Turbo Molecular Pumps Market — Strategic Outlook and 2026 Playbook

Executive preview

The turbomolecular pumps market is transitioning from a component-led industrial niche into a strategic lever for semiconductor, analytical, and research-intensive industries. This briefing summarizes the strategic value of PW Consulting’s full Turbo Molecular Pumps market study for corporate leaders making 2026 investments. It demonstrates the analytical depth and actionable framing you can expect from the complete report while intentionally withholding granular segment tables and split-level figures — the precise segmentation and supplier scorecards are available in the full report on our site.

Turbo Molecular Pumps (Turbomolecular Pumps) Market

Market snapshot and trajectory

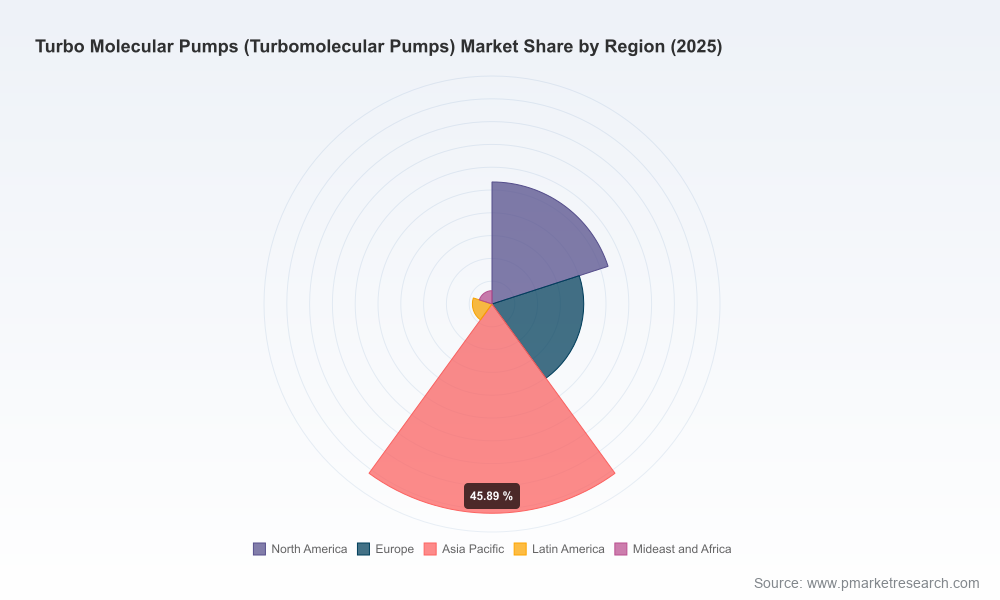

Using 2025 as the base year, this sector exhibits a measured, resilient expansion characterized by an underlying structural demand for higher pumping speeds, lower base pressures, and reduced life-cycle energy intensity. The market grew from roughly USD 1.2 billion in 2020 to about USD 1.69 billion in 2025 (base year). Our forecast through 2032 projects continued growth at a compound annual growth rate (CAGR) of approximately 5.5%, reaching an expected market size in the vicinity of USD 2.46 billion by 2032. These macro indicators point to a market large enough to sustain multiple technology pathways and consolidation dynamics, yet specialized enough that engineering differentiation and after-sales capabilities materially affect competitive advantage.

Turbo Molecular Pumps (Turbomolecular Pumps) Market

Why 2026 is a strategic inflection point

- Demand pull from advanced manufacturing: Accelerated capacity build-outs under public policy initiatives (notably semiconductor and life-science cluster investments) are increasing requirements for high-throughput, ultra-high-vacuum solutions. Buyers are prioritizing pump families that deliver repeatable base pressures and fast pump-down times at scale.

- Energy and net-zero mandates: New regional energy-efficiency directives and net-zero trajectories are reshaping purchasing specifications. OEMs are responding with lower-wattage drives, intelligent standby modes, and operational software to claim energy savings — an important procurement qualifier for public and quasi-public projects.

- Materials and supply-chain stress: Component sourcing risks — especially related to rare-earth materials used in magnetic-levitation designs — are prompting strategic redesigns and dual-sourcing of magnets and high-performance bearing materials. Choices made in 2026 about rotor architecture and supplier contracts will lock in risk profiles for several years.

- Regulatory time horizons: Compliance requirements tied to energy intensity and procurement standards are increasingly multi-year commitments, affecting product design, warranty offerings, and the economics of retrofit vs. replacement strategies.

Technology and product dynamics to watch

The market’s technology landscape remains pluralistic: oil-lubricated mechanical designs continue to serve cost-sensitive industrial applications, magnetically levitated (maglev) pumps gain share for performance-sensitive installations, and hybrid architectures sit between these poles. Key engineering battlegrounds for 2026 decisions include:

Turbo Molecular Pumps (Turbomolecular Pumps) Market

- Energy per throughput: Watt-per-liter performance is now a procurement metric alongside ultimate pressure.

- Materials and endurance: New bearing alloys and Cronidur-type stainless steels are reducing corrosion risk and extending maintenance intervals, changing lifecycle cost assumptions.

- Magnet strategy: Designs that reduce reliance on high-dysprosium content magnets or that allow substitution without performance loss will be favored where rare-earth risks are acute.

- Digitalization: Predictive maintenance, integrated telemetry, and power/efficiency dashboards are becoming table stakes for buyers seeking lower total cost of ownership.

Competitive landscape — practical takeaways

The competitive configuration is moderately concentrated; the top three suppliers account for a meaningful share of the market and the top five consolidate further, indicating a mix of global scale players and specialized regional champions. This concentration underscores two strategic realities: incumbent engineering depth matters, and there is room for differentiated newcomers with compelling cost, service, or niche-application value propositions.

- Edwards Vacuum (Burgess Hill, UK) — Known for broad mechanical and maglev pump series; active in showcasing product families and integrated pumping solutions at trade events. Recent presence at Analytica 2026 signaled continued emphasis on combined product-service solutions for analytical markets.

- Pfeiffer Vacuum (Aßlar, Germany) — Offers a full spectrum of bearing configurations for high and ultra-high vacuum, competing on depth of product architecture and engineering customization.

- Ebara Corporation (Tokyo, Japan) — Focused on maglev offerings with high throughput and strong performance credentials; a play for customers prioritizing durability and high pumping speeds.

- Leybold (Cologne, Germany) — Recent expansion of robust mechanical families underscores its industrial coating and research-market focus; product refreshes in early 2026 emphasize reliability under challenging duty cycles.

- ULVAC (Chigasaki, Japan) — Competes with a mix of desktop and larger maglev/ball-bearing lines, aiming at both lab-scale and manufacturing customers.

- Agilent Technologies (Santa Clara, USA) — Plays to analytical and research applications with a focus on high-vacuum pumping solutions tightly integrated with analytical instruments.

Recent vendor activity — product line expansions and trade-show investments — indicate the market is being actively defended and re-segmented by innovation rather than only by price. For buyers and executives, supplier roadmap visibility and lifecycle service agreements are now as important as headline pump performance.

Regulatory, sourcing and operational risks

- Energy-efficiency regulation: Bids for public-sector projects increasingly require demonstrable efficiency features; vendors without low-wattage or intelligent standby options risk exclusion.

- Net-zero alignment: Multi-year contractual clauses on energy intensity and emissions performance are entering supplier agreements, shifting risk toward OEMs.

- Rare-earth and raw-material supply: Magnet sourcing risk is influencing decisions on maglev designs and encouraging alternative rotor/bearing concepts. Materials such as high-grade stainless steels (e.g., Cronidur-type alloys) are becoming procurement differentiators for longevity.

- Concentration risk in components: Consolidation among critical-component suppliers could create single-point risks unless buyers pursue multi-sourcing or longer-term supply contracts.

How executive teams should use this research in 2026

PW Consulting’s full study is designed to translate market intelligence into immediate actions across product strategy, procurement, and M&A. Strategic uses we recommend for 2026:

- Product roadmapping: Prioritize low-energy architectures and telemetry-enabled control systems for new product releases slated for 2027–2029. Map regulatory timelines to feature delivery to ensure bid-eligibility in major public tenders.

- Procurement and supplier strategy: Lock in dual-source arrangements for magnets and high-performance bearing materials; include materials-replacement clauses to maintain performance under constrained rare-earth supply scenarios.

- Aftermarket and services: Build service networks in regions supported by public funding and semiconductor clusters to monetize uptime guarantees and predictive maintenance.

- M&A and partnerships: Use small, targeted acquisitions to secure niche bearing technologies, digital telematics capabilities, or regional service footprints rather than broad horizontal deals.

- Risk-adjusted capex allocation: Re-evaluate factory automation and testing lab investments to support maglev assembly tolerances and to ensure supply flexibility across bearing and rotor configurations.

What the full PW Consulting report contains (operational highlights)

The complete study delivers practical, transaction-grade outputs to support 2026 strategic choices. Highlights include:

- Time-series market model (2020–2032) with scenario sensitivities and forecasting by technology pathway — fully editable and exportable for internal planning.

- Supplier scorecards and capability matrices that rank engineering depth, global service footprint, product roadmaps, and supply-chain resilience.

- Regulatory and procurement playbooks tailored to public-sector tenders and major private OEM RFPs, including specification checklists and clauses to manage energy-intensity obligations.

- Technology assessment dossiers that compare oil-lubricated, maglev, and hybrid architectures across lifecycle cost, energy, and maintainability metrics.

- M&A and partnership screening with valuation shorthand and integration risk flags for target segments (IP, manufacturing, service networks).

- Practical annexes: buyer’s RFP templates, capex vs. opex decision matrix, and a 24-month implementation roadmap for procurement, engineering, and aftermarket teams.

Note: detailed split tables by region, product, and application are part of the paid dataset and are intentionally excluded from this preview. These granular segmentations drive the supplier scores and scenario outputs described above and are required for transaction-level decisions.

Next steps for leaders in 2026

For corporate strategists, procurement leaders, and product heads, 2026 is the window to secure design wins, lock in resilient supply agreements, and align new product launches to tightening energy regulations. The choices you make now about bearing architectures, energy optimization, and supplier diversification will determine competitiveness well into the 2030s.

PW Consulting’s Turbo Molecular Pumps study translates the market’s macro growth trajectory — a steady expansion at a mid-single-digit CAGR through 2032 — into practical, executable strategies. To obtain the full segmentation, downloadable data models, supplier scorecards, and the procurement playbook referenced above, consult the full report on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Turbo Molecular Pumps (Turbomolecular Pumps) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com