Wearable ECG Monitors Market: Growth Trends and Forecast to 2029

Other |

2026-05-15 07:41:30

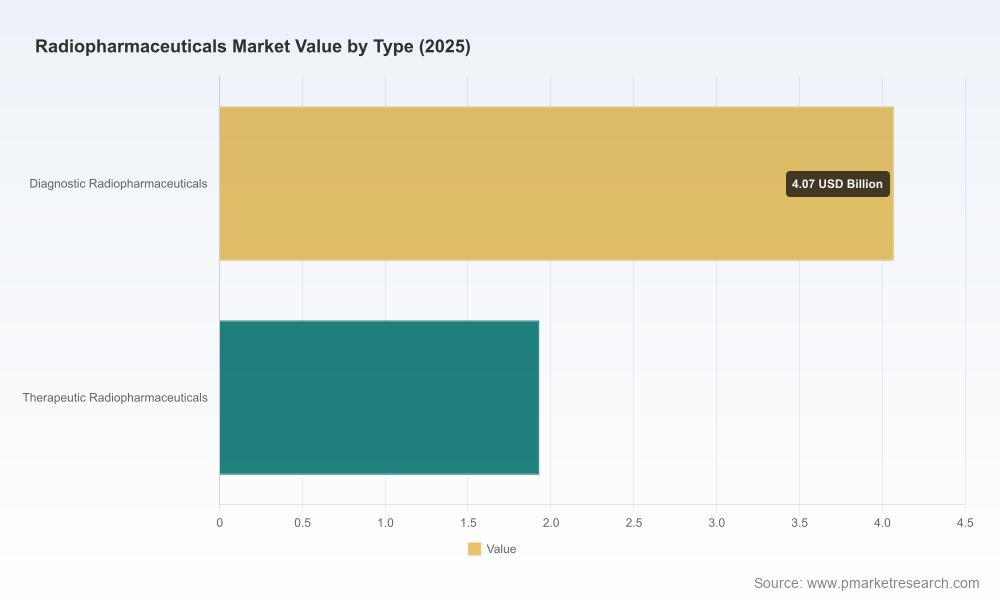

PW Consulting’s Radiopharmaceuticals Market study (base year 2025; historical 2020–2025; forecast 2026–2032) frames a rapidly maturing sector that has moved from niche clinical programs toward mainstream commercial opportunity. Total market value expanded markedly from the start of the decade and reached roughly USD 6.0 Billion in 2025; under our central scenario the market is projected to grow at a compound annual growth rate (CAGR) of approximately 8.5% across 2026–2032, reaching just over USD 10.5 Billion by 2032. These headline dynamics capture a market shaped by technology-driven clinical advances, concentrated supply-side capability, and accelerating policy incentives that together create both acute operational risks and high-return strategic opportunities for biopharma sponsors, CDMOs, and investors.

Radiopharmaceuticals Market

Policy inflection points are material to near-term economics. Recent regulatory and reimbursement moves (including an add-on payment for domestically produced Tc-99m dosing under the CY 2026 OPPS-ASC rules, and a maintained mean unit cost methodology for separately payable diagnostic radiopharmaceuticals) are shifting incentives for where and how radiopharmaceuticals are manufactured and reimbursed. Concurrent draft regulatory guidance on dosage optimization for oncology radiopharmaceuticals is raising the bar for clinical evidence strategies.

Radiopharmaceuticals Market

Trade and tariff policy has introduced a new vector of uncertainty. A Section 232 proclamation in 2026 imposing duties on certain pharmaceutical imports (with phased effective dates beginning mid‑2026) introduces a tangible commercial calculus for sponsors weighing offshore supply against onshore production or inventory buffering.

Radiopharmaceuticals Market

Supply-side constraints are no longer theoretical. Demand for therapeutic isotopes — notably Lu‑177 and Ac‑225 — continues to outpace available production capacity, and the lead time to commission new irradiation/manufacturing facilities is long. This creates both premium pricing power for secure suppliers and severe delivery risk for companies that underinvest in resilience.

Market concentration is meaningful but not absolute. The top three and top five supplier groups collectively hold a critical share of supply and technical capability, creating strategic chokepoints for certain isotopes and manufacturing services. This concentration amplifies both opportunity for vertically integrated players and counterparty risk for downstream users.

Our competitive audit focuses on companies that are shaping industrial-scale radiopharmaceutical capability today. The report provides deep profiles; below we summarize strategic positions that are consequential for partners, acquirers, and competitors.

Telix Pharmaceuticals (Melbourne) — operating GMP sites in Europe and Asia, Telix is transitioning manufacturing capability from clinical scale to commercial supply. Recent commissioning of production facilities underscores an execution playbook that blends in‑house manufacturing with hospital delivery networks.

ITM Isotope Technologies Munich SE (Garching) — vertically integrated across isotope production and radiopharmaceutical formulation, ITM’s leadership in high‑value isotopes (e.g., non‑carrier added Lu‑177 and Ac‑225) makes them a strategic anchor for oncology programs that require secure isotope sourcing.

Nucleus RadioPharma (Rochester) — a full‑service CDMO model offering development‑to‑supply logistics; attractive for sponsors seeking end‑to‑end outsourcing to compress time‑to‑clinic and commercial scale‑up risk.

Evergreen Theragnostics (Springfield) — a US‑based CDMO with a concentration on contract development and manufacturing, increasingly relevant where reshoring or tariff mitigation is a priority.

PanTera (Mol) — a JV focused on photonuclear routes to Ac‑225 precursors; operational milestones and permitting progress position PanTera among the small set of entrants that could materially expand global alpha‑emitter supply.

RayzeBio (San Diego) — developer and manufacturer centered on Lu‑177 agents, playing a role in the clinical commercialization wave for targeted radiotherapeutics.

Perspective Therapeutics (Florida) — focused on targeted alpha emitters for solid tumors; exemplifies the therapeutic‑pipeline innovation that is driving demand for scarce isotopes.

Cardinal Health (Dublin, Ohio) — a major distribution and manufacturing partner within nuclear medicine supply chains; its scale and logistics footprint are central to any commercialization strategy in markets with high regulatory and cold‑chain complexity.

Facility investments and partnerships: multiple new site commitments and joint ventures in 2024–2026 have begun to increase global installed capacity, but lead times mean meaningful relief from capacity constraints will be phased across the medium term.

Authorization and permitting progress for novel Ac‑225 production routes is a watershed for alpha‑emitter availability; where these projects succeed, they will unlock new therapeutic programs and shift supply bargaining dynamics.

Trade policy changes and tariffs introduce an immediate financial and operational risk for cross‑border supply chains; sponsors with low tolerance for supply shock may prefer onshore partners or partnerships that include contractual supply guarantees.

The report translates market dynamics into actionable steps by business function. Below are the high‑impact moves we recommend for 2026.

R&D and clinical strategy: Reassess dose‑optimization trials and comparator selection in light of FDA draft guidance; embed isotope availability and production timelines into go/no‑go criteria for Phase II–III investment decisions to avoid clinical holdouts caused by supply shortages.

Manufacturing & supply chain: Prioritize dual‑source strategies for critical isotopes, negotiate capacity reservation agreements with upstream producers, and evaluate selective vertical integration or strategic equity stakes in CDMOs that control critical isotope supply.

Commercial & reimbursement: Model the financial impact of new add‑on payments and maintained per‑day thresholds under plausible tariff scenarios; consider pricing strategies that reflect differential reimbursement across delivery settings and domestically sourced products.

M&A and partnerships: Use current market concentration to identify targets that offer supply security (isotope production), regulatory expertise, or commercial distribution capability. Structured earnouts and supply‑backed guarantees are especially valuable where regulatory or tariff risk remains elevated.

Regulatory & compliance: Fast‑track internal capability to respond to dosage optimization guidance, and prioritize contingency planning for OPPS/ASC and CMS reimbursement shifts to preserve commercial launch economics.

Our market study is structured to be immediately usable by strategy, BD, operations, and investor teams. Key deliverables include:

To preserve the strategic value of the study as a commercial product, this briefing intentionally omits detailed sub‑segment breakdowns and the granular regional allocations that underpin our model. Those tables, along with company‑level supply commitments and contract comparables, are available only in the full report and interactive model.

Short term (next 6 months): conduct a rapid supply‑security audit for all programs that rely on Lu‑177, Ac‑225, Tc‑99m and similar isotopes; secure capacity reservations where possible and update investor communications to reflect tariff and reimbursement impacts.

Medium term (6–18 months): align clinical development plans with expected regulatory guidance timelines; execute selective partnerships or minority investments in CDMOs that provide guaranteed throughput for pivotal trials and early launches.

Long term (18 months+): consider strategic vertical integration or geographic diversification of manufacturing to hedge against trade policy and supply concentration; use M&A to consolidate capability where gaps exist.

The radiopharmaceuticals sector presents a classic high‑risk, high‑return landscape: technical and regulatory complexity creates barriers, but also defensible commercial positions for firms that can secure isotope supply and navigate evolving reimbursement rules. PW Consulting’s full Radiopharmaceuticals Market study provides the quantitative underpinnings and transaction‑grade playbooks that decision‑makers need to act in 2026. For access to the complete model, segmented forecasts, supplier scorecards, and tailored advisory engagements, please consult the full report on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Radiopharmaceuticals Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com