Asia-Pacific Water Purifier Market Overview: Key Drivers and Challenges

Other |

2026-03-09 04:35:58

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused, executive-grade introduction to our new Heat Guns Market study. This preview translates robust market intelligence into boardroom-ready implications for 2026 planning cycles. It highlights why heat guns—once a niche hand-tool—have become a strategic product line for manufacturers, channels and industrial end-users, and it frames the decisions leadership teams must prioritize this coming year. To preserve the commercial value of the full study, this piece demonstrates analytical depth while intentionally withholding the granular segment tables and proprietary model outputs that subscribers will find on the report page.

Heat Guns Market

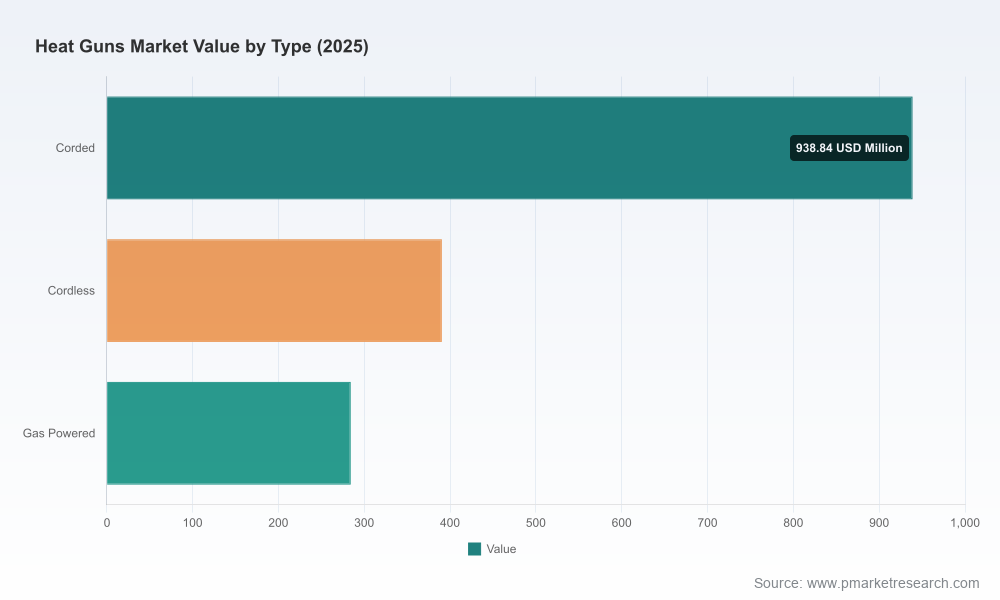

The global heat guns market has shown resilient expansion across the 2020–2025 historical window, growing from USD 1,312.48 Million in 2020 to USD 1,613.61 Million in 2025 (base year). Our outlook projects continued expansion through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 4.3%, with the market reaching approximately USD 2,185.83 Million by 2032. These headline metrics reflect a market that is neither hyper-booming nor stagnant—rather, it is maturing, driven by incremental product innovation, steady industrial demand, and structural shifts in energy and tool electrification.

Heat Guns Market

Market structure matters: concentration is meaningfully high. The top three players account for roughly two-thirds of market revenue, while the top five control nearly four-fifths. This concentration creates a competitive landscape in which scale, channel access, and product breadth materially affect outcomes for challengers and incumbents alike.

Heat Guns Market

Portfolio prioritization: With steady but selective growth, heat guns are now a strategic line for companies looking to balance volume with margin. Decisions on R&D allocation (battery integration, temperature control, ergonomics), SKUs to keep, and SKUs to sunset should be informed by forward-looking demand curves—precisely the type of output embedded in our full study.

Channel and commercial model choices: The market rewards companies that tailor distribution to end-user workflows—industrial procurement versus trade and DIY channels require different packaging, warranty models, and aftermarket services. Our research maps these distinctions and shows where pricing power resides.

M&A and partnership focus: High concentration and technology-driven differentiation make targeted M&A or strategic partnerships an efficient route to scale or capability. Our report includes a prioritized M&A screen and partnership playbook designed for 2026 execution windows.

Supply chain resilience: Manufacturers must manage component exposure (heating elements, electronics, battery cells, polymers) and geographic supply nodes. The study lays out supplier-risk heatmaps and contingency levers to preserve time-to-market and margins.

Technological substitution and batteryization: The march toward cordless, battery-powered tools is accelerating. Improvements in battery energy density and thermal management reshape product form factors and open new usage occasions—particularly in environments where tethered power is a constraint. Expect cordless iterations to command premium positioning in certain professional segments.

Industrial process optimization: Heat guns are increasingly used as precise process tools—hot-air shrink, localized heating, paint removal, and polymer forming. Industry 4.0 trends are nudging customers toward models with tighter temperature control, diagnostics, and serviceability.

Aftermarket and service revenue: As buyers seek lifecycle value, warranties, consumables (nozzles, filters) and refurbishment services become levers for revenue capture beyond the initial sale. Prioritizing these channels materially improves customer lifetime value.

Regulation and safety standards: Evolving safety codes and product testing frameworks are lifting the bar for certifications and labeling—creating a dual effect of increasing seller costs while raising entry barriers for low-cost suppliers.

Price and raw-material cyclicality: Elemental inputs and electronics remain exposed to commodity cycles. Operational strategies that blend local sourcing, hedging, and modular design reduce margin volatility.

The market features several global manufacturers with complementary strengths. Our competitive analysis evaluates product portfolios, R&D positioning, channel footprints, and strategic intent. Highlights include:

Makita Corporation (Japan): Known for professional-grade cordless solutions, Makita’s emphasis on battery integration and ruggedization positions it well with trade professionals who demand portability and endurance. Their strength lies in engineered reliability and a hardened distribution network across professional channels.

Robert Bosch GmbH (Germany): Bosch combines broad product breadth with strong brand equity in precision and safety. Its variable-temperature models and focus on user ergonomics make it a go-to in both industrial and premium DIY segments.

Stanley Black & Decker, Inc. (United States): With a diversified tools portfolio and deep channel relationships in construction and manufacturing, Stanley Black & Decker leverages scale to optimize cost-to-serve and aftermarket offerings.

Techtronic Industries (Hong Kong): TTI’s capability in delivering cordless and energy-efficient designs, combined with fast product cycles, makes them a rapid commercialization partner for new battery-driven form factors.

Apex Tool Group (United States): Apex’s industrial and automotive tool focus creates a stable demand base for application-specific heat guns, particularly where customization and OEM integration are valued.

Koki Holdings (Japan): Koki emphasizes professional hot-air tools with serviceable designs; their competitive advantage is in field-serviceability and trade-focused performance claims.

Across these players, we identify recurring strategic moves: consolidation of cordless platforms, selective vertical integration for batteries and electronics, expansion of aftermarket services, and selective channel deepening. For challengers, the gap to scale often lies less in product engineering and more in distribution reach, brand recognition, and aftermarket frameworks.

Our Heat Guns Market report is engineered for immediate operational and strategic use by executives, product managers, and business development teams. Key deliverables include:

Granular demand model (historical 2020–2025, forecast 2026–2032) with scenario toggles for energy costs, battery adoption rates, and regulatory shifts.

Competitive benchmarking heatmap—R&D focus, channel strength, price positioning, and aftermarket strategy—mapped to practical moves for incumbents and entrants.

Go-to-market playbooks for industrial, trade, and retail channels, including SKU rationalization guidance, promotional cadence, and distributor incentive structures.

Cost-to-serve and margin-preservation levers, with case-level simulation tools for product redesigns and sourcing reconfiguration.

M&A and partnership screen with prioritized capability gaps and the financial criteria we recommend to evaluate targets for 2026 action.

Regulatory and compliance checklist tailored by product class and suggested product-architecture responses to meet anticipated 2026 safety changes.

Note: We intentionally withhold segmented regional and application-level tables in this preview; the full dataset and interactive models are available through the report portal and are essential for transaction- and investment-level decisions.

Commit to cordless R&D where it intersects with professional use-cases: Prioritize battery thermal management and modular battery platforms that can be shared across tool ecosystems. Time-to-market advantage will convert into durable share gains.

Monetize aftermarket and services: Institute consumable bundles, extended warranties, and field-repair programs to capture recurring revenue and deepen customer ties.

Optimize channel segmentation: Align SKU strategy with distribution economics and buyer willingness-to-pay. For high-volume industrial accounts, emphasize total-cost-of-ownership; for retail, emphasize ease-of-use and safety credentials.

De-risk supply chains: Dual-source critical components, bring final assembly closer to key markets where margins justify it, and hedge against raw-material swings through design modularity.

Be acquisition-ready: With the market showing concentration and moderate fragmentation below the top tier, maintain a shortlist of tuck-in targets that solve capability gaps—battery tech, IoT-enabled controls, or service-platforms.

Elevate compliance & safety as product differentiators: Deploy testing and certification as a go-to-market advantage in professional channels where liability and downtime matter.

This preview is intended to crystallize the strategic opportunity set for 2026. For transaction-grade analysis—including the complete segmentation tables, downloadable model files in USD Million, and the proprietary scenario simulator—please consult the full Heat Guns Market report on our website. The full dataset is the operational asset teams will use to build FY26 budgets, prioritize R&D pipelines, evaluate M&A opportunities, and design channel strategies with quantifiable ROI.

PW Consulting combines market rigor with hands-on execution know-how. If you are evaluating portfolio moves or need a tailored workshop to translate these findings into a 90-day action plan, our consulting teams are available to collaborate.

For detailed analysis of this topic, please visit the official page:Heat Guns Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com