Garage Body Shop Equipment Market: Trends, Forecast, and Competitive Landscape 2025 –2032

Health |

2026-06-29 06:21:38

As companies prepare budgets, sourcing strategies, and product roadmaps for 2026, an informed, forward-looking view of the wear plate market is no longer optional — it is mission-critical. PW Consulting’s forthcoming Wear Plate Market study synthesizes seven years of historical performance and a seven-year forecast to deliver an actionable line of sight on growth trajectory, competitive structure, regulatory exposures, and pockets of opportunity. This preview highlights the study’s strategic value without disclosing the granular segment tables reserved for subscribers and licensed clients.

Wear Plate Market

Structural growth: The market has demonstrated steady expansion through 2020–2025 and is modeled to continue growing at a compound annual growth rate (CAGR) of 6.7% over the forecast window beginning 2026. This steady upward trajectory reflects durable demand from heavy industries subject to abrasive wear and impact.

Wear Plate Market

Scale and trajectory: Using 2025 as the analytical baseline, the market’s size and projected 2032 scale were calculated to inform capital allocation, production planning, and M&A assessment over multi-year investment horizons.

Wear Plate Market

Competitive context: Market concentration is low relative to many industrial-materials markets — the top-three and top-five supplier shares indicate a fragmentary vendor landscape, creating both risk for buyers (inconsistent standards, quality variance) and opportunity for scale-seeking consolidators.

Procurement and supplier risk: With persistent growth and fragmented supply, procurement leaders should prioritize strategic supplier segmentation in 2026 — allocating spend across tiered partners while securing options for rapid capacity scaling during cyclical upswings.

CapEx and plant planning: Manufacturers and OEMs must reconcile longer-term demand visibility with near-term plant investments. Our forecast horizon supports prioritized investments in modular hardfacing capacity and automation that reduce unit labor content and improve repeatability.

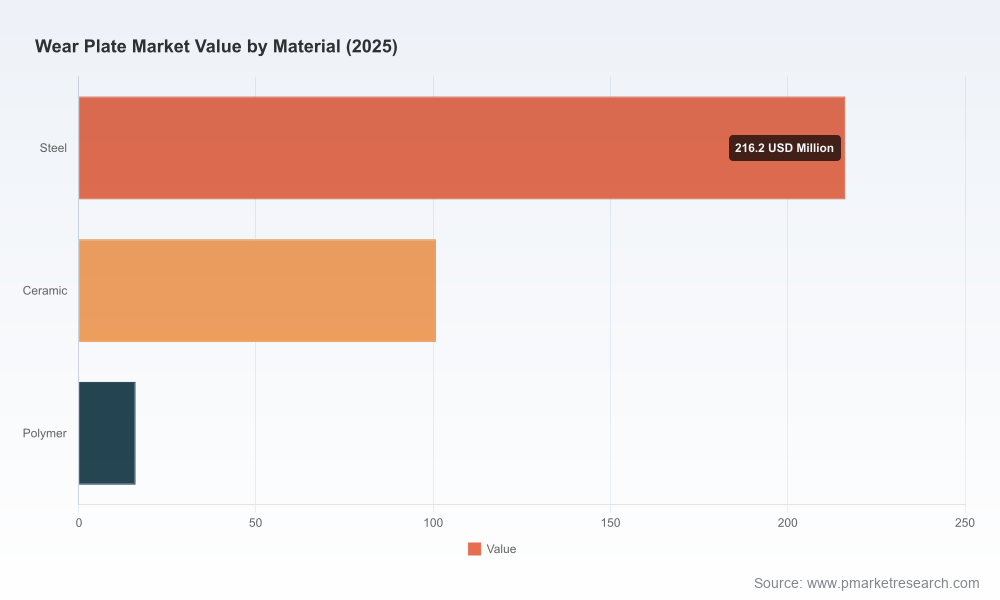

Product and material strategy: The market’s material mix requires a differentiated product strategy — balancing commodity abrasion steels with higher-margin engineered overlays and advanced ceramic/polymer inserts. R&D roadmaps should be sequenced to capture share in higher-growth, technically differentiated subsegments.

Regulatory alignment: The EU Carbon Border Adjustment Mechanism (CBAM) is scheduled to take effect in 2026. Firms supplying into EU value chains will need to quantify embedded carbon and determine cost-to-serve changes, reprice accordingly, or reconfigure sourcing to lower-carbon suppliers.

Robust market sizing and outlook: Historical performance (multi-year) and a detailed forecast through 2032, with scenario variants for macroeconomic shock and raw-material price volatility.

Segment-level intelligence: Multi-dimensional segmentation (by material type, application verticals, and geography) with demand drivers and margin profiles. (Segment tables and per-unit price decks are accessible in the licensed report.)

Price and cost analytics: A deconstructed view of feedstock cost drivers, processing-cost curves, and margin sensitivity to key inputs — essential for pricing strategy and hedging decisions.

Supply chain mapping: Capacity inventories, lead-time analysis, logistics and tariff exposure, and supplier concentration risk heatmaps designed for procurement playbooks.

Competitive benchmarking and capability matrices: Product capabilities, process technologies, service offerings, and channel strategies across incumbent and emerging players.

M&A and partnership playbook: Target heatmaps for bolt-on acquisitions, partnership archetypes, integration synergies, and valuation multiples observed in the sector.

Regulatory and ESG scenarios: Quantified impacts of carbon pricing, trade measures, and product stewardship requirements; pathways to de-risk EU-facing supply chains under CBAM.

Implementation tools: Executive dashboards, commercial KPIs, and a decision-tree toolkit to operationalize the study’s findings in procurement, sales and manufacturing functions.

The market is characterized by a set of specialized manufacturers and regional players that combine metallurgical know-how with application-focused service. Key firms profiled in the study include established OEM-suppliers and overlay specialists based in North America and Asia. Each brings different strengths to bear: deep hardfacing expertise, custom-engineering services, or cost-efficient scale production. Representative examples include:

Wear Plate USA (North Carolina, United States) — Known for custom-engineered wear plates and hardfacing solutions tailored to mining and heavy-equipment applications. Their emphasis on engineered liners and abrasion-resistant components positions them well with OEMs requiring bespoke lifecycle improvement.

ASGCO Manufacturing, Inc. (Allentown, Pennsylvania, United States) — A recognized name in Chromium Carbide Overlay (CCO) and ceramic systems for conveyor and chute protection. Their productization strategy and aftermarket service network are core competitive advantages.

JADCO Manufacturing, Inc. (Harmony, Pennsylvania, United States) — An integrated producer of Chrome Carbide Overlay plates and abrasion-resistant steels; recent product introductions emphasize thinner CCO applications to extend service life in high-damage equipment.

Halden (China) and Tianjin Leigong (Tianjin, China) — Represent fast-following producers with cost-competitive abrasion-resistant steels and customizable hardfacing solutions for regional and export markets.

Metco Joining & Cladding (Westbury, New York, United States) — A specialist in hardfacing alloys and welding overlays, catering to mining and industrial customers requiring application-specific alloying and deposition expertise.

The study’s company profiles include capability matrices, channel footprints, recent product development events, and strategic moves. Recent industry developments captured in the analysis — such as JADCO’s thin CCO launch and updated product catalogs from other suppliers — point to intensified product innovation aimed at delivering longer wear life and lower life-cycle costs.

For manufacturers and OEMs: Prioritize dual-sourcing strategies that hedge carbon exposure and supply disruption. Invest in modular overlay lines and robotic deposition to reduce process variability and lower long-term unit costs.

For distributors and service providers: Differentiate through engineering-led service agreements and condition-based replacement programs that convert commodity buyers into annuity customers.

For private equity and corporate development teams: Target tuck-in acquisitions that add customer intimacy, regional service hubs, or in-house cladding capabilities. Fragmentation creates multiple arbitrage opportunities for roll-up strategies.

For procurement leaders serving EU customers: Begin implementation of CBAM-aligned carbon accounting and supplier audits in 2026; consider nearshoring or contracting with certified low-carbon producers to avoid tariff and competitiveness impacts.

For R&D and product teams: Accelerate work on hybrid solutions that combine advanced steel chemistry with ceramic/polymer inserts to extend service life while reducing part weight — a key selling point for equipment manufacturers focused on fuel and energy savings.

Raw material volatility: Sharp swings in alloying metals or scrap prices can meaningfully compress supplier margins and recalibrate customer total cost of ownership analyses.

Regulatory shocks: Faster-than-expected expansion of carbon tariffs or new product regulations could trigger supplier reconfiguration and regional reshoring.

Technological disruption: Breakthroughs in low-cost ceramic manufacturing or wear-resistant polymer composites could change value-capture patterns across the supply chain.

Macroeconomic cycles: Downturns in end-use industries such as mining and construction would lower near-term demand and elongate working capital cycles for manufacturers.

Our full Wear Plate Market report provides the granular segment tables, regional demand splits, and unit-price decks needed to model specific procurement or investment scenarios. For executives who need rapid decision support in 2026, PW Consulting offers custom workshops, supplier stress-testing, and M&A target screening informed by the study’s dataset and proprietary field interviews.

We deliberately limit this preview to strategic themes and macro findings. The full intelligence package contains the detailed segment economics, company-by-company revenue estimates, and downloadable datasets that commercial teams and dealmakers rely on to operationalize plans.

Download the executive summary and sample datasets to validate assumptions against your internal models.

Schedule a briefing with PW Consulting analysts to review scenario outcomes tailored to your geographic footprint and product mix.

Commission a fast-track strategic audit to convert the market outlook into a 90-day action plan aligned to your 2026 priorities.

In a market growing at a mid-single-digit CAGR with entrenched technical requirements and emerging regulatory constraints, the winners in 2026 will be those who combine manufacturing discipline, carbon-aware supply chains, and service-led commercial models. PW Consulting’s Wear Plate Market study equips leaders with the lens and toolkit to make those choices with confidence; the granular data and executable playbooks are available in the full report.

For detailed analysis of this topic, please visit the official page:Wear Plate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com