Insufflation Needles Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-23 04:23:41

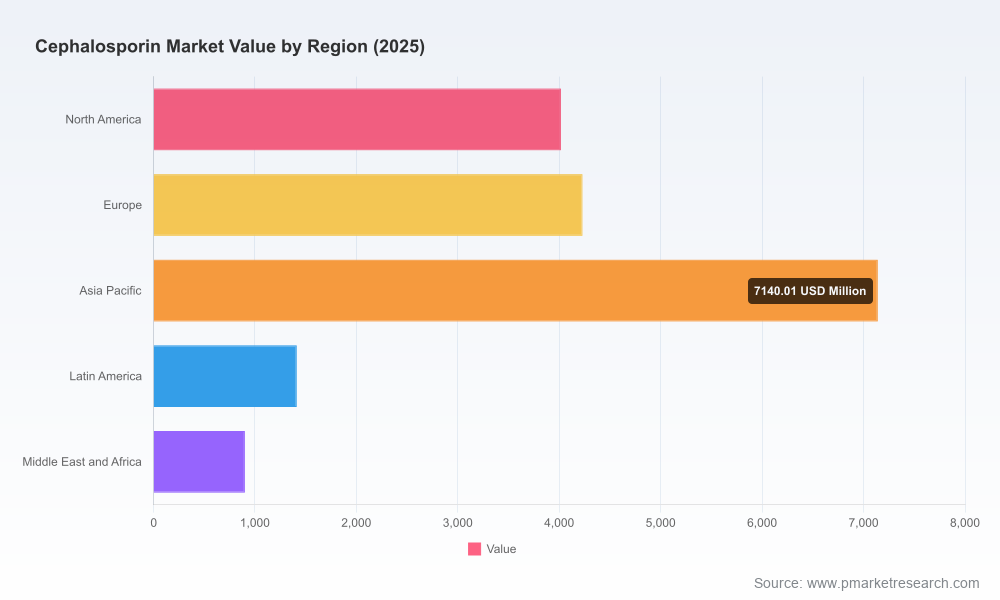

As global healthcare systems recalibrate in the post-pandemic era and antimicrobial stewardship gains urgency, the cephalosporin market presents a blend of stability and structural change. Our PW Consulting market model, with a 2025 base year and a forecast window running 2026‑2032, projects steady expansion at a compound annual growth rate (CAGR) of 3.0% across the forecast period. The market reached approximately USD 17.7 billion in 2025 and is expected to approach the low‑twenty billions by the end of the forecast horizon. This steady growth masks important inflection points — shifts in supply‑chain geography, regulatory pressures, product innovation and procurement dynamics — that will determine winners and losers through 2026 and beyond.

Cephalosporin Market

Leaders in pharma manufacturing, API supply, private equity, hospital procurement and policy need a concise, actionable synthesis of the structural forces shaping demand and supply. The key strategic choices in 2026 will hinge on three questions:

Cephalosporin Market

This introduction highlights where value is concentrated, the types of moves that are proving effective today, and why the full quantitative segmentation and scenario modeling in our report are essential to set a 2026 playbook.

Cephalosporin Market

The market’s modest but reliable CAGR reflects two offsetting dynamics. On the demand side, cephalosporins retain broad clinical relevance across a spectrum of infections, supporting consistent baseline consumption. On the supply side, price and procurement pressures — driven by genericization and hospital contracting — constrain headline growth. The result is a “mature growth” profile: predictable, low‑volatility expansion that rewards scale and operational resilience.

For 2026, this implies that incremental growth strategies focused on product mix upgrades (higher‑value formulations, combination therapies) and route‑to‑market optimization will generally outperform broad volume plays. Investors should favor strategies that protect margins rather than pure volume accumulation.

The cephalosporin value chain is tightly coupled to a small number of geographic production clusters for core intermediates. That concentration produces material price and availability leverage for those upstream producers and raises geopolitical and tariff vulnerability for downstream manufacturers and importers. Since early 2025, tariff measures and trade policy changes have already altered landed cost dynamics for many buyers, and continued policy volatility is a credible downside risk to margin forecasts in 2026.

Regulatory regimes are also reshaping competitive advantage. Authorities such as the US FDA and NMPA have intensified scrutiny of anti‑infective GMP compliance and are prioritizing certain novel cephalosporin combinations as part of antimicrobial resistance strategies. These regulatory trends favor firms with validated, inspected plants and established cross‑jurisdiction approvals.

The global supplier set combines large diversified multinational pharmas, established generic manufacturers with integrated API capabilities, and regional specialists with focused injectable or fermentation strengths. Market concentration metrics indicate a moderate top‑player share — enough to create scale advantages for certain incumbents but not enough to preclude nimble challengers from gaining ground through targeted moves.

Recent regulatory and commercial developments exemplify these dynamics: an approved cefepime‑combination for complicated urinary tract infections in 2026 demonstrates how a targeted product approval can unlock higher‑value hospital indications; new injectable plants inaugurated in 2025 signal renewed investment in parenteral capacity; and approvals in large regulated markets continue to be a gating factor for premium market access.

This market preview is intentionally selective. The complete PW Consulting Cephalosporin Market report provides the operational detail that active decision‑makers require, including:

We deliberately withhold the detailed numeric splits and proprietary scenario tables in this preview to protect the actionable intelligence that underpins those recommendations. Clients and subscribers can access the full dataset, models and country‑level risk matrices through the official report package.

Our modelling uses a base year of 2025 and historical calibration across 2020‑2025. Forecast scenarios run through 2032 underpinned by bottom‑up consumption models, supplier capacity inventories, and policy‑sensitive price curves. All revenue figures are denominated in USD (Million). Market concentration assessments rely on audited sales disclosures and proprietary channel checks; the current top‑player clusters show measurable scale but leave structural opportunity for focused challengers.

For leaders asking whether to prioritize scale, resilience or differentiation in 2026, the answer is context dependent but clear in direction: scale remains valuable for baseline competitiveness, yet sustainable margin expansion will come from de‑risking supply chains, securing regulatory footholds in high‑value hospital indications, and pursuing selective product innovation. The cephalosporin market is not a binary opportunity; it is a mosaic of stable cashflows and episodic value‑creation moments. Being positioned to act when one of those moments arises — regulatory approval of a novel combination, a regional capacity shortfall, or a tariff shock — will define outperformance through the decade.

PW Consulting’s full Cephalosporin Market report contains the detailed segmentation, scenario outputs and vendor scorecards necessary to convert insight into action. For teams preparing strategic plans and investment cases in 2026, the report provides the models and contractual templates that shorten decision cycles and reduce execution risk. Contact our market desk or download the full study to unlock the granular intelligence behind the forecasts summarized here.

For detailed analysis of this topic, please visit the official page:Cephalosporin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com