Vitamin K1 Market Forecast & Growth Analysis

Art |

2026-06-25 12:19:26

As manufacturers, supply-chain leaders, and investors plan for 2026, the metal cutting tools market presents a mix of steady expansion, supply-side stressors, and pockets of strategic opportunity. PW Consulting’s upcoming full report—anchored on a 2025 base year and projecting through 2032—synthesizes historical performance (2020–2025), near-term inflection points, and actionable scenarios. This preview outlines the market’s macro trajectory, the forces reshaping competitiveness, and the practical intelligence executives need to align capital deployment, sourcing strategies, and product roadmaps for 2026.

Metal Cutting Tools Market

Capital planning cycles, supplier contracts, and new product development timelines all converge in 2026. Our research identifies not only the direction of travel—a market expanding at a mid-single-digit compound annual growth rate (CAGR)—but also the operational levers and risk vectors that will determine whether firms capture market share or merely weather the upswing. In short: understanding volume growth is necessary but insufficient. Executives need a practical map of margin pressures, material constraints, regulatory shifts, and competitor moves to convert momentum into durable advantage.

Metal Cutting Tools Market

Baseline: PW Consulting uses 2025 as the base year for commercial planning. The market in that year represents the foundation for 2026 budgeting and go-to-market programs.

Metal Cutting Tools Market

Near-term growth: Our forecast models point to mid-single-digit expansion in the forecast window, with a core CAGR of approximately 5.82% over the projection period (2026–2032).

Outlook through 2032: Under the central case scenario, the market grows steadily toward the higher end of the forecast horizon, driven by ongoing demand from precision manufacturing, automotive electrification-related machining needs, and renewable and power-generation components.

Raw material pressure: The sector is contending with material-side volatility—most notably tungsten carbide and certain high-speed steels. Recent industry reporting highlights sharp price increases and constrained rod-making capacity, and in some corridors inventories are tighter than manufacturers prefer. For 2026, procurement strategies that blend longer-term off-take agreements with flexible spot exposure will materially affect cost of goods and margin visibility.

Demand composition: Demand drivers are becoming more differentiated. While traditional sectors like automotive and general manufacturing remain important, growth pockets are emerging in precision electronics, energy components, and specialized medical devices. These end-markets demand higher-performance substrates, tighter tolerances, and traceable supply chains—creating opportunities for premium pricing and value-added services.

Standards and certification: Compliance and traceability are moving from “nice to have” to “must have” in many industrial accounts. Recent certifications and standards updates impacting manufacturing operations amplify the premium placed on certified suppliers with demonstrable quality-management systems and environmental controls.

Exhibitions and knowledge flows: Trade events and industry associations remain critical nodes for innovation transfer. Several leading manufacturers used major exhibitions in early 2026 to debut carbide tooling and precision milling systems—signaling that product innovation and customer engagement will continue to drive differentiation.

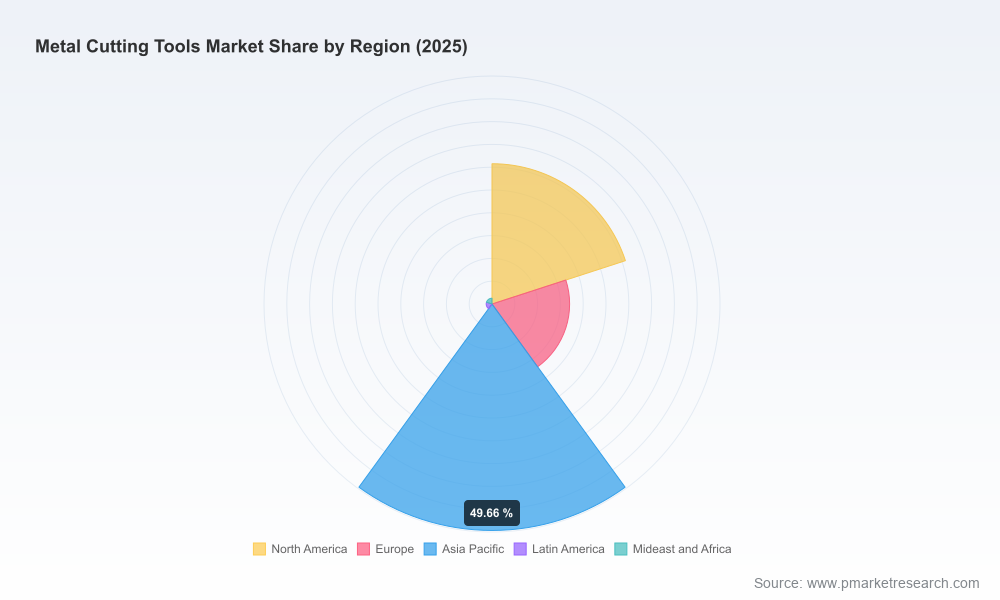

The metal cutting tools market is characterized by a broad set of global players, a deep tier of regional specialists, and a growing number of service-led newcomers. Market concentration remains moderate: the top three players account for roughly one-quarter of the market, and the top five just under a third—an environment that encourages both scale-driven investments and targeted niche plays.

Kennametal Inc. (Pittsburgh, PA, United States) — A leader in indexable inserts, carbide tooling, milling cutters, and holemaking tools. Kennametal’s emphasis on application engineering and system-level tooling solutions positions it well where customers demand integrated productivity gains. (https://www.kennametal.com)

Sandvik AB (Stockholm, Sweden) — A prominent supplier of carbide inserts, turning and milling tools, and advanced metal cutting systems. Sandvik’s R&D and global service footprint offer scale advantages in high-mix, high-precision environments. (https://www.sandvik.com)

ISCAR Ltd. (Tefen, Israel) — Known for advanced carbide inserts, drills, and indexable solutions, ISCAR combines material know-how with aggressive product cadence; its full-facility certifications underscore a quality and environmental compliance narrative important to OEM procurement. (https://www.iscar.com)

OSG Corporation (Nagoya, Japan) — Specializes in high-performance drills, taps, and end mills. OSG’s strengths are in tooling for complex part geometries and high-speed machining strategies. (https://www.osg.co.jp)

Walter AG (Tübingen, Germany) — Offers indexable inserts, turning and milling tools, and modular systems; Walter’s modularity approach reduces buyer complexity for mixed-cell manufacturing. (https://www.walter-tools.com)

Ceratizit Group (Mamer, Luxembourg) — A producer of carbide tools and inserts with a strong focus on performance coatings and specialty geometries, enabling tailored solutions for higher-value segments. (https://www.ceratizit.com)

TaeguTec Ltd. (Daegu, South Korea) — Supplier of carbide inserts, drills, and advanced cutting tools, with a notable presence in Asian manufacturing hubs and a growing emphasis on aftermarket and service capabilities. (https://www.taegutec.com)

These incumbents are complemented by regional specialists and emerging suppliers that leverage localized manufacturing, aftermarket reconditioning, and digital-enabled services. Competitive advantages in 2026 will accrue to firms that combine materials science, tooling systems integration, and predictable supply assurance.

March 2026 industry reporting flagged a notable year-over-year increase in US cutting tool shipments and underscored raw-material shortages affecting industry sentiment. This has direct implications for inventory strategies and lead-time assumptions.

Early 2026 trade shows and exhibitions saw leading suppliers showcase next-generation carbide end mills, drills, and precision inserts—evidence that innovation cycles remain active even amid material cost pressures.

Action-oriented market forecasts calibrated to procurement and capital-expenditure cycles—ready to plug into 2026 budget models.

Scenario-based raw-material stress tests that quantify margin shock under different tungsten-carbine and high-speed-steel availability assumptions, plus recommended hedging and supplier diversification tactics.

Competitive playbooks for global leaders and regional challengers—detailing likely moves across product innovation, aftermarket services, and channel strategies.

Commercial due-diligence templates for evaluating M&A and partnership targets, emphasizing technology fit, manufacturing footprint, and customer retention mechanics.

Go-to-market roadmaps for premiumization strategies—how to shift from commodity selling to solution-based value capture in high-precision segments.

Supply-chain resilience checklists including recommended contract structures, inventory buffers by risk category, and supplier scorecards tied to quality and compliance metrics.

Rebalance supplier portfolios: Prioritize multi-sourced supply positions for critical raw materials, while locking in strategic volumes with preferred partners to stabilize unit costs.

Invest selectively in premium tooling and services that improve customer throughput—the ability to demonstrate cycle-time or scrap reduction will command price premiums and stickier relationships.

Strengthen certification and traceability pathways: As buyers increasingly demand certified supply chains, investments in ISO and similar frameworks will reduce procurement friction and open higher-margin accounts.

Leverage trade-show and association engagement: Use 2026 industry events and association initiatives to accelerate product validation, gather competitive intelligence, and secure pilot customers for new tooling solutions.

Model for volatility: Incorporate scenario stress-testing for raw-material price spikes into 2026 planning and ensure pricing models can be adjusted with transparent inflation pass-through mechanisms.

The metal cutting tools market in 2026 is not a static arena of incremental volume growth; it is a dynamic landscape where material scarcity, certification demands, and product innovation intersect. Companies that combine disciplined procurement, targeted product premiumization, and service-oriented commercial models will outperform peers even in an environment of moderate CAGR growth. PW Consulting’s comprehensive study equips leaders with the quantitative forecasts, competitive diagnostics, and operational playbooks required to convert market momentum into lasting advantage.

This preview highlights the strategic contours and executable themes in our full Metal Cutting Tools Market study. For the granular segmentation, regional and application-level analytics, supplier scorecards, and the detailed financial models that inform 2026 decisions, please consult the full report available on our research portal. The full dataset includes scenario analyses and downloadable templates you can integrate directly into planning and procurement workflows.

For detailed analysis of this topic, please visit the official page:Metal Cutting Tools Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com