Glass-Resin Hybrid Lenses Market 2026 Growing at 8.7% CAGR with AR/VR and Imaging Innovation

Other |

2026-06-17 11:14:53

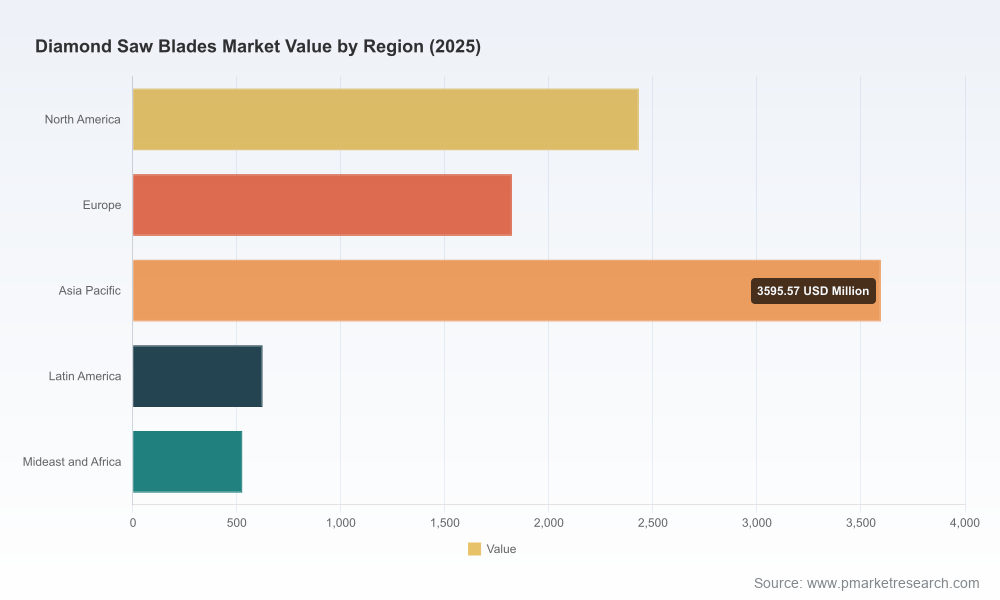

As capital allocation cycles reset and procurement leaders finalize 2026 roadmaps, an incisive understanding of the diamond saw blades market is no longer optional. Our latest market study, anchored on a 2025 base year and a seven-year forecast window through 2032, synthesizes macro trajectories, supply-chain fault lines, and competitive positioning to inform near-term commercial and operational choices. In brief: the sector recovered from a 2020 baseline and expanded to an estimated USD 9,000 Million by 2025, with a moderate compound annual growth rate of 2.41% projected across the 2026–2032 horizon. This preview highlights the strategic value of those insights for executives, buyers, and investors planning for 2026, while intentionally omitting granular segment-level outcomes to encourage access to the full study for transaction- or bid-critical detail.

Diamond Saw Blades Market

Several intersecting forces make 2026 a pivotal year for players across the value chain. First, steady but modest market growth has shifted the conversation from “share capture through volume” to “margin protection through specialization.” Second, upstream material sourcing and regulatory signals are reconfiguring supplier footprints, which means procurement teams must decide between consolidating suppliers for scale or diversifying to reduce geopolitical and regulatory exposure. Third, demand-side drivers — a renewed emphasis on energy efficiency in construction, automation to mitigate labour shortages, and rising expectations for precision cutting in infrastructure projects — are altering product specifications and after-sales service needs. Our research decodes these dynamics and translates them into executable choices for 2026 budget cycles.

Diamond Saw Blades Market

Scale and trend: The industry expanded from a 2020 baseline to approximately USD 9,000 Million by 2025, and is forecast to continue growing to a larger market size by 2032 under a steady CAGR of 2.41%. This trajectory indicates a mature market with pockets of upgrade-driven growth rather than disruptive expansion.

Diamond Saw Blades Market

Concentration: Market concentration metrics show moderate fragmentation (leading three and five players do not dominate the sector), implying persistent opportunities for specialized entrants, private-label strategies, and regional suppliers to retain local advantages.

Supply-side sensitivity: Synthetic diamond segments—central to product performance—are subject to sourcing complexity and regulatory oversight. Recent customs rulings and origin disclosures highlight that primary sources span multiple countries, increasing the need for traceable, resilient procurement strategies.

From a practical standpoint, three dynamics require immediate attention in 2026 planning:

Material provenance and regulatory compliance: Visibility into synthetic diamond supply chains is now a contract-level requirement for many enterprise buyers. Companies with documented, audited sourcing will enjoy preferential access to large construction and infrastructure tenders.

Product differentiation through engineering: Energy-efficiency mandates and the push toward automated cutting stations increase demand for blades that deliver repeatable, precision cuts with lower power draw and longer life cycles. R&D investments that reduce cycle time and improve segment metallurgy will yield outsized returns in specific subsegments.

Aftermarket and lifecycle services: As capital equipment suppliers and general contractors prioritize uptime, bundled offerings—spare inventory programs, predictive replacement cycles, and certified mounting/training services—create new recurring revenue pools. Suppliers who can operationalize service-level agreements will lock in higher customer lifetime value.

Our competitive audit profiles established manufacturers, OEM power-tool divisions, and specialist distributors. Each cohort brings distinctive advantages and emerging vulnerabilities:

Traditional manufacturers (examples include firms producing premium segmented, continuous rim, and turbo blades) continue to compete on product breadth and established distribution channels. Their strengths are deep application know-how and wide aftermarket footprints; their challenge is margin compression as commoditization pressures excess capacity.

Power tools divisions of larger industrial groups leverage brand, integrated tool-blade offerings, and cross-selling into broader equipment portfolios. Such companies are well-positioned to influence specification standards, but strategic realignments—such as announced exits from non-core stone tool businesses—create short-term disruptions and competitive openings.

Specialist distributors and newer manufacturers focus on speed-to-market and customization. Their agility is a competitive asset in retrofitting and niche industrial applications, though they must scale quality assurance processes to compete for institutional contracts.

Illustrative corporate reads from our study:

Suppliers with legacy strengths in masonry and concrete cutting remain the default choice for many contractors because of proven performance across wet and dry use cases. Several US-based and European players anchor this tier.

Industrial abrasives specialists bring advanced segment formulations and abrasive engineering experience into blade design — an advantage where material-specific performance dictates unit economics.

Emerging firms using automated production techniques and laser-welded technology position themselves as high-consistency suppliers, particularly attractive to OEMs and precision-focused end users.

Trade shows and new product introductions continue to be the primary channels for product visibility and specification updates; several exhibitors and catalog launches in late 2025 and early 2026 signal a fresh wave of tool optimization for tiling and stone applications.

Targeted product announcements and technical reviews are being published by distributors and specialist retailers, underscoring the importance of third-party validation in purchasing decisions.

Corporate restructuring in established tool groups, including announced discontinuation of certain stone tool activities, will alter competitive footprints and dealer networks — creating both short-term supply gaps and medium-term consolidation opportunities.

Our full study is built for decision-makers who need more than narrative — they need executable options. The deliverables include:

A rigorous market-sizing model spanning 2020–2032 with transparent assumptions and sensitivity scenarios to stress-test budgets and investment thesis under varying demand and cost trajectories.

Strategic supplier-risk maps highlighting exposure to single-source synthetic diamond suppliers and regulatory choke points, with recommended contingency procurement ladders.

Competitive benchmarking across product quality, go-to-market strategy, and aftermarket capabilities, coupled with an assessment framework for potential M&A targets and partnership candidates.

Commercial playbook entries: price-indexing guidance, inventory optimization heuristics for contractors versus distributors, and service-bundling templates designed to convert transactional customers into subscription-style accounts.

Operational modules: recommended best practices for blade mounting, handling and safety protocols to reduce field failures, and a supplier qualification checklist aligned with major tenders' procurement criteria.

Scenario-driven investment cases for product R&D, automation enabled manufacturing, and route-to-market experiments—each with expected payback windows and sensitivity to raw-material cost shocks.

Procurement: Implement a two-track sourcing approach—secure long-term agreements with audited suppliers for critical synthetic-diamond components while qualifying a secondary supplier pool to mitigate disruption risk.

Product and R&D: Prioritize development of energy- and life-cycle-efficient blades for automated cutting equipment and infrastructure projects where precision and throughput are valued.

Sales and Distribution: Test bundled service offerings in pilot regions to shift from unit sales to higher-margin aftermarket contracts. Leverage partnerships with power-tool OEMs to co-develop specification-compliant kits.

M&A and Portfolio: Monitor portfolio realignments by major tool groups as attractive entry points for acquiring channel access, intellectual property, or regional production capacity at favorable valuations.

Compliance and Risk: Integrate traceability clauses and country-of-origin audits into supplier contracts to ensure compliance with customs rulings and client procurement demands.

This article is intended as a strategic primer. It surfaces the most consequential trends, competitive moves, and procurement considerations for 2026, while withholding the granular segmentation tables and region/application-specific allocations that are essential for procurement bids, M&A modelling, and product-line P&L creation. The full PW Consulting report contains the data tables, supplier lists, and scenario spreadsheets required to execute the recommendations outlined above.

For executives and investors, the diamond saw blades market in 2026 will reward disciplined strategy over broad-stroke expansion. The pace of growth is predictable enough to plan capital, but nuanced enough — shaped by supply-chain provenance, regulatory shifts, and product-technology pairing — to require informed judgment. PW Consulting’s study translates these complexities into tactical roadmaps: protect margins by shoring up raw-material and regulatory risk, differentiate through application-specific engineering and services, and position for consolidation opportunities as incumbents and new entrants reconfigure their portfolios. To move from strategy to execution, access to the report’s full segmentation, source tables, and executable models is essential.

Contact PW Consulting to obtain the full Diamond Saw Blades Market report and the accompanying decision-support toolkit for 2026 planning.

For detailed analysis of this topic, please visit the official page:Diamond Saw Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com