacity and formulation innovation capture disproportionate margin uplift as fermentation cost improvements and formulation patent cliffs converge.

Regulatory and market access: Early engagement with regulatory bodies and alignment with organic/OMRI pathways accelerates product adoption in premium segments; late entrants face higher compliance cost and longer time‑to‑market.

M&A and partnership playbook: The market’s moderate concentration and technology push create attractive bolt‑on opportunities—especially for firms seeking to secure upstream supply or add differentiated formulation portfolios.

Commercial prioritization: Our demand scenarios enable prioritized targeting of crop segments and distribution channels that offer the fastest payback on promotional spend in 2026.

Production efficiency improvements: Industry adoption of probiotics and optimized fermentation techniques in late 2025 yielded notable cost reductions—near‑term data indicates production cost improvements of roughly 9% for adopters. Companies that scale these process innovations will see margin expansion or be able to underprice competitors in selected segments.

Regulatory inflection points: The substance’s regulatory status is actively evolving. European regulatory reviews concluded in 2025 and U.S. listings were updated through mid‑2026, creating both short‑term compliance requirements and longer‑term clarity on permitted uses and label claims. Products that align with organic certification pathways have a distinct commercial advantage in specific markets.

Formulation and applications innovation: New low‑volatile and shelf‑life enhancing formulations (including launches in 2025) are re‑shaping use cases across horticulture, fruit production, and specialty crops. These formulation advances are becoming primary purchase drivers for growers concerned with postharvest quality and market timing.

Boardroom capital allocation—Prioritize: Use our scenario outputs to stress‑test capacity expansion and acquisition proposals against downside regulatory and raw‑material scenarios.

R&D and product strategy—Differentiate: Focus R&D spend on organic‑compatible formulations and low‑volatility solutions that reduce application risk and unlock premium pricing.

Commercial deployment—Segment: Align sales incentives and channel partnerships with the crop categories and distribution channels that our demand elasticity models show are most responsive to promotional support.

Risk management—Hedge: Build sourcing strategies that mirror the three most likely raw‑material trajectories in our probabilistic model to avoid margin compression if input prices spike.

The GA market displays moderate fragmentation: the three‑player and five‑player concentration ratios indicate that while global incumbents hold visible brands and distribution reach, there is ample room for mid‑market specialists and regional suppliers to compete through product differentiation, responsive supply, and targeted channel strategies. Below is a concise tactical read on leading participants featured in the full study.

Valent BioSciences LLC (United States) — Strength: Deep PGR (plant growth regulator) formulation expertise and established brands. Strategic priority: defend value by bundling agronomic advisory and loyalty programs; risk: incumbent brand erosion if formulation innovation stalls.

Nufarm Limited (Australia) — Strength: Broad commercial footprint in agriculture/horticulture channels. Strategic priority: leverage distributor networks in key export markets and invest in localized stewardship programs to accelerate adoption.

Fine Americas, Inc. (United States) — Strength: Focus on ornamentals and turf markets with specialized application knowledge. Strategic priority: scale micro‑formulation R&D to capture premium margins in high‑value niches.

SePRO Corporation (United States) — Strength: Unique presence in aquatic and turf management. Strategic priority: cross‑sell into adjacent landscaping and municipal channels where long contract cycles favor incumbents.

Jiangsu Fengyuan Bioengineering Co., Ltd. (China) — Strength: Low‑cost manufacturing scale and upstream supply. Strategic priority: move up the value chain through co‑formulation and regulatory compliance investments to access Western markets.

Corteva Agriscience (United States) — Strength: Strong R&D and go‑to‑market engine; notable product launch (X‑Pand™) in mid‑2025 with OMRI listing for organic compatibility. Strategic priority: exploit brand trust and regulatory approvals to accelerate premium segment penetration.

Greenleaf Chemical LLC (United States) — Strength: Niche formulations for ornamentals/horticulture. Strategic priority: build technical service bundles to offset price competition from bulk suppliers.

Zhengzhou Delong Chemical Co., Ltd. (China) — Strength: Specialization in GA3 manufacturing. Strategic priority: target white‑label relationships and consider JV strategies with Western formulators seeking consistent low‑cost supply.

Product innovation: Corteva’s July 2025 launch of a new low‑volatile, organic‑eligible GA product has shifted customer expectations around shelf life and postharvest performance. This highlights the importance of formulation IP as a defensive moat.

Regulatory clarity: Updates across major regulatory jurisdictions through 2025–mid‑2026 have reduced legal uncertainty for certain use cases, but they also raise the bar for compliance documentation—creating an advantage for firms with robust regulatory affairs capabilities.

Cost base changes: The 2025 fermentation and bioprocessing advances reduce per‑unit production cost for adopters. Early implementers gain a cost leadership path; laggards risk margin erosion as price competition intensifies.

The full PW Consulting study is structured for immediate operational use. It includes:

Transparent market sizing and a documented methodology (base year 2025), with historicals 2020–2025 and a scenario‑based forecast through 2032.

Demand elasticity matrices and go‑to‑market playbooks tuned to crop types and channel archetypes.

Supplier & formulation heatmap, including technical maturity, regulatory status, and cost curve positioning.

Commercial scorecards for the leading suppliers and a supplier selection framework for procurement teams.

M&A checklist, including value‑creation levers, integration risks, and a shortlist of bolt‑on targets (annotated with strategic rationale).

Regulatory tracker and compliance calendar to align product launches with approval milestones.

Interactive dashboards (subscriber access) enabling you to run custom scenarios for price, input cost, and adoption speed—the practical toolset for 2026 planning cycles.

Prioritize small, fast payback experiments in formulation variants that claim organic compatibility or extended shelf life—these are demand accelerators with relatively low CAPEX.

Invest in upstream supply safeguards: secure fermentation capacity or preferred supplier agreements now to protect gross margin through 2027–2028.

Build regulatory capability in‑house or via retained experts; regulatory clarity in 2025–2026 creates a commercial runway but requires proactivity to exploit.

Use M&A selectively to add formulation IP or channel access rather than bulk manufacturing alone—our valuation scenarios show higher returns from capability‑adding acquisitions.

PW Consulting’s full analysis contains the detailed segmentation, financial models, and downloadable dashboards necessary to operationalize these recommendations. This preview demonstrates the strategic value the research delivers to 2026 decision‑makers while intentionally omitting the granular region/application splits and level‑by‑level revenue tables that form the backbone of executable plans. For access to the complete dataset, user‑interactive tools, and the vendor scorecards, please visit our report page.

For detailed analysis of this topic, please visit the official page:Gibberellin Acid (GA) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com