Copper Sulfate Pentahydrate Market — Strategic Outlook for 2026 Decision-Makers

The copper sulfate pentahydrate market is at an inflection point. After steady recovery through the early 2020s, total global revenues expanded from approximately USD 315.2 Million in 2020 to about USD 402.5 Million in 2025, and our base-case forecast projects a continuation of disciplined growth to roughly USD 576.8 Million by 2032 — implying a compound annual growth rate (CAGR) of 5.4% across the 2026–2032 forecast horizon. For senior leaders planning capital allocation, procurement strategy, product development or M&A in 2026, this report provides the line-of-sight required to convert market momentum into defensible strategic choices.

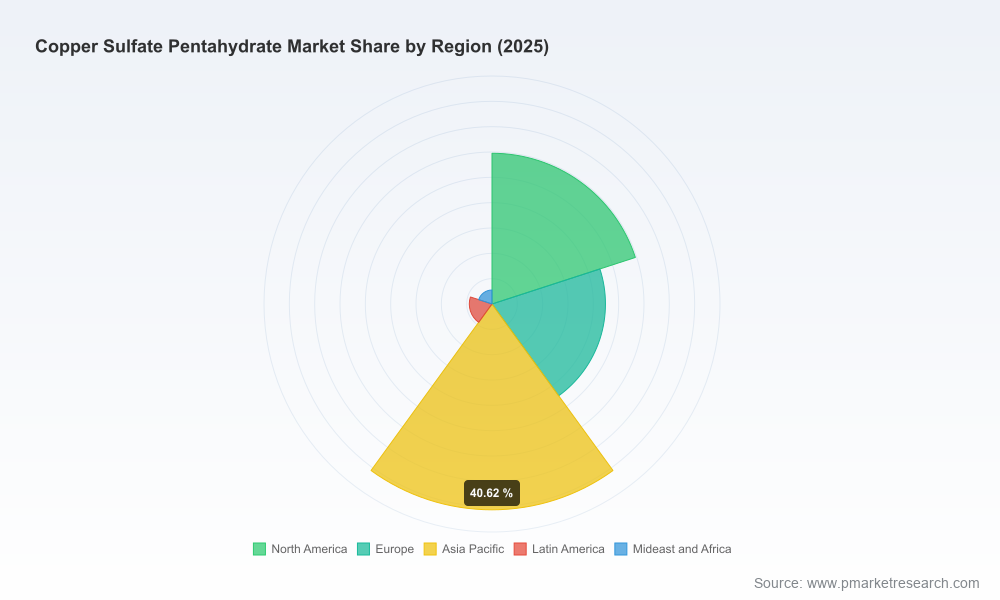

Copper Sulfate Pentahydrate Market

Why this moment matters

Copper sulfate pentahydrate uniquely sits at the intersection of agricultural input cycles, aquaculture expansion, industrial surface-finishing demand and stricter environmental/regulatory scrutiny. That multi-industry exposure creates both upside and exposure: predictable demand drivers from crop protection and aquaculture are counterbalanced by episodic risks in feed safety and raw-material quality that can quickly shift sourcing preferences and regulatory responses. The market’s mid-single-digit CAGR reflects this balanced dynamic — stable, but sensitive to supply-chain shocks and policy shifts.

Copper Sulfate Pentahydrate Market

How PW Consulting’s research helps 2026 decision-makers

- Executive prioritization. We translate market growth and volatility into actionable priorities for procurement, product teams and corporate development. If your horizon is 1–3 years, the report highlights supply continuity and compliance levers; for 3–5 year horizons, it emphasizes capacity positioning and adjacency plays.

- De-risking operational plans. The research distills the most probable near-term disruptions (regulatory recalls, contamination events, concentrated upstream supply) and prescribes mitigations such as dual-sourcing tiers, supplier audits, and inventory policy adjustments calibrated to each business model.

- Investment decision support. Our scenario-backed revenue and margin projections give private equity and strategic acquirers a transparent framework for valuation sensitivity — from conservative (safety-first) to aggressive (growth-capture) plays.

- Go-to-market and product roadmaps. Manufacturers and distributors can use the report’s granular qualitative intelligence to refine grade mix, customer segmentation, and channel strategies — for example, prioritizing high-value electroplating formulations where regulatory thresholds and technical specs create higher margins.

Market structure and segmentation (summary)

The market is mapped across three conventional axes: region, product grade and end-use application. Product grades span agricultural, feed, industrial and electroplating specifications, each with distinct quality, documentation and traceability requirements. End markets — agriculture & forestry, aquaculture, chemical intermediates, electroplating and metal/mining uses — impose different procurement cadences and compliance burdens. The report contains a full set of historical time series (2020–2025) and granular forecasts through 2032 for each segmentation axis, but this executive overview intentionally refrains from publishing core segment figures to encourage deeper engagement with the full dataset.

Copper Sulfate Pentahydrate Market

Key strategic themes for 2026

- Supply-chain resilience is table stakes. 2026 planning should assume intermittent supply and quality incidents. Building dual-sourced supply lanes, strategic buffer inventories for high-criticality grades, and supplier scorecards that incorporate quality-certification and traceability are essential.

- Quality assurance and documentation win deals. Buyers, especially in feed and pharmaceutical adjacent markets, are raising the bar on GMP, USP/IP/FCC documentation and traceability. Suppliers who invest in certifications and visible audit trails command pricing and preferred-supplier status.

- Regulatory vigilance and rapid-response capability. Contamination or recalls can be industry-wide reputational events. Rapid recall-management protocols, transparent customer communication templates, and pre-approved remediation partnerships (labs, alternative supply) are high-leverage investments.

- Product differentiation through formulation & service. With core chemistry being well established, differentiation increasingly comes from service (technical support, dosing systems), tailored grades for niche electroplating processes, and bundled analytics for agriculture/aquaculture customers.

- Value migration toward specialty & premium grades. Where customers demand high-purity or documented provenance, margin expansion is possible. Players with the capability to produce pharmacopeial/commercially certified grades should prioritize those lines for long-term margin resilience.

- ESG and sustainability as commercial drivers. Responsible sourcing, lower-contaminant raw inputs, and reduced waste in manufacturing are becoming purchase criteria. Early adopters of cleaner-process claims can access institutional buyers and premium channels.

Competitive landscape — who to watch

The market mix includes regional specialist producers and players focusing on particular grades or channels. Notable firms we analyze in the full report include:

- Shreeji Industries (India) — A GMP-certified manufacturer producing multiple pharmacopeial and technical grades for pharmaceutical, nutraceutical, agricultural and electroplating applications. Their compliance profile and export orientation make them an important supplier in GMP-sensitive value chains.

- Sulfozyme Agro India Pvt Ltd (India) — Focused on agricultural and technical grades for plant nutrition, fungicidal use and feed additives. Their capability to serve agronomic channels is a competitive asset where localized field support matters.

- Univerical (United States) — A North American supplier of high-purity liquid and crystalline products tailored to electroplating and industrial applications. Proximity, grade specialization and service models are their differentiators in regional markets.

These and other producers operate in a market that is neither monopolistic nor highly fragmented. Leading players capture meaningful but not dominant shares — making targeted consolidation and capability-focused M&A attractive to firms seeking scale or technologic differentiation.

Regulatory & safety watch: 2026 early alerts

- Contamination and recalls. In early 2026, industry stakeholders observed voluntary recalls of contaminated feed-grade lots originating from an overseas source. Such events illustrate how single supply-chain failures can reset buyer preferences and accelerate regional reshoring or supplier qualification programs.

- Documentation mandates. Feed and pharma-adjacent customers increasingly require batch-level documentation, contaminant testing, and supplier audit trails. Suppliers lacking these systems face de-listing risk.

- Environmental controls. Tighter discharge and waste handling regulations in several jurisdictions mean producers must invest in treatment systems or face costlier compliance regimes.

Practical playbook for executives in 2026

- Procurement leaders: adopt a three-tier supplier strategy (primary, validated backup, contingency) and require harmonized quality documentation for all tiers. Negotiate inventory buffers into contracts during price-stabilization windows.

- Manufacturing and operations: fast-track investments in contaminant screening, in-line analytics and traceability systems. Establish rapid escalation pathways with customers for any non-conformance event.

- Commercial teams: position premium, certified grades to institutional buyers and communicate value via case studies that show lower total cost of ownership (fewer reworks, better yields).

- M&A and strategy: prioritize targets that either close quality/certification gaps or offer high-margin specialty grades. Smaller bolt-on acquisitions that bring documented supplier relationships in regulated channels can be accretive quickly.

- R&D and product development: focus on formulation innovations that reduce downstream contaminant risks, and packaging/delivery formats that improve dosing accuracy in agriculture and aquaculture use.

What the full PW Consulting report contains

Our full Copper Sulfate Pentahydrate Market report provides the operational detail and proprietary models behind this overview, including:

- Comprehensive historical time series (2020–2025) and modeled forecasts through 2032, expressed in USD Million, with scenario sensitivity around input-price and regulatory shocks.

- Granular segmentation by region, product grade and application with demand drivers and adoption curves for each cohort.

- Supplier landscaping with profiles, capability maps and comparative assessments of certification, capacity and distribution footprints for key players.

- Trade-flow analysis and a deep-dive into upstream feedstock dynamics, cost pass-through mechanics and freight/insurance considerations.

- Regulatory tracker and a practical FAQ addressing contamination events, recall management, and recommended supplier-audit checklists (including a curated list of red-flag indicators and mitigation templates).

- Deal-screening framework for M&A, a TCO calculator for procurement, and a 90-day tactical playbook for operational leaders responding to supply disruptions.

Methodology & scope

The study uses a base year of 2025, analyses historical performance across 2020–2025, and presents a forecast window spanning 2026–2032. All revenue figures are expressed in USD (Million). Data inputs include primary interviews with producers, distributors and end-users; trade statistics; customs flows; and PW Consulting’s proprietary demand modelling. We triangulate quantitative outputs with qualitative intelligence to create scenarios that reflect possible regulatory and supply-side shocks.

Next steps

For executives preparing 2026 business plans, the decision-relevant elements are clear: shore up quality and traceability, build flexible sourcing, selectively pursue premium grades, and treat contamination management as a core capability. PW Consulting’s full report provides the segmented demand tables, regional maps and supplier benchmarking necessary to convert these principles into concrete budgets and contracts.

To access the full dataset, segment-level forecasts, and supplier scorecards referenced here, visit the source report page or contact PW Consulting for a confidential briefing. The overview above is designed to help you prioritize—our full research delivers the transactional detail you’ll need to act.

For detailed analysis of this topic, please visit the official page:Copper Sulfate Pentahydrate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com