Vegetable Protein Market 2026: Strategic Imperatives for Corporate Decision‑Makers

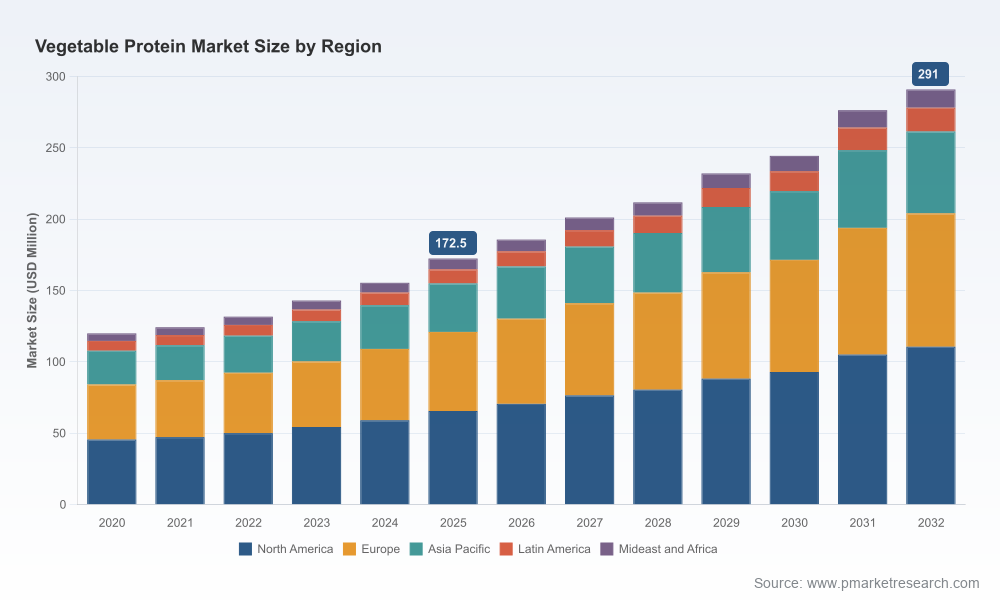

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive introduction to our latest Vegetable Protein Market research — a practical, decision‑grade study built for boards, corporate strategy teams, and investor due‑diligence groups preparing plans for 2026 and beyond. The market is in a structural growth phase: the global vegetable protein market expanded materially through 2020–2025 and is forecast to continue at a compound annual growth rate of 7.9% over the 2026–2032 horizon. From a solid mid‑market base in 2025, our forecast shows an accelerating revenue trajectory through 2032 as demand, innovation, and upstream investments converge.

Vegetable Protein Market

Why this report matters for 2026 decisions

- Capital allocation and capacity timing: New integrated facilities and selective closures across major producers mean capacity availability will be lumpy. Boardrooms that get timing right for greenfield, brownfield, or tolling contracts will protect margins and market share.

- Sourcing resilience: Upstream agronomy initiatives and policy shifts are redefining raw material risk profiles. Procurement teams need a forward‑looking sourcing playbook, not a rear‑view mirror contract.

- Regulatory and labeling readiness: New guidance on plant‑based naming and allergen disclosure is reshaping product claims and packaging decisions — fast compliance is a market access enabler.

- Product and sensory strategy: Textured formats and neutral‑taste isolates are enabling premiumization across meat analogues, beverages, and fortified foods. R&D investments now determine commercial relevance in two years’ time.

- M&A and partnership windows: Moderate market concentration and active capex by large players create opportunities for bolt‑on acquisitions, JV manufacturing, and offtake arrangements.

What PW Consulting’s Vegetable Protein Market report delivers

This study is designed as a playbook for execution — not just a market narrative. Highlights include:

Vegetable Protein Market

- Proven market sizing & forward forecasts: A transparent base‑year (2025) and a 2026–2032 forecast built from primary interviews, proprietary demand models, and supply‑side capacity schedules. (Summary macro figures are presented in this introduction; detailed revenue, price, and volume matrices are provided in the full report.)

- Supply‑chain heatmaps: Plant locations, integrated crush‑to‑texturization flows, critical logistics chokepoints, and cost drivers for key raw materials.

- Raw material and input modelling: Scenario decks for pulse, oilseed, and cereal feedstocks under alternative yield and policy pathways; sensitivity to freight, energy, and exchange rates.

- Regulatory & policy impact analysis: Practical implications of recent FDA draft labelling guidance and updated dietary guidance on product positioning, claim mapping, and litigation risk mitigation.

- Competitive and capability benchmarking: Supplier scorecards, CRx concentration analysis, technology roadmaps, and commercial channel strategies for leading players.

- Commercial playbooks: Go‑to‑market frameworks for B2B ingredient sales, co‑packing, private label relationships, and direct‑to‑consumer protein innovations.

- M&A and strategic partnership toolkit: Target screen templates, valuation comparables, integration checklists, and transaction case studies focused on de‑risking deals in a capital‑intensive sector.

- Implementation accelerators: 90‑, 180‑ and 360‑day action plans for procurement, R&D, manufacturing, and sales to convert insights into measurable outcomes.

Note: this public introduction deliberately showcases the study’s depth while reserving granular region/application revenue splits and sensitive contract data for the full report and client workshops.

Vegetable Protein Market

Dynamics shaping the market in 2025–2026

- New capacity & consolidation: Large investments and plant reconfigurations are already shifting the supply curve. The entry of major integrated facilities and periodic plant rationalizations change bargaining power between buyers and suppliers.

- Policy and diet guidance: Regulatory shifts and public diet recommendations are lifting the macro demand envelope for plant proteins even as labeling and allergen disclosure rules force tactical changes in product architecture.

- Agronomy and upstream innovation: Seed technologies and biological solutions are improving yields and protein quality in targeted climates, reducing unit cost pressure and enabling localized sourcing strategies.

- Product innovation: Advances in texturization and flavor masking increase the addressable market for premium meat analogues and high‑protein beverages, raising per‑unit realizations.

- Geopolitical & policy tailwinds: National self‑sufficiency programs for pulses and legumes create sourcing diversification opportunities — but also short‑term volatility where procurement strategies are not adapted.

Competitive landscape: players, positioning, and recent strategic moves

The market is characterised by a mix of large integrated agribusinesses, ingredient specialists, and focused pea/legume processors. The three‑ and five‑firm concentration metrics indicate a market with room for scale advantages but also niches where focused specialists compete on quality and specialty applications.

- Roquette Frères (Lille, France): A clear leader in plant‑based ingredient innovation with a broad textured protein portfolio. Roquette’s recent launches of textured wheat and pea variants, and a neutral‑taste pea isolate, signal a renewed push into meat analogues and clean‑label beverage formulations. Their strength is product breadth and R&D to translate crop sourcing into market‑ready formats.

- Archer Daniels Midland (ADM) (Chicago, US): ADM leverages integrated crush‑to‑texturization assets. Their recent U.S. plant consolidation reflects an efficiency play: optimizing capacity utilization while maintaining wide reach for soy‑based proteins.

- Cargill (Minneapolis, US): A diversified portfolio across isolates, hydrolysates and textured products, with a global supply chain that supports both food and animal nutrition demand segments.

- Puris (Des Moines, US): A market leader on pea‑first strategies, focusing on non‑GMO, clean‑label isolates and premium variants tailored to plant‑milk and alternative‑meat segments.

- Protealis (Belgium): Bringing upstream differentiation via seed technology and biologicals, enabling higher‑yield varieties adapted to European climates — a strategic asset for companies pursuing local sourcing and traceability.

- Louis Dreyfus Company, Beneo, Ingredion, IFF: Each plays a distinct role — from broad pulse ingredient coverage to functional oat proteins and flavor systems — creating an ecosystem where formulation, flavor, and functionality are decisive competitive levers.

Recent industry moves — new integrated capacity online, targeted product launches, regulatory approvals for seed biology, and facility optimization by legacy players — are concrete indicators that 2026 will be a year of reallocating advantage for companies that act early.

Strategic implications and recommended actions for 2026

- Procurement & sourcing: Re‑negotiate medium‑term offtake contracts with optionality for crop yield scenarios; build diversified supplier panels that include seed‑to‑product specialists to lower raw material volatility.

- Manufacturing footprint: Reassess tolling vs. owned capacity in light of recent new facilities and closures — a hybrid model often balances capital efficiency with market responsiveness.

- R&D & product roadmaps: Prioritize formats with sensory parity, clean labeling, and functional performance. Invest in joint development with flavor houses and texturization partners to accelerate time‑to‑market.

- Regulatory readiness: Update labeling, claims, and allergen disclosures now to avoid costly repackaging and market access delays when guidance becomes law or industry standard.

- M&A & partnership strategy: Use our target screen to identify bolt‑on technologies, regional seed specialists, or co‑packing partners that close capability gaps without disproportionate integration risk.

- Sustainability & traceability: Translate upstream seed and agronomy investments into verifiable chain‑of‑custody claims — a growing purchasing criterion for large CPG buyers.

How to use this report in your 2026 planning cycle

We recommend a three‑phase approach aligned to typical corporate planning calendars:

- Phase 1 – Immediate (0–90 days): Use the market scenarios and supplier scorecards to reprice and secure 12‑ to 24‑month supply commitments; update product claims to comply with emerging regulation.

- Phase 2 – Tactical (90–180 days): Run pilot product launches with flavor‑masked prototypes, lock tactical tolling arrangements, and commence targeted M&A diligence on accretive assets identified in our screening tool.

- Phase 3 – Strategic (180–360 days): Finalize capacity investments or JV structures guided by our capex ROI model and deploy a three‑year commercialization plan informed by our demand elasticity and price‑realization scenarios.

Next steps & how to access the full intelligence

This introduction highlights the strategic value our Vegetable Protein Market study offers for 2026 decision‑making. For procurement teams, R&D leaders, M&A sponsors, and sustainability officers, the full report includes granular revenue matrices, regional and application breakdowns, supplier contracts and pricing decks, and a proprietary list of vetted acquisition targets — content intentionally reserved for report subscribers and strategy workshop clients.

Engage with PW Consulting to receive the complete study, a tailored executive summary for your business unit, or to schedule a scenario workshop that maps the implications of our forecast to your organization’s P&L and balance sheet. In a market growing at near‑double digit rates on a multi‑year horizon, actionable timing matters more than ever.

For detailed analysis of this topic, please visit the official page:Vegetable Protein Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com