Nafion Market 2026: Strategic Preview for Executive Decision‑Making

As global energy transition priorities accelerate, Nafion — the perfluorosulfonic acid polymer family that underpins critical electrochemical technologies — has moved from niche specialty material to strategic industrial input. PW Consulting’s latest Nafion Market study (base year 2025, forecast 2026–2032) synthesizes five years of historical tracking and forward-looking scenario work into a decision-grade briefing for corporate leaders, investors, and policy teams. This preview explains why the study matters for decisions in 2026, what unique practical outputs the full report delivers, and how executives should translate the market trajectory into concrete choices.

Nafion Market

Market snapshot: a rising, investible market

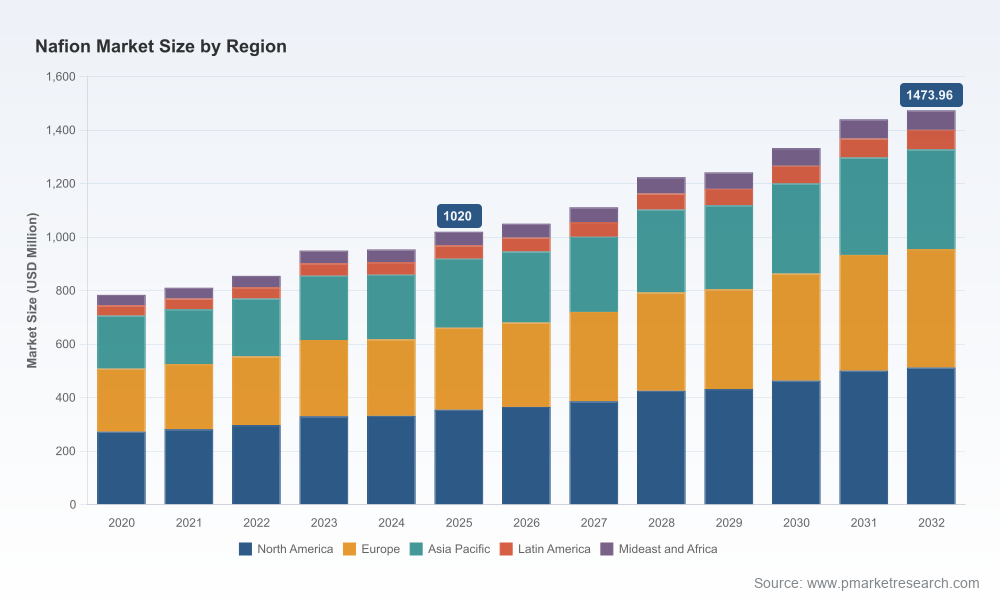

By the study’s base year (2025) the global Nafion market reached a material scale in monetary terms, reflecting steady expansion from the start of the decade. Historical figures show a clear, compounding upward trend between 2020 and 2025; our forecast projects sustained growth through 2032 driven by fuel cell and electrolyzer deployment, regulatory support for hydrogen infrastructure, and incremental adoption in chlor‑alkali and specialty industrial applications. The model uses a central CAGR of 5.4% across the 2026–2032 forecast window and produces a near‑term and long‑term view that supports both capital planning and supply‑chain strategies.

Nafion Market

Two facts anchor the investment case: (1) the market has moved past early adopter dynamics into structural growth, and (2) supplier concentration remains significant, meaning supply risks and supplier strategies meaningfully affect downstream costs and project economics. These macro features — not the individual segment mechanics — are what make Nafion a strategic procurement and technology risk for 2026 planning cycles.

Nafion Market

Why this study is essential for 2026 corporate strategies

- Timing of capital commitments: Large‑scale hydrogen and fuel‑cell projects entering FEED and final investment decision stages in 2026 must include Nafion availability, lead time, and cost trajectory in their NPV models. Our forecast and sensitivity modules quantify how material price and availability swings propagate through project IRRs.

- Sourcing and supplier selection: With a concentrated supply base, vendor selection and diversification strategies are high‑impact levers. The study evaluates supplier roles, capability gaps, and credible alternative pathways to de‑risk procurement.

- Innovation prioritization: For manufacturers of membranes, MEAs, and related stacks, the study identifies where incremental R&D yield translates into commercial advantage — whether through cost reductions, lifetime improvements, or integration benefits with system‑level designs.

- Regulatory and market access planning: Public hydrogen strategies and carbon‑reduction mandates are driving demand for Nafion‑dependent technologies; the report maps policy‑led demand pockets to help prioritize market entries and advocacy efforts.

What the full report delivers — practical, transaction‑oriented outputs

PW Consulting’s Nafion Market study is explicitly built as an operational toolkit for 2026 decisions, not an academic survey. Key deliverables include:

- Transparent market size and growth model (2020–2025 historical series; 2026–2032 forecast) with downloadable scenario runs that let you stress price, demand, and policy variables.

- Detailed supply‑chain maps and lead‑time heatmaps that identify single points of failure, capacity bottlenecks, and alternate sourcing routes.

- Competitive landscape deep dives on incumbent manufacturers, authorized distributors, and value‑added processors — including capability matrices, strategic positioning, and near‑term investment posture.

- Commercial benchmarking tools for procurement teams: price benchmarking ranges, contract clause templates for long‑lead materials, and an expected total cost of ownership framework for membrane procurement.

- Scenario playbooks (base‑case, constrained supply, accelerated adoption) with recommended tactical responses for procurement, sourcing, R&D, and M&A activity.

- Regulatory and incentive mapping tied to project economics — enabling teams to quantify how policy support changes payback periods across hydrogen and fuel‑cell projects.

- Executive dashboards and investor briefing packs to accelerate board‑level decisioning and fundraising conversations.

To preserve the strategic utility of the work across competitive readers, the full report retains the granular regional and application‑level splits and exact pricing curves behind paywalled data tables and interactive models.

Competitive dynamics: who matters and why

The Nafion ecosystem is characterized by a small number of high‑capability suppliers and a set of specialized downstream players who add manufacturing and application expertise. Market concentration metrics indicate a dominant tier of suppliers that collectively control a substantial portion of global supply; this structure amplifies the strategic importance of supplier moves.

- The Chemours Company (Wilmington, Delaware) — the original developer and primary manufacturer of Nafion™ materials, spanning membranes, dispersions, and resins. Chemours’ corporate results and segment reporting are leading indicators for capacity utilization and pricing trends. Recent communications and industry engagements suggest the company is actively aligning supply strategy with hydrogen economy demand.

- Ion Power, Inc. (New Castle, Delaware) — an authorized distributor and value‑added manufacturer focused on electrochemical applications. Ion Power’s position highlights the importance of distributors and toll‑processors in providing rapid access to membrane forms and sub‑assemblies.

- Perma Pure LLC (Florida) — specialized in Nafion® tubing and gas‑conditioning components; a reminder that Nafion’s commercial footprint extends beyond membranes into engineered system components where form‑factor and durability matter.

- Beantown Chemical (Hudson, New Hampshire) — a supplier focused on research materials and small‑volume membrane products, catering to R&D pipelines and early‑stage commercialization efforts.

The competitive analysis in the full report dissects capability stacks (R&D, scale manufacturing, downstream processing), contractual behavior (willingness to enter long‑term offtake, tolling, or licensing), and strategic intent (capacity expansion, vertical integration). For example, recent industry disclosures and company reporting are triangulated to assess how supplier financials and technical collaborations will affect availability for large electrolysis and fuel‑cell programs.

Dynamics shaping supply, price, and risk in 2026

- Input cost volatility: Raw material and energy cost shifts materially affect per‑unit economics for Nafion production. Our stress tests show that price swings materially impact project economics for large electrolyzer and fuel‑cell deployments unless hedging or long‑term contracts are in place.

- Policy tailwinds: National and regional hydrogen strategies are accelerating demand in targeted infrastructure corridors. These policies create predictable adoption windows but also concentrate demand geographically, amplifying short‑term logistics and allocation risk.

- Capacity response: Major suppliers have signaled and executed capacity expansions to support the hydrogen economy. The timing and scale of these investments — and the lead times to bring them on stream — are central to our supply scenarios.

- Commercial pricing structure: Nafion remains a premium, engineered input. The full report provides procurement teams with benchmarking bands and negotiation levers appropriate for 2026 contracting cycles.

Strategic implications and recommended actions for 2026

For executives making decisions in 2026, the study’s synthesis points to a set of prioritized actions:

- Lock in strategic supply for anchor projects: For capital‑intensive hydrogen projects, secure material through multi‑year agreements or volume frame contracts tied to performance milestones. Use the report’s contract templates and TCO tool to structure defensible commercial terms.

- Design for material flexibility: System integrators should design stacks and balance‑of‑plant for membrane variants and supply contingencies — enabling substitution or phased upgrades without major redesign costs.

- Pursue supplier partnerships: Consider JV, equity, or strategic partnership structures with membrane manufacturers or toll processors to ensure prioritized capacity and knowledge transfer. The report profiles partnership archetypes and valuation implications.

- Protect against input risk: Implement a layered hedging approach that combines long‑term contracts, multi‑sourcing where feasible, and options for inventory buffering calibrated to project cashflow profiles.

- Prioritize R&D paybacks: For materials and stack OEMs, prioritize R&D efforts that improve durability and reduce per‑cycle costs, as these have outsized impact on life‑cycle economics compared with incremental material cost cuts.

How to use this preview and where to find more

This article is a tactical preview: it demonstrates the study’s analytical depth and the type of operational outputs your team can deploy in 2026 planning, while intentionally withholding micro‑segmentation tables and raw price curves that are central to competitive advantage. The full PW Consulting Nafion Market report includes downloadable datasets, interactive scenario models, and layered segmentation (by region, product type, and end‑use) that executives will need to finalize procurement schedules, capex approvals, and partner negotiations.

If your 2026 roadmap depends on predictable Nafion supply, material cost assumptions, or supplier contracting, the full report will accelerate decision‑making and materially reduce execution risk. PW Consulting’s advisory team is available to run a customized workshop to apply the model to your portfolio and produce a prioritized set of actions tied to your risk appetite and timing constraints.

In an industry where a small number of material choices can determine project viability, having a precise, actionable view of market scale, trajectory, and supplier behavior is not optional — it is a table stake for any organization seeking to lead in hydrogen, fuel cells, or related electrochemical markets in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Nafion Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com