Global LED Display Screen Market Growing at 5.3% CAGR Through 2032

Other |

2026-07-08 11:55:11

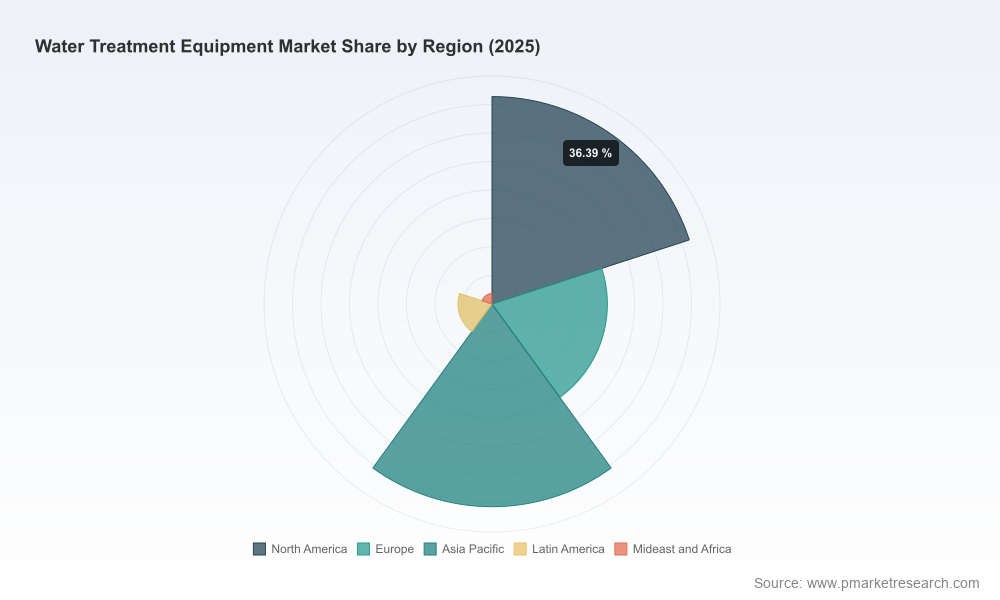

As capital allocations tighten and regulatory pressures mount, water treatment equipment has moved from an operational line item to a strategic battleground. PW Consulting’s latest Water Treatment Equipment Market study (base year 2025, forecast 2026–2032) synthesizes macro momentum, technology inflection points, and competitive positioning into a practical playbook for 2026 decision‑makers. The global market reached approximately USD 66.0 Billion in 2025 and continues to expand at a multi‑year compound annual growth rate of 6.2%, moving toward a near‑hundred‑billion‑dollar opportunity by the early 2030s. This article distills the study’s executive takeaways — intentionally high‑level to preserve the detailed segmentation and proprietary datasets available in the full report.

Water Treatment Equipment Market

Capital allocation: Equipment spending is increasingly driven by compliance deadlines, energy reduction targets, and the economics of reuse. Our forecast and scenario models translate these forces into investment pacing and capacity timing, helping CFOs and asset owners prioritize projects in 2026.

Water Treatment Equipment Market

Technology selection: Membrane advances, modular ZLD, intelligent pumping, and digital dosing platforms are reshaping lifecycle costs. The study evaluates technology TCO under real operational constraints to guide procurement and pilot decisions.

Water Treatment Equipment Market

M&A and partnership diligence: With a market that remains fragmented (CR3 ~24%; CR5 ~30%), the landscape favors bolt‑on consolidation, vertical partnerships, and service expansion. Strategic acquirers and private equity can use our competitive overlays and valuation comparators to identify high‑impact targets.

Regulatory readiness: New mandates and public financing mechanisms are accelerating upgrade cycles. Our regulatory impact maps and funding scenarios show where grant/loan availability alters project viability and how to structure bids to capture subsidized infrastructure spend.

A concise set of market drivers will dictate winners in 2026 and beyond. First, regulatory momentum — including fresh mandates requiring smart water management — is forcing fleetwide modernization. Second, energy intensity is an increasingly visible line on utility and municipal balance sheets: energy accounts for a material share of treatment operating costs, and targeted efficiency practices in plants can unlock double‑digit reductions in OPEX.

Third, infrastructure renewal needs and the economics of water reuse are pushing industrial and municipal operators toward higher‑value solutions such as membrane systems, ZLD modules, and integrated monitoring/dosing platforms. Fourth, raw material and supply chain constraints continue to favor vendors with robust procurement strategies and modular, field‑serviceable designs.

Finally, digitalization — from AI‑driven pump optimization to real‑time chemical dosing platforms — is moving from “nice‑to‑have” to contractual requirement in many procurement processes. Vendors who can demonstrate measurable reductions in energy, chemical consumption, and unplanned downtime will increasingly command premium pricing.

The market exhibits a blend of global service integrators, specialized equipment makers, chemical platform providers, and strong regional players. Competitive positions vary by technology stack, service capability, and route‑to‑market:

Aquatech — Industry leader in desalination, water reuse, and ZLD. Strengths: end‑to‑end project delivery for industrial and municipal clients; implied upside in modular, factory‑built solutions for repeatable plant types.

Calgon Carbon — Deep expertise in adsorbents, UV, and ion exchange. Strengths: materials and consumables business model that supports recurring revenue and retrofit pathways.

The Dow Chemical Company — Materials and membrane chemistry capabilities that underpin low‑energy separation. Strengths: R&D leverage and scale in membrane substrate supply chains.

Evoqua Water Technologies — Focused on compliance and process‑level solutions for municipal/industrial customers. Strengths: service contracts and regulatory know‑how that lower buyer risk.

Veolia & SUEZ — Global operators with integrated water management services and broad membrane portfolios. Strengths: full‑lifecycle service offerings and municipal concessions; strategic value in bundled solutions.

Xylem & Grundfos — Technology leaders in pumps and digital monitoring. Strengths: platform play — intelligent pumps and telemetry that reduce operating costs and create SaaS‑adjacent revenue streams.

Pentair & Ecolab — Combined reach across residential, commercial, and industrial channels. Strengths: cross‑sell opportunities, especially when chemical controls and filtration can be bundled.

Kurita & Newater — Regional specialists with strong industrial process know‑how and custom engineering. Strengths: speed to specification and deep local relationships in industrial accounts.

VESSCO, ALAR, WTS — Distribution and factory‑direct equipment specialists supporting retrofit and localized service needs. Strengths: aftermarket parts, rapid deployment, and last‑mile service networks.

Recent product launches underscore the shape of near‑term competition: new intelligent pumps with AI flow control (late‑2025 launches), next‑generation UV disinfection systems with advanced monitoring (early‑2026), modular ZLD units for industrial users (2025), and ultra‑fine whole‑house RO systems introduced at trade events (2026). These introductions highlight vendor strategies: differentiate on energy, digital ROI, modularity, or consumable lock‑in.

Transparent market sizing and methodology that reconciles historical data (2020–2025) with scenarios to 2032, including base, high‑adoption, and constrained‑supply cases.

Scenario‑based procurement and capex/opex models that convert technical choices into multi‑year financial outcomes.

Regulatory impact matrices and public‑funding overlays that identify where financing changes project economics.

Technology roadmaps and adoption curves for membranes, disinfection, ZLD, and digital platforms — with technology risk scoring and adoption timeframes.

Competitive playbooks and an M&A/partnership heatmap: where to buy, partner, or build for capability acceleration.

Procurement templates, supplier scorecards, and deployment case studies with quantified energy and OPEX savings.

Company profiles and strategic SWOTs for leading vendors, plus a fragmentation analysis that quantifies consolidation opportunity (market concentration metrics included).

To be clear: this article intentionally summarizes executive insights. The full report contains granular segmentation by region, type, and application, and the underlying data tables used to build the forecasts and financial models. Those detailed splits and datasets are not reproduced here so that strategic users engage directly with the complete analysis.

0–90 days: Run a portfolio triage. Categorize assets by regulatory urgency, energy intensity, and retrofit feasibility. Launch 1–2 “fast‑payback” pilots that combine energy‑efficient hardware and digital performance monitoring to demonstrate savings.

3–12 months: Lock in medium‑term supplier relationships with outcome‑based contracts. Prioritize vendors who can bundle digital monitoring, consumables, and service level agreements to reduce vendor churn and total lifecycle cost.

12–36 months: Move from pilots to scale. Deploy standardized modular platforms where repeatable plant types exist. Where appropriate, pursue bolt‑on acquisitions or strategic alliances to fill capability gaps in membrane engineering, ZLD, or digital platforms.

Investor guidance: For financial sponsors evaluating the sector, target companies with recurring revenues (service/consumables), differentiated digital platforms, and defensible engineering IP. Fragmentation points and regulatory tailwinds create clear arbitrage for consolidation plays.

The water treatment equipment market in 2026 sits at the intersection of regulatory acceleration, energy stewardship, and digital transformation. With the global market expanding from its mid‑2020s base and a fragmented competitive field, the next 24 months will reward organizations that move quickly to standardize modular offerings, demonstrate measurable OPEX reductions, and secure lifecycle‑oriented customer relationships.

PW Consulting’s full Water Treatment Equipment Market report translates these conclusions into executable workstreams, financial models, and vendor due‑diligence templates tailored to investment committees, utilities, industrial operators, and equipment manufacturers. For teams seeking the granular segmentation, proprietary datasets, and transaction support that turn strategy into action, the complete report and our advisory services are available through PW Consulting.

For detailed analysis of this topic, please visit the official page:Water Treatment Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com