Workshoes Market 2026: A Strategic Preview — What Corporate Leaders Must Know

Introduction

As companies recalibrate supply chains, product portfolios, and safety compliance programs for the post-pandemic industrial landscape, the workshoes market has quietly returned to a zone of steady expansion. PW Consulting’s new Workshoes Market study (base year 2025) synthesizes seven years of historical behavior and a seven‑year forecast to 2032, identifying the structural drivers that will shape procurement, R&D, and channel strategies through the next strategic planning cycle.

Workshoes Market

Market snapshot: scale, pace, and structural context

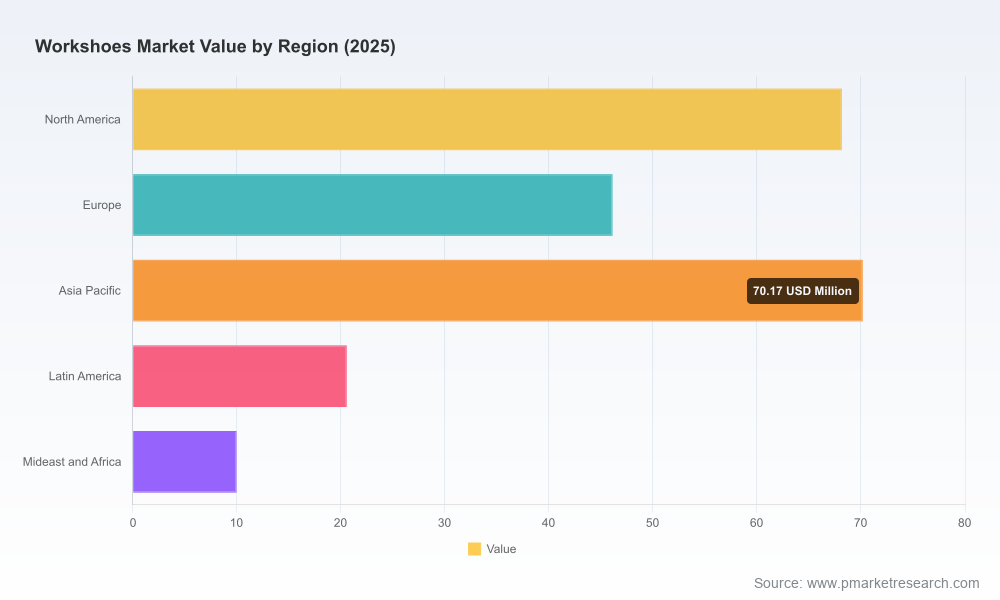

Our consolidated model places the global workshoes market at USD 215.0 Million in 2025. The market has delivered consistent year‑on‑year expansion over the 2020–2025 review period and is projected to continue on a compound annual growth rate (CAGR) of 6.98% across the 2026–2032 forecast window—reaching an overall market size north of USD 340 Million by 2032. This combination of reliable growth and manageable absolute scale creates a landscape in which targeted product innovations and distribution moves can yield outsized returns without the capital intensity required in larger equipment sectors.

Workshoes Market

Why PW Consulting’s 2026 perspective matters to corporate decision‑makers

- Actionable timing: 2026 is a hinge year—standards, raw material cycles, and trade dynamics converge such that product redesigns initiated now can reach market in time to capture the most receptive demand window.

- Risk‑reward clarity: The market’s mid‑single digit CAGR signals healthy demand, but constrained absolute scale means players must optimize margins and unit economics precisely. Our study translates top‑level momentum into practical investment thresholds for product line rationalization, manufacturing footprint adjustments, and go‑to‑market experiments.

- Compliance as a growth lever: Recent regulatory updates reshape product specification baselines; companies that align engineering and certification roadmaps with standards changes can convert compliance into premium positioning.

Core dynamics shaping 2026 decisions

- Regulatory tightening: The ASTM F2413 revision effective in 2026 raises the bar on impact, compression, and electrical hazard testing. Our review of certification authorities shows that updated thresholds—most notably higher compression resistance requirements—are already being enforced by accredited labs. Enterprises must accelerate validation pathways for existing SKUs and ensure new designs are tested against the 2026 standard to avoid product relabeling and costly market withdrawals.

- Raw material volatility: Leather, polymers, and high‑performance composites continue to exhibit price and availability volatility. Our sensitivity analysis demonstrates material input swings materially affect cost of goods sold (COGS), with composite toe constructions—using materials such as Kevlar or carbon fiber—incurring a materially higher bill of materials than steel toe alternatives. This has ripple effects on pricing strategy and margin management across commercial and industrial accounts.

- Fragmented competitive structure: Market concentration metrics indicate a fragmented competitive field. This fragmentation amplifies the strategic opportunity for scale players to pursue targeted consolidation, OEM partnerships, or licensing arrangements that capture procurement efficiencies and broaden distribution reach.

- Channel evolution: The direct‑to‑worker online channel is growing in importance, but institutional procurement (unionized buyers, large contractors, and defense contracts) remains a critical anchor for volume purchases. Differentiated channel strategies—balancing retail brand equity with B2B service offerings—are increasingly a competitive differentiator.

What this PW Consulting report contains (operationally focused)

- Detailed market sizing and validated forecasts (2026–2032) with scenario sensitivity for input cost shocks and regulatory stress tests.

- Market structure and concentration analysis with competitor benchmarking, capability matrices, and downloadable executive dashboards for rapid scenario modeling.

- Regulatory and standards playbook—stepwise compliance actions, testing timelines, and certificate renewal workflows tied to the 2026 ASTM updates.

- Commercial playbooks for channel optimization, including pricing elasticity models, bid strategies for institutional tenders, and retailer vs. D2C roll‑out decision trees.

- Capex and sourcing advisories—cost/benefit frameworks for reshoring vs. offshore manufacturing, near‑sourcing options, and supplier risk index tools.

- New product commercialization templates—recommended prototyping timelines, sample lab testing schedules, and certification gating criteria to speed product launch while minimizing regulatory risk.

Note: This preview intentionally omits full tabular breakdowns of regional, application, and type splits. Subscribers receive the complete segmentation datasets and country‑level dashboards on the report landing page.

Workshoes Market

Competitive landscape — strategic positions and tension points

The market combines long‑standing heritage brands with nimble regional players and large OEM license partnerships. Key profiles covered in the report include American heritage manufacturers (notably those emphasizing Made in USA construction and unionized production), specialized EU producers with strong chemical and heat‑resistant product lines, and a cohort of Chinese manufacturers focused on cost‑competitive volumes and composite solutions.

- Heritage U.S. manufacturers (brand premium & safety pedigree): Companies with historical manufacturing in the United States emphasize craftsmanship, materials traceability, and institutional relationships. Their strategic advantages include brand trust with industrial buyers and control of manufacturing quality. Their primary challenge is cost competitiveness versus low‑cost imports—our margin stress tests identify where premium pricing holds versus where value engineering is required.

- European specialists (technical protection & regulatory alignment): Firms with roots in polymer and composite technology are leveraging product differentiation—heat and chemical resistance, specialty polymer outsoles, and advanced protective laminates—to compete on specification rather than price. These players often lead on compliance timelines and present acquisition targets for firms seeking accelerated tech transfer.

- Asia‑based producers (scale & cost efficiency): Manufacturers in China and the broader Asia Pacific region continue to expand their industrial protective portfolios with composite toe caps and lightweight designs. Their role in the market is pivotal for volume supply; they are often the partners of choice for private label programs and major retail licensing agreements.

Recent developments that crystallize 2026 priorities

- Certification updates tied to ASTM F2413 (early enforcement by accredited labs) are already influencing product specifications on procurement sheets—companies delaying compliance re‑engineering face time‑to‑market risk.

- Trade‑show activity in late 2025 highlighted technical differentiation (e.g., new welder/foundry boots and chemical‑resistant PVC lines), indicating the premium end of the market is doubling down on high‑spec niches.

- Branded licensing moves and retail partnerships launched in 2026 show the channel dynamic shifting: major construction and general merchandise retailers are incorporating licensed work footwear collections into mass channels, compressing price points while scaling distribution rapidly.

Strategic implications and recommended 2026 actions

- Prioritize certification readiness: Map your product portfolio to the 2026 ASTM test matrix now. For SKU families that fail to meet the revised compression and impact thresholds, allocate immediate engineering sprints or sunset timelines—our report includes a prioritized remediation ladder you can apply in 60 days.

- Hedge raw material exposure: Implement dual‑sourcing for critical components (leather, polymer compounds, composite materials) and negotiate indexed price ceilings for at least one major supplier to moderate margin volatility. We provide supplier scorecards and a recommended contracting clause library.

- Rationalize SKUs by channel economics: Use our channel contribution analyses to identify which SKUs should migrate to private label, which to preserve as premium branded lines, and where hybrid licensing makes sense to retain margin while unlocking scale.

- Invest in product premiumization selectively: For markets where compliance and specification command price premiums (e.g., specialized chemical/heat work environments), prioritize development of high‑margin, certified products with clear documentation chains—these offer disproportionate EBIT uplift relative to volume plays.

- Explore M&A and partnership windows: Given the fragmented competitive picture, there are opportunity windows for acquisitive players to capture distribution and technical capabilities. Our report flags potential consolidation targets by capability map and provides a high‑level valuation methodology for initial screening.

How PW Consulting supports execution

PW Consulting offers a suite of implementation services tied to the study: rapid compliance audits, supplier risk re‑mapping, channel economics workshops, and acquisition target diligence. For leadership teams planning 2026 investment cycles, we provide a 90‑day tactical playbook that converts strategic priorities into deliverables—product certification plans, sourcing contracts, and channel piloting frameworks—ready to hand to procurement, R&D, and commercial leads.

Closing: what decision‑makers should do next

For procurement chiefs, product VPs, and corporate strategists, the key takeaway is simple: the workshoes market’s steady growth and tightening standards create a time‑limited advantage for prepared players. Companies that proactively align product design, supplier strategy, and channel economics with the 2026 regulatory and cost environment will not only avoid downside risk but can capture durable margin expansion. PW Consulting’s full Workshoes Market report provides the validated segmentation, granular scenario tables, and executable templates required to move from insight to implementation.

To access the full dataset, segment breakouts, and company‑level dashboards (including downloadable financial and regional matrices), visit our report landing page—detailed intelligence and operational playbooks are available to subscribers and clients seeking immediate execution support.

For detailed analysis of this topic, please visit the official page:Workshoes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com