How Is Industrial Modernization Supporting the Middle East and Africa Industrial Display Market?

Networking |

2026-07-08 09:25:17

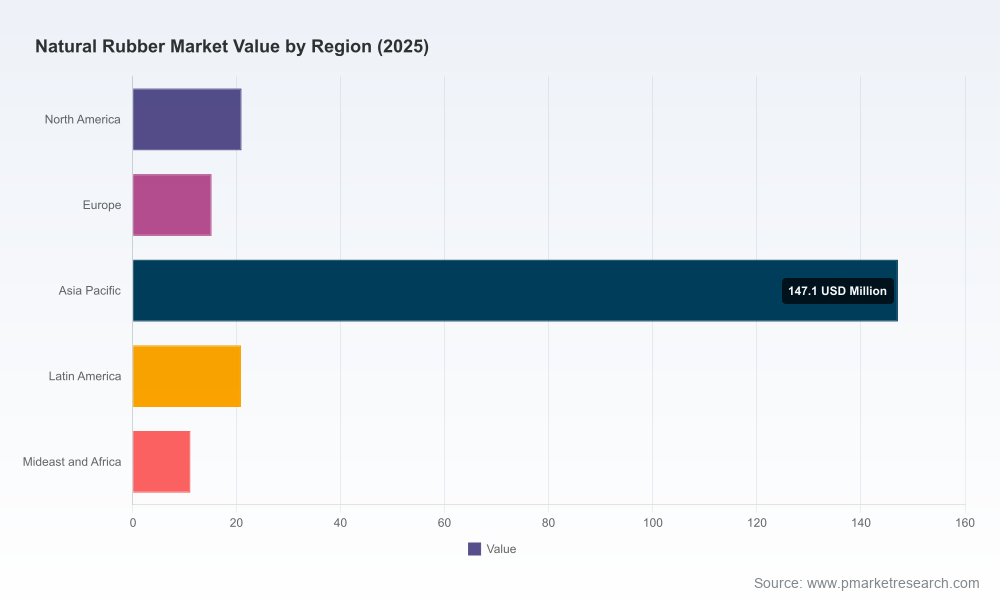

Natural rubber is entering 2026 from a position of measured growth and mounting structural change. Our base-year assessment (2025) places the global market at USD 215.0 Million (revenue basis), having expanded from USD 163.15 Million in 2020. Under the scenarios modeled in our study, the market is projected to grow to USD 344.8 Million by 2032, reflecting an aggregate compound trajectory consistent with a 5.86% CAGR across the 2026–2032 forecast window. This trajectory hides significant short‑term volatility and diverging regional dynamics that will matter for procurement, manufacturing and investment decisions through 2026 and beyond.

Natural Rubber Market

Timing of regulatory compliance: From 30 December 2026 the EU Deforestation Regulation (EUDR) will require proof of no-deforestation and strict plot-level traceability for natural rubber entering the EU market. For large operators this is not a distant compliance exercise; it becomes a binding operational constraint within the 2026 calendar year and will materially affect sourcing, supplier selection and capital allocation decisions.

Natural Rubber Market

Supply-side fragility: Recent production shocks — including recurring flood-related disruptions in Thailand reported to have the potential to remove on the order of magnitude of tens of thousands of tonnes from available supply — underline how weather, logistics and local labour dynamics can rapidly compress availability and raise spot price risk. Our report integrates alternate supply-shock scenarios calibrated to recent events and industry production forecasts.

Natural Rubber Market

Near balance at global scale: Sector forecasts from primary institutions indicate production and consumption are near parity in 2026, with a small but persistent supply-demand gap. That equilibrium amplifies the price and availability sensitivity to discrete events (weather, regulation, large-firm sourcing shifts) — making preparedness and flexible sourcing strategies essential for stable operations.

Consolidation and market power: The sector is concentrated around a limited set of large processors and integrated producers. Competitive moves by these players — from sustainability certification to vertical integration — shape market access and price dynamics for downstream buyers.

Our full Natural Rubber Market study is structured to translate market analysis into operational actions and board-level choices. Key deliverables include:

Robust market sizing and scenarios: a verified historical series (2020–2025), base-year benchmarking (2025) and multiple demand-supply scenarios for 2026–2032 tailored to alternative recovery, climate and policy pathways.

Price and inventory stress-testing: elasticity matrices and hedging implications that allow procurement teams to model the P&L and working capital impacts of spot spikes, supply interruptions and compliance cost pass-throughs.

Regulatory playbook for EUDR and equivalents: a compliance roadmap that translates plot-level traceability requirements into a six‑to‑twelve month operational plan, including data requirements, supplier contracts, audit cadence and likely cost vectors.

Supplier risk scoring and sourcing options: a validated framework for assessing counterparty resilience (production footprint, processing flexibility, certification readiness) and practical sourcing pathways — from near-shoring and blended sourcing to strategic stockpiling.

Investment and M&A signal matrix: identification of technical and geographic pockets where value accrues for acquirers (capabilities, traceability tech providers, midstream processors), together with recommended diligence checklists.

Smallholder engagement & sustainability levers: operational templates and business models for scaling fair‑trade and sustainable procurement programs that mitigate reputational and supply risks while unlocking preferential offtake.

The natural rubber value chain is shaped by a mix of integrated processors, specialized suppliers and regional champions. Our analysis synthesizes public disclosures, production capacities and strategic orientation to map where each firm is positioned relative to 2026 priorities:

Sri Trang Agro-Industry — As the largest processor by volume, their scale gives them bargaining power and the ability to underwrite compliance investments (traceability systems, diversified drying and storage nodes). For buyers, Sri Trang represents both a stable anchor supplier and a potential chokepoint should they reprioritize customer mix or inventory holdings in response to shocks.

Halcyon Agri — Integration across plantation and processing, combined with an explicit sustainability orientation, makes Halcyon a useful partner for buyers seeking consolidated compliance paths. Their operating model highlights how upstream control can be deployed to accelerate EUDR readiness.

Thuan Loi Rubber and Ngoc Chau Natural Rubber — Vietnam-based capacity and export orientation are strategically important as buyers reassess diversification away from single-country concentration. These firms typify the growth opportunity and operational risk in higher-yield, export-led production models.

Siam Synergy Industrial — Specialists in grades including reclaimed rubber, their portfolio illustrates how downstream buyers can manage input costs by blending grade types, managing quality specifications and pursuing material substitution where application permits.

Across these actors, observable trends include accelerated investment in traceability technologies, diversified logistics footprints to mitigate flood and road-access risk, and selective upstream partnerships to secure feedstock under compliance-ready models.

Flooding in key production zones has elevated the probability of short-term supply reductions; our scenarios quantify the P&L sensitivity to these shocks and propose mitigation ladders for buyers and processors.

The rollout of national and industry sustainable rubber initiatives (for example, government-backed certification and grower support programs) is shifting the cost base of compliant production — a dynamic that will influence long‑run supplier availability and pricing.

Industry partnerships targeting smallholder livelihoods and quality improvement are creating new sourcing pools that may offer lower reputational and compliance risk, albeit with initial onboarding and traceability investment requirements.

Immediate compliance triage: map all EU‑bound product lines and identify suppliers lacking plot-level traceability. For material exposure, implement contractual clauses that accelerate delivery of trace data or establish conditional sourcing alternatives.

Operationalize a two-tier sourcing strategy: secure a compliance‑certified core supply that meets EUDR needs and maintain a flexible satellite sourcing pool to manage price and availability shocks.

Invest in traceability pilots now: prioritise technologies that can be scaled across suppliers (mobile-enabled farmer data capture, GIS-backed chain-of-custody). Early pilots reduce 2026 compliance costs and shorten audit timelines.

Hedge selectively and manage inventories: combine financial hedges with tactical inventory buffers sized to company risk tolerance and working capital constraints; our report includes stress-tested inventory rules calibrated to recent supply events.

Pursue strategic partnerships and M&A selectively: prioritize deals that accelerate traceability, secure captive supply or add processing flexibility rather than those that merely add capacity.

To preserve the report’s commercial value and to follow the “preview” principle, we present high‑level market trajectories, regulatory imperatives and competitive positioning above while omitting granular split tables and segment-by-region/application revenue breakdowns in this briefing. The full report contains the detailed regional and application segmentation, grade-by-grade pricing matrices, and supplier-level benchmarks needed to execute sourcing or M&A transactions with precision.

For procurement chiefs, corporate strategy teams, and private equity sponsors preparing decisions in 2026, our team offers rapid deployment offerings: 48–72 hour supplier compliance triage, eight-week traceability pilot designs, and custom scenario modeling aligned to client hedging and inventory constraints. Our full Natural Rubber Market study is the executable reference for these engagements — combining the public data and primary interviews that underwrite the scenarios summarized above.

Request the full report to access the segmented revenue tables, supplier scorecards and scenario appendices required for transactional decisions.

Commission a tailored 4–6 week readiness assessment if your firm has EU market exposure or sizable upstream contracting commitments due in 2026.

For detailed analysis of this topic, please visit the official page:Natural Rubber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com