Alpha-2-Antiplasmin Market Overview: Key Drivers and Challenges

Networking |

2026-02-23 08:27:27

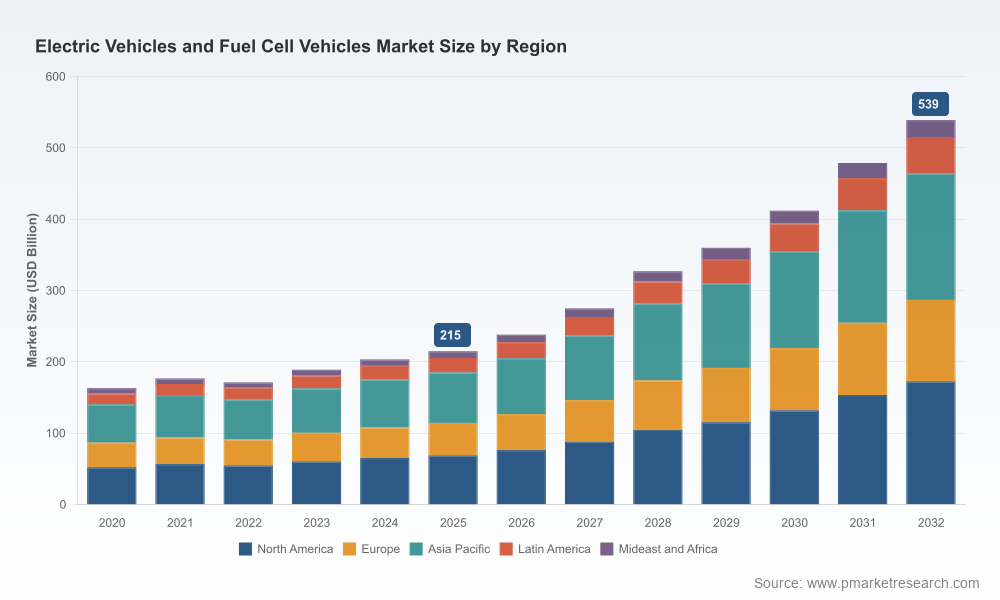

As governments tighten emissions targets and capital allocators recalibrate transport portfolios, corporate leaders face a compressed window in 2026 to convert strategy into durable advantage across the electric vehicle (EV) and fuel cell vehicle (FCV) ecosystem. PW Consulting’s latest market study—anchored on a 2025 base year and a 2026–2032 forecast horizon—translates complex macro trends into operational choices. The market we modelled expanded from the low‑hundreds of billions (USD) in 2020 to approximately USD 215.0 Billion in 2025, and our conservative projection takes the industry to roughly USD 539.0 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 14.06% over the forecast period. That trajectory creates both scale opportunities and nonlinear risks for vehicle OEMs, suppliers, energy incumbents, fleet operators and new entrants.

Electric Vehicles and Fuel Cell Vehicles Market

Timing of scale: The market is accelerating. Between 2026 and early 2030 we expect structural inflection points—driven by policy, raw‑material learning curves and commercial hydrogen economics—that will determine which technologies and supply models capture the bulk of value.

Electric Vehicles and Fuel Cell Vehicles Market

Capital allocation: A sustained mid‑teens CAGR implies large addressable pools, but the path to profitable unit economics is differentiated across vehicle types and use cases. 2026 is a pivotal year to finalize capital commitments or pivot to strategic partnerships.

Electric Vehicles and Fuel Cell Vehicles Market

Portfolio design: With BEV adoption at record levels globally and incremental interest in hydrogen mobility for heavy‑duty and long‑range use cases, firms must choose between vertical integration, modular OEM partnerships, or pure‑play component positions.

The headline numbers are instructive: recovery since 2020 has given way to an expansion phase where revenue pools broaden rapidly. This growth is not homogeneous—regulatory pressure in major markets, record EV penetration in 2025 (exceeding 20 million units globally), and targeted technological cost reductions are the primary tailwinds. At the same time, short‑term adoption noise—such as localized registration declines for specific fuel cell programs—reveals that infrastructure and total cost of ownership (TCO) realities matter materially for buyers.

Three structural drivers will dominate 2026 decisions:

Policy and regulation: Stricter CO2 standards and zero‑emission vehicle mandates are compressing OEM product timelines and forcing pricing actions that change competitive dynamics.

Cost curves and scale effects: Public targets for fuel cell system costs and hydrogen production costs are acting as explicit inflection points for fleet buyers and logistics providers evaluating long‑distance duty cycles.

Customer economics: Fleet electrification economics for urban delivery and short‑haul transit are approaching parity faster than for heavy‑duty long‑haul, generating tactical winners and losers.

The industry remains fragmented: concentration metrics indicate that even the leading triad of players does not dominate the market, leaving room for new entrants, technology specialists, and regional champions. Our competitive analysis synthesizes recent product launches, production starts and partnerships to map where capability is being built.

Toyota Motor Corporation: Continues to advance fuel cell system maturity with a third‑generation product positioned for passenger, commercial and heavy‑duty applications. Toyota’s strategy is clear—build durable, scalable hardware and leverage broad geographic launches to accelerate learning curves.

Hyundai Motor Company: Investing in both passenger and heavy‑duty hydrogen platforms, Hyundai’s roadmap (including updated Nexo and commercial applications) signals a dual‑track approach that hedges BEV competition while owning hydrogen truck and bus niches.

Honda Motor Co., Ltd.: With production starts in new regions and plug‑in FCEV models in market, Honda is pursuing manufacturing footprint diversification and targeted product differentiation to address regional demand and regulatory environments.

BMW AG: Strategic collaborations and announced series production plans reflect a cautious route into hydrogen, using partnerships to de‑risk manufacturing complexity while preserving technology optionality.

Specialists (e.g., advanced catalyst and component suppliers): Companies producing next‑generation catalysts and balance‑of‑plant hardware are becoming leverage points in OEM sourcing strategies—where technology ownership can translate into outsized margin and bargaining power.

Recent developments—product launches, U.S. production starts, portfolio expansions for hydrogen subsystem suppliers—converge on an industry moving from demonstration to commercial roll‑out. However, these announcements must be read in context: product availability does not equal immediate demand, and regional infrastructure parity remains uneven.

Actionable procurement and manufacturing strategies should focus on three levers:

Raw materials and component modularity: Prioritize supplier agreements that allow step changes in cost through material substitution and modular architectures. Public targets—such as reducing fuel cell system cost per kilowatt and hydrogen production cost per kilogram—should be used as scenario anchor points in investment cases.

Localised manufacturing vs. global sourcing: The interplay of regulation, trade policy and logistics means many OEMs will choose a geo‑flexible production strategy. The optimal blend will depend on product family and duty cycle economics.

Service and uptime economics: For commercial and heavy‑duty customers, uptime and refueling/recharging network density are as decisive as purchase price—making aftermarket service models a defensible source of margin.

Regulatory tightening—especially in major economic blocs—will force product portfolios to change. Meanwhile, macro adoption indicators (record EV sales in 2025) juxtaposed with localized FCV registration shifts highlight where momentum exists and where infrastructure or customer familiarity must catch up. Governments’ hydrogen and fuel cell cost targets are not just policy statements; they are investment signals that will shape where public incentives flow and which corridors achieve commercial‑scale hydrogen economies first.

Leaders who move decisively in 2026 should adopt a multi‑track approach calibrated to their core strengths. The following recommendations are operationally specific and time‑sensitive:

Commit to portfolio clarity: Decide which vehicle families you will own, which you will co‑develop, and which you will exit. Clarity reduces dilution of R&D and capex.

Derisk through partnerships: Execute binding offtake, co‑investment or technology licensing agreements with suppliers and energy providers to secure price and volume commitments.

Build modular manufacturing cells: Prioritize plug‑and‑play production lines that can switch between battery and fuel cell stacks where demand is uncertain.

Invest in TCO analytics: Deploy customer‑facing TCO tools that quantify break‑evens for fleets across regional energy prices, incentives and utilization patterns.

Define exit ramps: For investments that do not hit predefined learning or price thresholds within 24–36 months, prepare structured exit or pivot options to protect cash flow.

We recommend three scenario lenses for 2026 planning—Policy‑Driven Acceleration, Cost‑Driven Adoption, and Infrastructure‑Constrained Plateau. For each, monitor a concise dashboard to trigger pre‑defined strategic moves:

Policy indicators: New or tightened emissions standards, purchase incentives, and procurement mandates for fleets.

Cost indicators: Fuel cell system cost per kW and hydrogen production cost per kg relative to public targets—watch for crossing points that unlock heavy‑duty adoption.

Commercial uptake: Fleet procurement cycles, pilot-to‑scale conversion rates, and extension of service contracts.

Supply chain metrics: Lead times for critical components, supplier concentration, and price volatility indices for key raw materials.

To convert the insights above into executable plans, our full study provides:

Granular market modeling with historical baselines and bottom‑up scenario forecasts across the 2026–2032 period.

Decision frameworks for OEMs, Tier‑1 suppliers and energy companies that translate market scenarios into capex and partnership roadmaps.

Commercial playbooks including go‑to‑market strategies for fleet sales, aftersales service architectures, and pricing templates.

Supply chain maps, technology readiness assessments, and partner risk matrices to prioritize supplier relationships.

Competitive profiles and primary research synopses covering leading OEMs and technology suppliers, linked to recent product launches and production milestones.

Interactive spreadsheet models and KPI dashboards to stress‑test strategic choices under alternative assumptions.

In this overview we expose the strategic shape of the opportunity and the levers that matter in 2026. Deliberately omitted are the detailed segment‑level revenue splits, regional shares and confidential unit‑economics tables that form the actionable core of buy/sell decisions. Those datasets—including the scenario‑by‑scenario breakdowns and downloadable models—are bundled with the full report and accompanying advisory engagement options.

If your 2026 capital plan, product roadmap or M&A pipeline touches on electric or fuel cell mobility, use the next 60 days to stress‑test assumptions: require scenario runs that include the DOE cost targets for fuel cells and hydrogen, validate partner commitments for infrastructure, and build conditionality into your product launch timelines. For teams that prefer to move faster, PW Consulting offers targeted workshops to translate the report’s models into concrete investment memos and implementation roadmaps.

Contact PW Consulting to access the complete dataset, excel models, and a tailored briefing that aligns our findings with your strategic priorities.

For detailed analysis of this topic, please visit the official page:Electric Vehicles and Fuel Cell Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com