PID Sensors and Detectors Market: Strategic Primer for 2026 Decision‑Makers

Executive summary

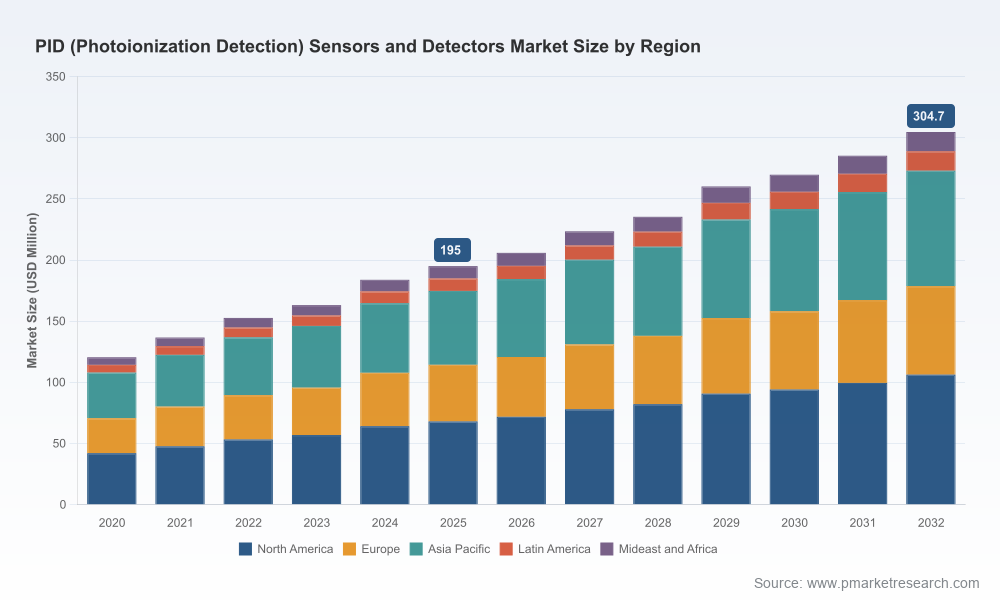

The Photoionization Detection (PID) sensors and detectors market has moved from a specialist niche into a strategic component of industrial safety, environmental monitoring, and process control portfolios. Our PW Consulting PID Sensors and Detectors Market study — with a 2025 base year and projections through 2032 — shows sustained expansion: the market grew materially during 2020–2025 and is forecast to continue expanding at a compound annual growth rate (CAGR) of 6.5% over the 2026–2032 period. By 2025 the global market sits at roughly USD 195 Million (Million USD unit), and our baseline projection points toward a materially larger market by the end of the forecast horizon.

PID (Photoionization Detection) Sensors and Detectors Market

For leadership teams planning budgets, R&D allocations, M&A pipelines, or go‑to‑market priorities in 2026, the question is not whether to allocate resources to PID technology — it is where and how to allocate them to capture the growing value pool without overexposing the business to technology, regulatory, or supply‑chain risk. This primer highlights the strategic value of our full report and the immediate implications we expect to drive executive decisions next year.

PID (Photoionization Detection) Sensors and Detectors Market

Why this study matters for 2026 strategic decisions

- Clear growth runway: An above‑average CAGR over the forecast window supports investment into product development, sensor integration strategies, and aftermarket services.

- Regulatory and standards momentum: VOC exposure limits, regional chemical control regimes, and laboratory accreditation demands are rapidly reshaping procurement specifications and product certification needs.

- Technology inflection points: PPB‑level sensitivity, lamp life improvements, and ultra‑low power electronics are changing product differentiation and total cost of ownership calculations for portable, handheld and fixed systems.

- Concentration and competitive dynamics: The market is neither atomized nor monopolized — the top tiers control meaningful share while mid‑market firms continue to innovate — creating an active environment for partnerships, selective M&A, and OEM supply arrangements.

What the full report delivers (practical contents)

PW Consulting’s report is built as an operational playbook for executives. Key deliverables include:

PID (Photoionization Detection) Sensors and Detectors Market

- Market sizing and trend analysis: A consistent historical data series (2020–2025) and detailed scenario‑based forecasts (2026–2032) with sensitivity testing around regulatory tightening and technology adoption rates.

- Market structure and concentration assessment: CR3 and CR5 analysis, channel mapping, and an evaluation of barrier-to-entry elements including lamp manufacturing, proprietary calibration methods, and certification capabilities.

- Vendor benchmarking: Comparative profiles covering product families, technical differentiators (e.g., sensor sensitivity, lamp life, repeatability), manufacturing scale, and commercial models for the industry’s core players.

- Regulatory and standards matrix: A cross‑jurisdictional mapping of VOC exposure limits, REACH/CLP implications, ISO 17025 calibration expectations, and their impact on product certification roadmaps.

- Go‑to‑market and commercial playbooks: OEM selection criteria, procurement templates, pricing and warranty strategies, and service bundle models for maximizing lifetime revenue.

- Risk and resilience analysis: Supply chain choke points, critical component sourcing, and mitigation roadmaps including dual‑sourcing and lamp lifecycle planning.

- Financial and investment tools: Lumpy CapEx/Opex models, ROI calculators for product launches, and M&A valuation guidance aligned to growth scenarios.

Competitive landscape — strategic read on core players

Our qualitative and quantitative analysis of incumbent and emerging firms yields clear positioning implications for decision‑makers evaluating partners, acquisition targets, or competitive threats.

- ION Science Ltd (Fowlmere, UK) — As the longstanding leader in PID technology, ION Science combines scale with brand recognition and a broad product roster. Their recent launch of the ION SENSE brand and the ARA‑X4 detector signals a twofold strategy: defend core OEM sensor revenues while migrating into higher‑margin detector solutions aimed at compliance and field monitoring. Strategic implication: incumbency gives ION Science pricing power and OEM pull‑through; rivals and potential partners should factor their distribution reach when structuring deals.

- Alphasense (Chorleywood, UK) — Alphasense’s PIDX range emphasizes sensor‑to‑sensor repeatability and lamp life improvements. This product positioning targets customers that prioritize low calibration overhead and predictable lifecycle costs. Strategic implication: product repeatability reduces TCO for large fleets and strengthens the case for volume OEM contracts.

- AMETEK MOCON (Brooklyn Park, MN, USA) — With iterative product introductions such as the piD‑TECH eV‑NXT family, AMETEK MOCON is leveraging industrial safety credentials to capture OEM and integrator demand for ruggedized PID modules. Strategic implication: industrial incumbency and product breadth make AMETEK a natural partner for system integrators and for end‑users focused on industrial hygiene programs.

- PID Analyzers, LLC / HNU (Sandwich, MA, USA) — Focused on application‑specific analyzers for air, water, and process control, HNU occupies a role between sensor suppliers and full solution providers. Strategic implication: convergence of sensor and analytics stacks opens opportunities for service‑led differentiation and subscription models.

- RKI Instruments (Hayward, CA, USA) & WatchGas (UK) — Both firms demonstrate how multi‑gas platforms and instrument ergonomics expand the addressable market for PID technology. By embedding PID capabilities into portable multi‑gas detectors and monitors, these vendors broaden adoption among first responders and plant safety teams. Strategic implication: partnerships with multi‑gas OEMs accelerate market diffusion, but demand product interoperability and consistent calibration practices.

Recent developments to watch (implications for 2026)

- Product launches from AMETEK MOCON and Alphasense during 2024–2025 underscore intensifying competition on accuracy, lamp life, and replacement‑friendly designs.

- ION Science’s brand repositioning and product introductions reflect a push to own both sensor and detector value chains — a trend that could compress margins for pure‑play sensor suppliers unless they secure strong OEM agreements or proprietary advantages.

- Regulatory pressures and lab accreditation (ISO 17025) are creating an addressable services market for calibration and traceable validation, presenting a recurring revenue opportunity for firms that can monetize calibration chains and lab services.

Technology, standards, and infrastructure dynamics

The market is being reshaped by four interlocking vectors:

- Regulation: Tighter VOC exposure limits and chemical classification regimes push end‑users to adopt higher‑sensitivity monitoring and certified measurement procedures.

- Standards & validation: ISO 17025 accreditation requirements influence how vendors design calibration programs and aftermarket service offerings.

- Technical innovation: PPB‑level sensitivity coupled with ultra‑low power electronics is enabling extended battery life for portable and handheld instruments, changing customer acceptance thresholds.

- Infrastructure integration: Remote environmental monitoring in heavy industries is integrating PID sensors into SCADA and IoT platforms for plume tracking and compliance reporting — opening new software and analytics monetization paths.

Practical 2026 recommendations — where to act

- Prioritize sensor repeatability and lamp life in R&D roadmaps. These attributes reduce lifecycle costs and are decisive in OEM selection processes.

- Invest in accredited calibration capabilities or strategic partnerships. Offering ISO 17025‑compliant services will create defensible recurring revenues and lower customer switching risk.

- Develop modular product families for easy field replacement. Drop‑in replacement designs accelerate OEM adoption and reduce service friction for end‑users.

- Bundle hardware with analytics and remote monitoring services. Integrating PID data with cloud analytics addresses rising demand for real‑time VOC plume tracking and compliance proofing.

- Target tactical M&A to close capability gaps. Focus on calibration labs, analytics startups, or specialized lamp/component suppliers to secure supply and accelerate time‑to‑market.

- Map procurement to regulatory scenarios. Use flexible procurement clauses to hedge against faster‑than‑expected regulatory tightening in priority jurisdictions.

Why PW Consulting’s full report is a must‑have for 2026

This primer outlines the strategic context; the full PW Consulting PID Sensors and Detectors Market report translates context into executable actions. It includes proprietary demand models, scenario testing, vendor scorecards, risk heatmaps, and commercial playbooks tailored for OEMs, industrial end‑users, service providers, and investors. The study reveals where margin pools will migrate under alternative regulatory and technology adoption scenarios and supplies the templates executive teams need to convert strategic intent into measurable outcomes.

Next step

For teams preparing capital allocations, R&D priorities, or M&A screens in 2026, the full PW Consulting report provides the granular insights and tools required to convert market growth into sustainable competitive advantage. To review the complete segmentation tables, vendor scorecards, and our scenario workbooks, consult the report landing page and subscribe for the full dataset and strategic annexes.

For detailed analysis of this topic, please visit the official page:PID (Photoionization Detection) Sensors and Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com