Destockage: How to Save Smartly on Bulk Products

Other |

2026-03-27 11:56:47

As PW Consulting’s lead industry analyst, I present a concise, decision-ready introduction to our full Bolt (Fastener) Market study. This briefing is written for C-suite executives, procurement leaders, private equity investors, and corporate strategy teams who must calibrate capital allocation, sourcing and M&A strategies in 2026. It synthesizes market dynamics, competitive positioning and actionable scenarios while preserving the proprietary segment-level detail contained in the full report — a deliberate “trailer” that demonstrates our analytic depth and strategic framing while directing readers to the source for the underlying tables, models and breakouts.

Bolt (Fastener) Market

Comprehensive market sizing and forward-looking forecasts grounded in a proprietary demand model spanning 2020–2025 (historical) with 2025 as the base year and a formal forecast horizon from 2026–2032.

Bolt (Fastener) Market

Scenario-driven revenue projections and sensitivity analysis to raw material swings, labor constraints and demand shocks — all denominated in USD (Million) for consistency across commercial and investment use cases.

Bolt (Fastener) Market

Competitive benchmarking across manufacturing, distribution and solution providers, coupled with go-to-market playbooks, supplier scorecards and M&A screens tailored to strategic acquirers and corporate development teams.

Operational playbooks for procurement and manufacturing leaders focused on cost-to-serve optimization, inventory strategy under price volatility and automation ROI for assembly operations.

The bolt and fastener market has demonstrated steady expansion through the early 2020s. Our topline market model shows growth from the start of the historical window through the base year, with continued expansion across the forecast period. Using 2025 as the base year, our long-range model projects a compound annual growth rate (CAGR) of 3.48% for the 2026–2032 forecast window. All figures in the full study are presented in USD, revenue unit: Million, and are supported by time-series demand drivers calibrated to end-market activity in automotive, construction, machinery and other adjacent sectors.

Put simply: the market is large, persistent and commercially attractive — not a hyper-growth interrupter, but a resilient industrial segment where small percentage changes in share, supply cost or service level translate to meaningful P&L and valuation impact. That profile makes the space ideal for operational improvement plays, bolt-on consolidation, and targeted innovation adoption.

Raw material volatility remains the most consequential supply-side input. Our monitoring in mid‑2026 shows steel prices elevated relative to the prior year, a pattern that amplifies cost passthrough pressure across manufacturing and distribution channels. The full report includes a steel-sensitivity module that quantifies margin erosion and customer price elasticity under multiple pricing paths.

Standards and technical governance are reasserting influence. Industry bodies have stepped up standards activity and education, evidenced by new initiatives and events focused on harmonizing testing and specification practices. For product-heavy manufacturers and exporters, compliance preparedness — test labs, traceability and certifications — is now part of the minimum competitive baseline.

Labor and capacity constraints are structural. The market remains labor-intensive across manufacturing clusters and employes millions globally; labor shortages and skill mismatches are producing recurring supply chain friction. Expect continued premium on predictable lead times and logistics sophistication.

The industry sits in a mid‑consolidation state. Market concentration metrics indicate that the top three players control a meaningful but not dominant share, while the top five increase that footprint modestly — a constellation that creates opportunity for scale-driven margin improvement yet leaves room for specialized competitors to preserve niches.

Würth Group (Künzelsau, Germany): A global distribution and service powerhouse. Würth’s breadth — a full range of bolts, screws and assembly materials served through an extensive branch network — makes it a go-to partner for multisite industrial customers requiring logistics-enabled fulfillment. Strategic takeaway: Würth’s model highlights the value of integrated distribution networks and field‑level customer intimacy.

LISI Group (Grandvillars, France): A specialist in high‑value fasteners for aerospace, automotive and medical applications. LISI’s focus on demanding end markets underscores the margin premium for qualification-heavy product sets and the barrier to entry created by certification cycles. Strategic takeaway: vertical specialization and engineering collaboration unlock superior margins and defensibility.

Bossard Group (Zug, Switzerland): Differentiated by fastening technology and logistics systems tailored to manufacturing automation. Bossard’s emphasis on system-level offerings (fastener + logistics + advisory) signals the future for suppliers: move from commodity to solution-led revenue.

SFS Group (Heerbrugg, Switzerland): Has a reputation for precision mechanical fastening systems. For buyers in precision assembly, SFS represents a quality/innovation playbook — and for investors, a potential acquirer of engineering-led assets.

Bulten AB (Gothenburg, Sweden): Automotive-focused fastener specialist with deep OEM relationships. The company demonstrates the value of long-term supply contracts and engineering collaboration in cyclical industries.

Hilti Corporation (Schaan, Liechtenstein): Known for high-performance construction fasteners and tools; Hilti’s brand and system selling in construction illustrates how product + service can command pricing premium and reduce commoditization risk.

Precision Castparts Corp (Lake Oswego, Oregon, USA): Supplier of high-strength cast and forged components for aerospace and power generation. Their capability set emphasizes advanced metallurgy and machining competence that commands differentiated pricing.

Across these profiles, two themes emerge: (1) logistics and service sophistication matter as much as unit economics; (2) technical specialization (aerospace-grade, high-strength, precision) creates defensible value chains that are less susceptible to pure price competition.

2026 trade platforms and industry forums have accelerated networking and innovation diffusion — major expos and institute events in 2026 provided concentrated venues for technology transfer, supplier discovery and standards alignment.

Standards camps and governance activity in 2026 also signaled a coordinated push toward higher consistency in specification and testing. This is relevant to any firm planning to export or pursue OEM contracts that require documented qualification processes.

Procurement resilience: Implement dynamic hedging and multi-source contracts tied to steel indices. Our report’s pricing scenario tool helps quantify the trade-offs between fixed-price, index-linked and spot purchasing strategies for common contract tenors.

Operational acceleration: Prioritize automation in assembly lines where labor scarcity and variability drive the highest cost-to-serve. The financial case in the full report prioritizes retrofits with <1.5–2.5 year payback in typical mid-sized plants.

Value migration: Suppliers should migrate up the value chain by packaging logistics, inventory management and technical advisory with physical product, capturing service margins and reducing price elasticity.

M&A and partnerships: Target assets that either (a) plug distribution or geographic coverage gaps, (b) add engineering/specification capabilities in high-barrier end markets, or (c) expand automated assembly service offerings. The report’s M&A screening matrix ranks targets by strategic fit, integration risk and expected synergies.

Standards and certification readiness: Build a prioritized certification roadmap if pursuing aerospace, medical or regulated construction segments — being first to certification in a sub-region provides early-mover negotiation leverage.

Granular, source-backed market size time series (2020–2025) and a transparent, auditable forecast model (2026–2032) with scenario toggles.

Cost and margin waterfall analyses, including steel sensitivity and labor-cost scenarios.

Actionable commercial playbooks for suppliers, distributors and end-users; model scripts for contract negotiation and inventory optimization.

Comprehensive competitor dossiers, executive contact mapping, and a prioritized opportunities pipeline for M&A and strategic partnerships.

Interactive dashboards and downloadable appendices (financial model, supplier scorecards and regulatory checklist) designed to accelerate decision turnarounds.

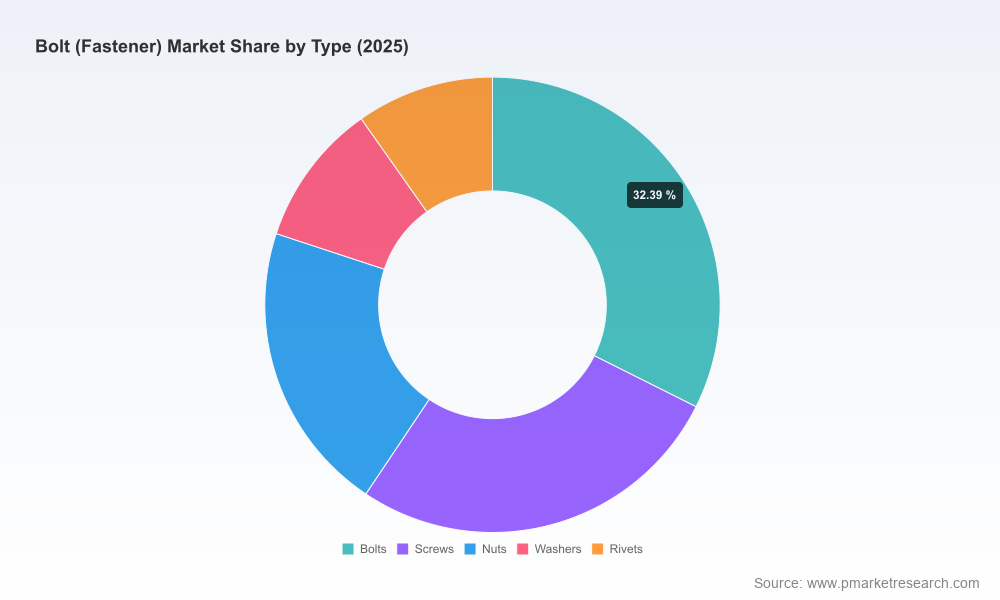

Important governance note: while this briefing highlights strategic directions and top-line market trajectories, it intentionally withholds the proprietary segment-by-segment breakouts and certain granularity in regional/application-level percentages to preserve the analytical value of the full study. Accessing the full dataset unlocks the specific splits, price curves and the downloadable model that enable precise investment sizing, integration planning and procurement contract drafting.

For 2026, the critical choices for firms in the bolt and fastener ecosystem are not whether demand exists — it does — but where to capture value along a shifting supply chain and standards landscape. PW Consulting’s Bolt (Fastener) Market study furnishes the maps, the scenarios and the executable playbooks: from procurement optimization and pricing strategy to M&A due diligence and operational transformation. If your priority is shortening the decision cycle and de‑risking a strategic move in this market, our full report and advisory team are prepared to help you convert modeled insight into measurable results.

To unlock the proprietary segment-level tables, regional and application breakouts, and the downloadable financial model that underpin the scenario analyses referenced here, please visit our research page or contact our advisory desk for an executive briefing and model access.

For detailed analysis of this topic, please visit the official page:Bolt (Fastener) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com