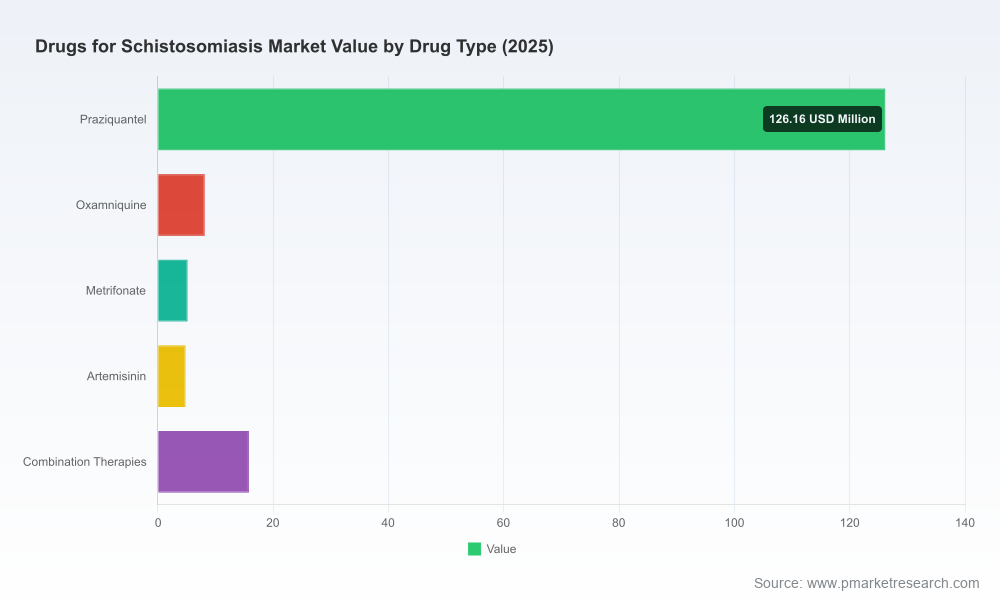

Drugs for Schistosomiasis Market: Strategic Imperatives for 2026

As PW Consulting’s Senior Strategy Advisor and Head of Industry Analysis, I present a concise, decision-focused overview of our latest Drugs for Schistosomiasis Market study. This introduction is written as a strategic “trailer”: it surfaces high-value, execution-oriented intelligence that senior executives, procurement leads, and public-health partners need to start planning for 2026 — while intentionally omitting the granular segment tables and country-level line items that live in the full report. If you are preparing procurement strategies, manufacturing investments, partnership roadmaps, or M&A diligence this year, the analysis below will help you prioritise the questions that matter most.

Drugs for Schistosomiasis Market

Market snapshot — scale, trajectory and structural cues

Between 2020 and 2025 the global market for drugs to treat schistosomiasis expanded steadily, reflecting sustained donor-funded mass drug administration (MDA), increasing programmatic focus on preschool and school-aged treatment, and expanded deployment of pediatric formulations. Our market model uses 2025 as the base year and projects the market forward to 2032. Key macro metrics from that model: the market increased consistently through the historical period and is forecast to continue growing over 2026–2032 at a compound annual growth rate (CAGR) of approximately 6.4%.

Drugs for Schistosomiasis Market

Those topline dynamics mask a market that is simultaneously concentrated and fragile: a small set of manufacturers account for a substantial share of global supply (our concentration metrics indicate a top‑three supplier concentration approaching two-thirds of the market and a top‑five concentration nearing four-fifths). That structure creates both leverage and risk for procurers and manufacturers alike — leverage in predictable tender outcomes when capacity is available, and acute supply risk when any major node is disrupted.

Drugs for Schistosomiasis Market

Why this research matters for decisions in 2026

- Supply security is now a strategic variable: 2025 saw episodic disruptions to praziquantel supply chains driven by geopolitical pressure and limited specialized capacity. For 2026, procurement teams cannot assume continuity on historical supply lines; they must design multi-vector sourcing strategies and contractual protections.

- Pediatric formulations change the playbook: New pediatric dispersible formulations have shifted NTD program dosing protocols and created differentiated procurement windows. For manufacturers, this is a product-led route to premium share; for ministries and donors, it is a programmatic lever to accelerate coverage.

- Regulatory optics determine access and price: WHO prequalification and essential-medicines listing are decisive for tender eligibility and preferential pricing in endemic countries. Achieving and maintaining those endorsements are critical milestones for market access in 2026.

- Concentration drives opportunistic strategies: High market concentration creates entry points for generic producers with cost-efficient manufacturing, and for innovators who can de-risk supply through partnerships and prequalification.

What the PW Consulting report delivers (practical, transaction-ready content)

Our report is structured to be immediately actionable for commercial, procurement, and policy teams. Key deliverables include:

- A calibrated market model (2020–2025 historical; 2026–2032 forecast) with scenario toggles for donor-funding intensity, MDA cadence, and pediatric adoption rates.

- Supply-side heat maps and a supplier-capacity scorecard that assess manufacturing footprints, WHO prequalification status, and resilience to geopolitical shocks.

- Tender-watch intelligence: upcoming national and multi-country procurement timelines; ideal bid positioning; and margin-to-win thresholds for commercial and not-for-profit tenders.

- Price and reimbursement benchmarking across buyer types (donors, ministries, NGOs), with sensitivity analysis to currency volatility and freight/logistics shocks.

- Regulatory and registration pathway guides for major endemic markets, including timelines and dossier expectations for pediatric and combination products.

- Practical playbooks for market entry: contract structuring, manufacturing partnerships, WHO prequalification strategy, and donor engagement templates.

- M&A and partnership decision frameworks: target archetypes, valuation levers, and integration risks specific to schistosomiasis drugs.

- Operational risk matrix addressing supply-chain fragility, single‑site manufacturing, API constraints, and mitigation levers including buffer inventories and dual-sourcing designs.

Note: the full report contains the granular segment splits (by region, drug type, distribution channel and end-user), country-level forecasts, and price curves. These core tables are intentionally withheld here to protect the commercial value of the dataset and to guide readers to the source report for complete intelligence.

Competitive landscape — who matters, and why

Our competitive analysis focuses on five producers whose actions and capacities will shape 2026 market outcomes:

- Merck KGaA (Darmstadt) — Merck is a strategic leader on pediatric formulations, including an arpraziquantel pediatric dispersible tablet program and WHO-prequalified supply. Recent moves — distribution of pediatric tablets into Uganda and a formal partnership with a major NTD funder — demonstrate an integrated supply-plus-program approach that accelerates adoption and creates a durable commercial channel.

- Bayer AG (Leverkusen) — As the historical marketing-authorisation holder for a widely used praziquantel product, Bayer’s production decisions materially affect European and global procurement flows. Notably, a 2025 production discontinuation in some regions prompted temporary importation measures and illustrates how a single corporate decision can ripple through procurement timelines.

- Taj Pharmaceuticals (Mumbai) — An example of resilient, cost-efficient generic supply for mass drug administration programs. Producers like Taj are positioned to win tender volume where cost and delivery speed are paramount.

- Cipla Ltd (Mumbai) — A prequalified supplier for essential medicines procurement, Cipla occupies the intersection of quality assurance and scale — a decisive position for major donor-backed tenders.

- Shin Poong Pharmaceutical (Seoul) — A longstanding manufacturer of generic praziquantel formulations, active in global supply chains and a competitive alternative for buyers seeking diversified sources.

Collectively, these firms illustrate two market truths: first, control of prequalification and product-format innovation (e.g., pediatric dispersibles) confers sustained access advantages; second, generic cost-competitive producers will continue to dominate volume tenders unless capacity bottlenecks or regulatory barriers constrain them.

Dynamics and disruptive risks to prioritise in 2026

- Geopolitical and logistics shocks: Periodic export restrictions and transit delays in 2025 demonstrated how fragile single-sourced supply can be. Scenario planning for 2026 must assume intermittent disruptions and embed contingency inventory and alternate logistics routes.

- Manufacturing and patent dynamics: Patent expirations in earlier cycles have already enabled multiple regional manufacturers to enter tenders. Expect continued price pressure and procurement arbitrage unless value-added formulations or service bundles alter buyer preferences.

- Donor strategy shifts: Changes in donor allocation or a reorientation towards integrated NTD packages can materially change demand profiles. Close engagement with major funders and program partners is essential for demand sensing.

- Regulatory levers: WHO prequalification remains the most powerful facilitator of access and preferential pricing. Products lacking prequalification face restricted participation in many tenders regardless of price advantage.

Recommendations — prioritized actions for 2026 decision cycles

- Lock multi-sourced supply for critical tenders: Negotiate layered contracts (primary supplier + nominated secondary) and include force‑majeure and inventory-release triggers to mitigate disruption risk.

- Invest in pediatric formulations strategically: For manufacturers, prioritize WHO prequalification of child-friendly presentations; for buyers, forecast pediatric uptake and align procurement volumes accordingly.

- Use tender design to incentivise resilience: Structure procurement to reward supplier prequalification status, demonstrated surge capacity, and local regulatory approvals — not price alone.

- Align with donors early: Map donor planning cycles and co-develop pilot deployments (e.g., preschool roll-outs) to secure multi-year funding commitments.

- Embed scenario-based financial modelling: Stress-test business cases against supply shocks, currency swings, and donor-budget retractions to set defensible production and pricing strategies.

- Pursue targeted partnerships: Consider co-manufacturing, tolling agreements, or equity stakes to secure API and finished‑product capacity at scale.

- Prioritise WHO prequalification actions: For any new product or reformulation, accelerating prequalification materially alters price parity and tender eligibility in endemic countries.

Closing — why read the full PW report now

2026 is a hinge year: the combination of pediatric product rollout, concentrated supply, and renewed programmatic push towards elimination means that procurement, manufacturing and policy decisions taken this year will shape the next funding and access cycle. Our full report not only contains the granular forecasts and segment tables (by region, drug type, distribution channel and end-user) but also provides the practical contract templates, supplier scorecards, tender intelligence, and scenario models that teams need to convert insight into executable plans.

For executives and teams preparing bids, supply strategies, or investment memoranda, the report functions as an operational blueprint: it tells you where to underwrite capacity, where to hedge, which partnerships to prioritise, and how to set realistic timelines for regulatory and prequalification milestones. To access the complete dataset, granular splits, and the decision-ready annexes, please consult the full PW Consulting Drugs for Schistosomiasis Market report.

If you would like a tailored briefing that translates our findings into a 90‑day action plan for your organisation, contact PW Consulting’s NTD practice — we will map the dataset to your procurement, manufacturing, and partnership priorities and produce a focused playbook calibrated for 2026 execution.

For detailed analysis of this topic, please visit the official page:Drugs for Schistosomiasis Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com