Precipitated Barium Sulfate Market — Strategic Briefing for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a succinct but high-fidelity briefing on the precipitated barium sulfate (PBS) market intended to shape executive choices in 2026. This note synthesizes market scale evolution, supply-and-demand dynamics, competitive posture, and pragmatic next steps. It deliberately emphasizes analytical depth while withholding granular segmentation tables and proprietary models — the precise breakdowns and scenario decks are available in the full report on our site.

Why this market matters to your 2026 agenda

- PBS is a strategic filler and functional additive across paints & coatings, plastics, rubber, and select industrial and healthcare uses. Its behavior often foreshadows margin pressure and formulation trade-offs across customer value chains.

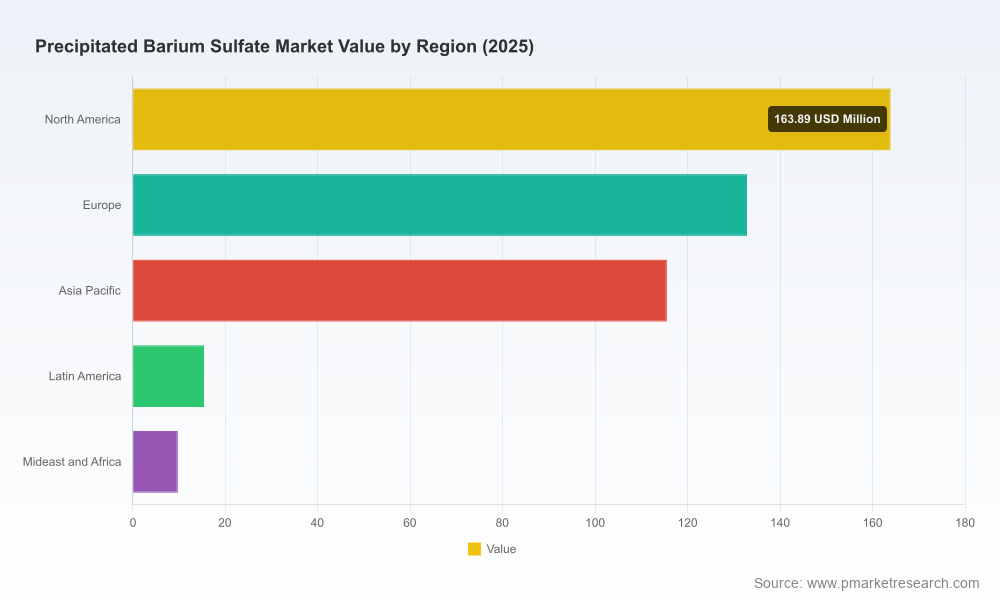

- After a steady recovery period through the early 2020s, the global PBS market reached USD 437.4 Million (base year 2025, revenues expressed in USD Million). Our historical series shows expansion from USD 356.25 Million in 2020 to that 2025 level, and our forecasts project continued growth to USD 583.94 Million by 2032. The forecast period (2026–2032) assumes a compound annual growth rate (CAGR) of 4.16%.

- For 2026 strategic planning, this combination of steady absolute expansion and moderate CAGR means opportunity for margin-capture through operational leverage, but limited room for demand-driven volume surges without focused investments or differentiation.

High-level market trajectory and implications

The market’s trajectory — recovery to 2025 followed by mid-single-digit growth through 2032 — implies a maturing product lifecycle where competition shifts from pure volume to value: specialty grades, purity, and service-led supply arrangements. Procurement teams should expect pricing cycles to be influenced more by input-cost pass-throughs and logistics than by sudden demand shocks.

Implications for 2026 planning include prioritizing three strategic levers: (1) product differentiation through modified and nano grades, (2) tighter integration with key customers via formulation support and anchored contracts, and (3) selective capacity investments where scale and proximity to end markets can provide defensible cost advantages.

Supply-side dynamics shaping near-term strategy

- Input-cost and logistics inflation is front-and-center. Bulk-freight and container cost inflation has raised delivered commodity barite and feedstock prices in import-dependent markets. The knock-on effect increases the marginal cost of producing precipitated grades, compressing margins for unconsolidated players.

- Specific raw-material pressures — including rising antimony and other specialty inputs — are exerting upward pressure on PBS pricing and are cited as proximate causes of supplier price actions in 2024–2025.

- Producers have already signaled and implemented price adjustments. Notably, several major suppliers announced price increases in March 2025 citing raw material and production cost escalation, and other suppliers implemented increases that became effective in early 2025. These moves indicate a willingness among leading producers to protect margins even at the expense of slower near-term volume growth.

- Capacity dynamics are nuanced: selective capacity additions were executed in 2024 by major European players, expanding production capability by meaningful increments. These moves reflect confidence in long-term demand for higher-performance grades and are a signal that competition may intensify in specific subsegments.

Demand-side shifts and product positioning

Demand is increasingly segmented by performance and regulatory attributes rather than only price. End-markets are evolving: coatings and paints seek optical and rheological performance; plastics buyers weigh density, whiteness, and dispersion advantages; specialty industrial uses demand fine-particle and nano-grade solutions. Healthcare and specialty industrial uses, while smaller in absolute terms, are rising in strategic importance because they allow higher margins and longer contract durations.

From a product strategy standpoint, executives should assess portfolio balance between commodity precipitated grades and modified/nano grades. The latter can command premium pricing but require R&D, tighter environmental and quality controls, and closer collaboration with customers on formulation engineering.

Competitive landscape — concentration and player profiles

The PBS market is moderately concentrated. The top three players account for a significant share of the market, and the top five consolidate just over half of global capacity. This competitive structure creates both opportunities and constraints: scale players exert pricing leadership and can absorb short-term cost volatility, while nimble regional producers can exploit service agility and localized feedstock advantages.

- Cimbar Performance Minerals (Chatsworth, Georgia, USA) — A leading North American producer, Cimbar supplies PBS across paints, coatings, plastics, printing inks, and lead-acid battery sectors. The company exercised pricing discipline, announcing a structured increase on specialty minerals that took effect in early 2025, signaling margin-protection priorities.

https://cimbarresources.com

- Nippon Chemical Industrial Co., Ltd. (Tokyo, Japan) — Known for high-purity precipitated barium sulfate aimed at precision industrial applications; their focus on quality and consistency is a competitive moat in specialty use-cases.

https://www.nippon-chem.co.jp

- Shanghai Tengmin Industry Co., Ltd. (Shanghai, China) — A major regional supplier that positions PBS as a primary filler for paints, coatings, and pigment systems. Their scale and proximity to large regional demand pools are advantages in price-sensitive segments.

https://www.tengminchem.com

- Hubei Qinba Advanced Materials Co., Ltd. (Hubei Province, China) — Specializes in synthetic PBS for high-performance powder coatings and industrial uses; recent commercial behavior — including price adjustments announced with peers — illustrates the balancing act between cost pass-throughs and volume retention.

Company profile link

Recent developments underscore market sensitivity: price increases announced by several major suppliers in 2024–2025 and capacity additions by a major European producer in 2024. For competitive strategy, such developments mean suppliers with upstream integration or logistics control can sustain tighter margins, while smaller players face margin compression unless they specialize.

What our PW Consulting report delivers (practical, executive-ready content)

- Validated historical time series (2020–2025) and scenario-based forecasts for 2026–2032 (base year 2025; revenues in USD Million). We present both a baseline and two downside/upside scenarios which incorporate logistics, raw-material shocks, and regulatory stress-tests.

- Actionable commercial playbooks: pricing playbook for contract negotiations, recommended hedging approaches for critical inputs, and customer-segmentation tactics for prioritizing sales engineering resources.

- Supply-chain heatmaps that identify import-dependent corridors, logistics pinch-points, and feedstock vulnerability clusters — with prioritized mitigations by investment type (e.g., buffer inventories, proximate tolling partnerships, or JV-based feedstock security).

- Competitive benchmarking: capability matrices for major suppliers, gap analysis against premium-grade requirements, and a short-list of acquisition or partnership targets by strategic rationale.

- Regulatory and sustainability assessment that maps current rules to near-term compliance cost impacts and product labeling risks — critical for customers in European and North American end-markets.

Recommended 90-day actions for 2026 planning cycles

- Run a margin-at-risk drill: quantify the P&L impact of a further 5–15% sustained feedstock inflation and simulate pass-through scenarios to principal customers. Use the report’s sensitivity matrices to shortcut scenario runs.

- Segment your customer base by price elasticity and technical dependency. Reallocate commercial engineering resources toward customers where PBS performance materially increases switching costs.

- Assess logistics and sourcing: where import dependency is high, evaluate localized supply contracts, dual-sourcing, or toll-manufacturing options to reduce delivered-cost volatility.

- Pursue at least one product-differentiation initiative (modified or nano-grade) with a named anchor customer under a co-development term-sheet within 90 days. The report provides a prioritized list of target formulations and potential partners.

- Prepare procurement contracts with clear indexing to feedstock cost indices and discrete cadence for renegotiation — a practical mitigation against ad hoc price shocks of the type observed in 2024–2025.

How PW Consulting can accelerate your 2026 outcome

Our full Precipitated Barium Sulfate Market report contains the detailed segmentation tables, regional and application-level demand breakouts, supplier capacity maps, and proprietary pricing intelligence that are intentionally omitted here to preserve strategic exclusivity. Those core data sets underpin the playbooks and scenario models referenced above. If your 2026 planning requires transaction-ready analytics (M&A target shortlists, contract-negotiation templates, or capex prioritization models), our team can deliver tailored workshops and a one-week decision pack built from the report’s datasets.

To access the complete dataset, proprietary segmentation, and downloadable scenario models, please consult the full report page on our website. The “preview” you’ve read is designed to give you authoritative insight and immediate strategic direction while reserving the granular intelligence that unlocks high-confidence decisions.

Closing synthesis

In 2026, PBS will not be a headline growth market, but it will be strategically important across multiple industrial value chains. The macro numbers indicate predictable, steady expansion — but the near-term strategic battleground will be margin protection, feedstock security, and product differentiation. Executives who treat PBS not as a commodity cost but as a portfolio of differentiated offerings — and who act quickly to secure logistics and supply arrangements — will convert modest market growth into outsized commercial returns.

PW Consulting stands ready to support transaction diligence, commercial transformation, and tailored forecasting needs. For the full intelligence suite, including the withheld segmentation tables and scenario models, please access our full report.

For detailed analysis of this topic, please visit the official page:Precipitated Barium Sulfate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com