1,3-Butylene Glycol (CAS 107-88-0): Strategic Market Briefing for 2026 Decision-Makers

As companies prepare capital allocation, sourcing strategies, and product roadmaps for 2026, the 1,3-butylene glycol market presents a distinctive combination of steady growth, concentrated supply, and regulatoryly driven product differentiation. PW Consulting’s new market study — grounded in granular primary research and forward-looking scenario modelling — synthesizes the signals commercial teams and executive leadership need to convert market visibility into competitive advantage. The summary below highlights the strategic implications of our findings while reserving the granular segment and regional matrices for the full report.

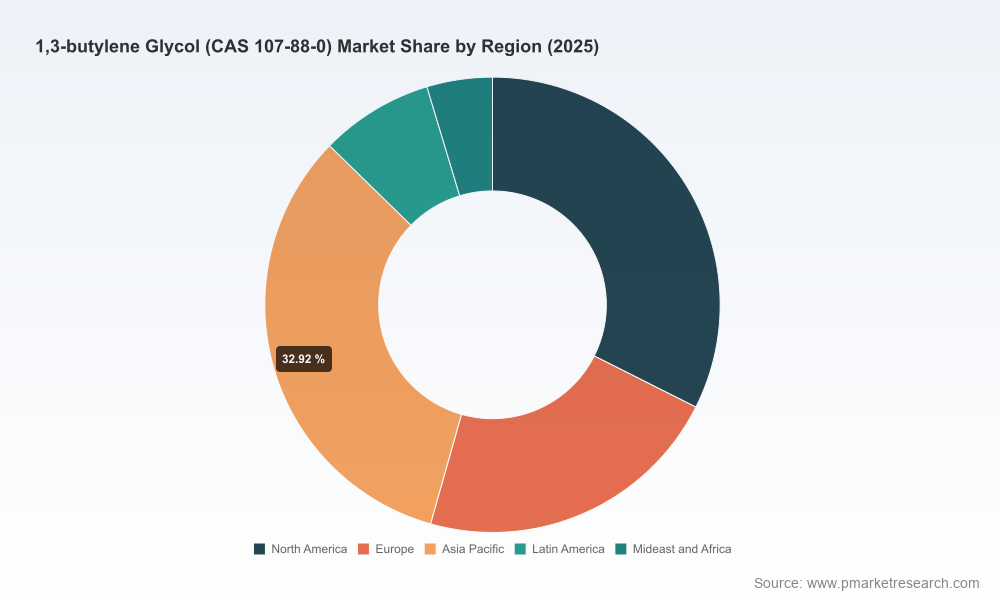

1,3-butylene Glycol (CAS 107-88-0) Market

Market Snapshot: Where the Market Stands and Where It’s Headed

Between 2020 and 2025 the global 1,3-butylene glycol market expanded from roughly USD 163.2 Million to USD 212.5 Million, reflecting recovery dynamics, shifting end-use demand, and evolving raw-material economics. The forecast period (2026–2032) shows continued expansion, with the market tracking to approximately USD 321.7 Million by 2032 at a compound annual growth rate (CAGR) of 5.9%.

1,3-butylene Glycol (CAS 107-88-0) Market

This steady, mid-single-digit CAGR masks structural asymmetries: demand is increasingly influenced by sustainability credentials, certification regimes in personal care and food, and the availability and price volatility of feedstocks—bio-based sugar feeds versus petrochemical derivatives. From a 2026 planning perspective, these macro numbers are important because they frame the scale of near-term investment and the horizon over which returns from capacity expansions, certification costs, and supply chain reconfigurations will accrue.

1,3-butylene Glycol (CAS 107-88-0) Market

Why This Study Matters for 2026 Decisions

- Capital and capacity decisions: With predictable market growth, leaders must decide whether to pursue incremental debottlenecking, brownfield expansions, or greenfield builds. Our modelling identifies the breakeven thresholds under multiple pricing, raw material, and utilization scenarios.

- Product strategy and certification: Demand is bifurcating between conventional and certified bio-derived grades. COSMOS, NATRUE, and comparable label expectations materially affect formulation choices and go-to-market claims — and, by extension, supplier selection and product premiums.

- Procurement and supplier risk: High market concentration and a limited set of qualified suppliers mean procurement strategies must move beyond transactional buying toward strategic partnerships, long-term contracts, or backward-integration evaluations.

- M&A and partnership scouting: The economics favor bolt-on acquisitions for filling capability gaps (bio-processing, purification, certification ownership) rather than large-scale greenfield investments in certain geographies.

Competitive Landscape: What the Leading Players Signal

The 1,3-butylene glycol supplier base is compact and increasingly specialized. Market concentration metrics indicate that the top three suppliers control a material majority of the market, and the top five approach near-total dominance — a structural feature with direct implications for pricing dynamics, lead times, and technology diffusion.

- OXEA GmbH (Oberhausen, Germany): A premium supplier across industrial and cosmetic grades, OXEA’s positioning emphasizes quality and global logistics capabilities. Its European base, combined with export reach, makes it a key counterparty for multinational formulators seeking consistent, certified inputs.

- Daicel Corporation (Osaka, Japan): With large-scale capacity and a strategic focus on sustainable applications, Daicel’s recent business-plan review signals close scrutiny of portfolio returns and potential redeployments of assets. For buyers, Daicel represents scale, technological know-how, and potential consolidation activity.

- Godavari Biorefineries Ltd. (Hyderabad, India): A leading bio-derived producer, Godavari executed debottlenecking to materially raise output and achieved full utilization. This trajectory underscores the commercial viability of bio-based 1,3-BG and the competitive pressure it places on synthetic producers, particularly in formulations where natural-origin claims matter.

- Penta Manufacturing Company & Rita Corporation (United States): Both firms provide high-purity grades suitable for pharmaceutical and food applications, serving regulated markets with stringent quality management systems and distribution networks tailored to small-batch, high-value demand.

- MMP Inc., Shanghai Jinjin Industry, KH Neochem, Whyte Chemicals: These players collectively serve regional and global channels — from coatings and plastics intermediates to personal care and industrial formulations. Their roles spotlight the hierarchy within the supply chain: multinational anchors, regional specialists, and distributors who smooth access to smaller end-users.

Strategic takeaways from the competitive set:

- High concentration (top-three/top-five dominance) confers pricing stability for suppliers and potential margin compression for buyers who cannot secure long-term contracts.

- Bio-derived entrants (capacity increases and certification gains) are rapidly changing the value proposition for personal care and food customers — compelling incumbents to either invest in bio routes or differentiate on logistics, quality, or vertical integration.

- Recent corporate moves — from capacity debottlenecking to business-plan reviews — suggest a period of portfolio fine-tuning rather than aggressive greenfield expansion among tier-one producers.

Market Dynamics, Risks, and Regulatory Drivers

Three dynamics dominate strategic risk assessments for 2026 planning:

- Feedstock volatility and dual sourcing: Bio-based production depends on agricultural inputs (e.g., sugarcane fermentation), while synthetic routes rely on petrochemical intermediates with periodic supply shocks. Procurement strategies that combine dual-sourcing, hedging, and regional buffer inventories reduce exposure.

- Certification and label-driven demand: Certification regimes like COSMOS and NATRUE create a premium segment for bio-derived 1,3-BG. Companies that obtain and maintain certified supply chains capture formulation share among premium personal care and natural-branded food products.

- Compliance costs across trade regimes: Regulatory frameworks (e.g., European REACH and U.S. TSCA) raise cross-border registration and approval costs, altering the economics of exporting from lower-cost regions and favoring local production or registered imports.

Additionally, programs such as the U.S. EPA’s Safer Choice labeling can be leveraged in marketing and product development for formulators emphasizing safety and sustainability. Anticipating and budgeting for these compliance and certification efforts should be a standard part of 2026 operating plans.

What the Full PW Consulting Report Delivers (Operationally Actionable)

The study is designed to be operational from day one. Highlights of deliverables include:

- Validated market sizing (base year 2025) and bottom-up forecasts (2026–2032) with scenario toggles for feedstock price shocks, certification adoption rates, and utilization shifts.

- Comprehensive competitor dossiers and supplier scorecards (quality systems, capacity, lead times, certification status, and financial health).

- Supply-chain heat maps and risk matrices identifying single-source dependencies, logistics pinch points, and regulatory friction zones.

- Pricing and margin models by grade and route (bio vs. synthetic) with thresholds for profitable capacity additions and contract pricing strategies.

- Go-to-market playbooks for formulators and chemical distributors: formulation switch timelines, certification roadmaps, and marketing claim strategies.

- M&A and partnership pipeline: shortlists of tuck-in targets and JV structures to secure feedstock or downstream formulation access, including indicative valuation ranges and integration checklists.

- Five strategic scenarios and recommended tactical responses for each, plus an executive dashboard to track lead indicators in 2026.

Because this briefing adheres to the “trailer” principle, granular regional, application, and type-level splits — including the numerical breakdowns and interactive model files that drive our recommendations — are available exclusively in the full report and interactive datasets.

Practical Recommendations for 2026

- Lock in strategic volumes with tier-one suppliers: Negotiate multi-year contracts with flexible volume clauses to protect against spot-price spikes while preserving optionality for certified bio-sourced volumes.

- Prioritize certification where it delivers premium: For personal care and natural-branded food lines, invest in certified bio-sourced supply or secure supply through branded suppliers to preserve product claims and margins.

- Assess debottlenecking before greenfield: Our economics show brownfield capacity increases and process optimizations often yield superior IRR versus greenfield builds under base-case growth trajectories.

- Embed regulatory foresight into sourcing: Factor REACH/TSCA registration timelines and costs into cross-border sourcing decisions to avoid downstream market entry delays.

- Monitor near-term M&A and partnership signals: Suppliers’ corporate moves are likely to drive short-term availability constraints or consolidation — maintain active intelligence on target companies and engage early where strategic fit exists.

Next Steps and How to Access the Full Intelligence

The full PW Consulting 1,3-Butylene Glycol market study contains the quantitative tables, regional and application splits, supplier-level capacity maps, and an interactive forecast model that underpin the strategic actions summarized here. For commercial teams, R&D heads, and corporate development officers preparing 2026 budgets, that granular intelligence converts directional insights into executable programs.

Contact PW Consulting to request the complete report package, licensing for the interactive model, or a bespoke 90–120 minute strategy workshop where our analysts will map the study’s findings onto your specific portfolio and risk profile. The full dataset is required to validate the precise price, volume, and margin thresholds that will determine optimal investment timing — and that is intentionally withheld from this public briefing to preserve the strategic value of the core deliverables.

PW Consulting’s analysis is pragmatic, actionable, and designed to help senior teams make confident 2026 commitments in a market defined by sustainable sourcing shifts, regulatory complexity, and supplier concentration. Use the macro view here to orient strategy, and consult the full study to operationalize it.

For detailed analysis of this topic, please visit the official page:1,3-butylene Glycol (CAS 107-88-0) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com