HD Map Market 2026: A Strategic Preview for Executive Decision-Making

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our HD Map Market research — a director’s cut that explains why this dataset will be instrumental to corporate strategy in 2026. This briefing demonstrates the analytical depth we applied, highlights the strategic inflection points that matter to automotive OEMs, Tier-1 suppliers, mapping vendors, and investors, and outlines immediate actions executives should prioritize. True to the “trailer” principle, we illustrate the framework and implications while intentionally withholding detailed segmentation tables and proprietary model outputs; access to the full report is required to obtain the granular inputs and financial models that underpin these recommendations.

HD Map Market

Market trajectory: scale, speed, and what it means for 2026

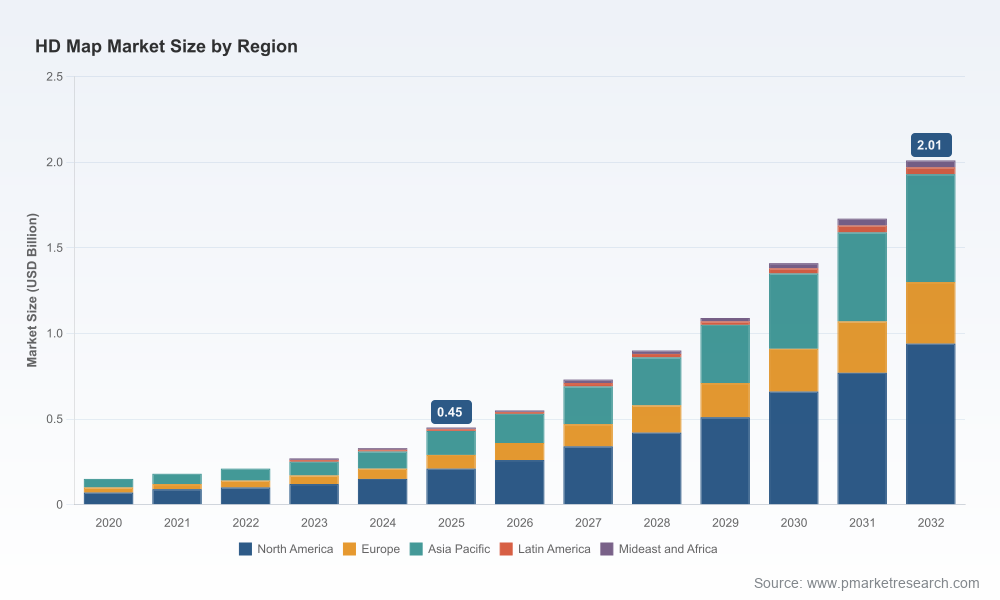

The HD map market has moved from a nascent, niche product to a commercially material infrastructure layer in just a few years. Our baseline shows a clear multi-year expansion: after steady growth through the early 2020s, the market accelerates into the second half of this decade. Using 2025 as our base year, the market size is positioned on an upward path driven by ADAS upgrades, initial SAE Level 3/4 rollouts, and an expanding set of safety-regulation use cases. Our forecast period (2026–2032) is modeled with a compound annual growth rate of approximately 21.74%, reflecting both rapid adoption and increasing per-vehicle map spend as services evolve from static lane geometry to live, software-defined capabilities.

HD Map Market

For strategic leaders, the two takeaways are straightforward: (1) timing matters — investments made in 2026 will capture disproportionately larger revenue pools through 2030 due to compounding growth, and (2) product breadth and data freshness will quickly differentiate winners from commodity suppliers as HD maps become an active safety and autonomy enabler rather than a passive reference layer.

HD Map Market

Key strategic levers for 2026

- Product positioning — “real-time” vs “reference”: Firms must decide whether to compete on latency and live-layer integration (cloud-delivered, AI-updated tiles) or on embedded, deterministic maps that prioritize ultra-low latency and redundancy. The market will reward clarity: buyers prefer suppliers who explicitly map their technical trade-offs to ODD and compliance outcomes.

- Partnerships and OEM integrations: Expect consolidation around OEM partnerships and navigation stack integrations. Vendors that secure vehicle-level partnerships or preferred integration status with Tier-1s will capture licensing and data-revenue uplifts.

- Data supply economics: The core cost equation is labor versus compute and equipment. Companies that optimize a hybrid approach — selective manual labeling augmented by targeted ML retraining and strategic MMS deployments — will lower cost-per-kilometer while preserving quality for safety-critical features.

- Regulatory alignment: HD maps are now an instrument of compliance (e.g., ISA, GSR-related use cases) and of ODD definition for levels 2–4 autonomy. Mapping roadmaps should be designed around regulatory milestones to secure preferred procurement slots with regulated fleets.

- Go-to-market and pricing: Buyers expect flexible licensing: bundled vehicle subscriptions, per-km consumption models for fleet operators, and premium real-time SLAs for automated-driving deployments. Firms that test and pilot hybrid pricing in 2026 will be best positioned to scale through 2027–2028.

What the full PW Consulting HD Map Market report delivers

The full research package translates market insight into operational playbooks. Highlights include:

- Methodology and assumptions behind the market model (historical 2020–2025 calibration, base-year definitions, and forecast scenarios for 2026–2032).

- End-to-end segmentation framework across delivery architecture (cloud vs embedded), application stack (autonomy, ADAS, telematics), and commercial models (OEM license, data-as-a-service, subscription).

- Vendor scorecards with capability matrices, go-to-market profiles, and comparative technology assessments — including data-refresh cadence, positional accuracy, and SLAs.

- Operational cost models for map production covering MMS fleet ops, sensor CAPEX, labeling labor, and ML compute — including sensitivity testing and break-even analyses for insourcing vs outsourcing collection and mapping.

- Regulatory impact maps that tie HD map requirements to specific compliance regimes and ODD definitions across major markets.

- Strategic playbooks: M&A target screens, partnership negotiation templates, pilot design blueprints, and an investor-ready market-entry memorandum.

These deliverables are designed as “plug-and-play” tools for commercial and product teams: practical templates and model files let users move immediately from insight to pilot to procurement.

Competitive landscape: who sets the technical and commercial bar?

The supplier field is evolving from pure-mapping players to integrated data-and-software platforms. A few illustrative vendor profiles from our coverage:

- HERE Technologies (Eindhoven, Netherlands) — Known for an HD Live Map offering and an expanding portfolio that bridges live map tiles with software for driver assistance and autonomy. Recent product launches emphasize AI-driven, software-defined vehicle capabilities, signaling a clear move to embed mapping as a run-time software asset rather than a static dataset. (See: here.com)

- Dynamic Map Platform (DMP) (Livonia, Michigan, USA) — Positions itself on absolute accuracy and mile-depth coverage in North America with a dual focus on e-Horizon software and ODD-support tools. DMP’s recent coverage expansions reinforce a coverage-and-accuracy play to win OEM fleet contracts that prioritize deterministic performance over generalized coverage. (See: dmp-maps.com)

- Mapbox (San Francisco, USA) — Transitioning from a developer-focused mapping platform to an in-car HD map enabler. Its 3D Lanes feature and vehicle integrations demonstrate a strategy built on flexibility and embedded navigation partnerships with automotive OEMs and tier suppliers.

Collectively these vendors illustrate three viable paths to value in 2026: (a) platform incumbency with integrated live services, (b) high-accuracy, coverage-first propositions serving regulated fleets, and (c) developer- and OEM-friendly embedded stacks. The market remains neither winner-take-all nor highly fragmented; we observe a moderate concentration where leading platforms exert meaningful influence, but technical specialization leaves space for focused challengers.

Recent product moves and their strategic implications

- January 2026: A major incumbent announced an AI-first software portfolio for software-defined vehicles. Strategic implication: mapping is evolving into a real-time runtime service; buyers will demand continuous update pathways and deterministic integration models.

- August 2025: A coverage-specialist expanded continental mileage claims with tight accuracy guarantees. Strategic implication: fleet buyers and regionally dominant OEMs will select suppliers based on local coverage-and-accuracy fit, accelerating multi-vendor procurement strategies.

- January 2026: An innovation-led player released 3D lane navigation and vehicle integrations with a global OEM. Strategic implication: partnerships that embed map features into vehicle UX create sticky value and new monetization levers (aftermarket updates, safety services).

Operational frictions and friction-mitigation strategies

The HD map value chain is subject to several persistent constraints that will shape practical strategy in 2026:

- Labor vs. compute trade-off: High-quality HD map production still depends on either intensive manual labeling or substantial ML compute. Firms must assess where semi-automated labeling pipelines and active-learning loops can materially reduce per-kilometer costs without degrading safety-critical accuracy.

- Equipment and MMS dependency: Accurate, production-grade HD maps require Mobile Mapping System (MMS) vehicles outfitted with LiDAR, cameras, and GNSS-RTK. For most buyers, partnering with local collectors or leasing sensor-equipped fleets will be more economical than in-house scale-up in 2026.

- Supply chain and localization: Specialized mapping hardware is concentrated in a few geographies. This reliance creates opportunities for regional data-collection partnerships and for companies that can design sensor-agnostic ingestion pipelines.

- Regulatory overlay: HD maps are directly implicated in compliance features (e.g., speed assistance) and ODD definitions. Mapping teams need to build traceable, auditable update chains and versioning to satisfy regulatory requirements and to support certification workflows for AD features.

Recommended 90-day agenda for executives (practical, prioritized)

- Run a rapid supplier audit: identify existing map suppliers, current SLAs, update cadences, and data-license clauses tied to autonomy/regulatory uses.

- Design and launch a 6–12 month pilot with at least two contrasting suppliers (one coverage/accuracy specialist and one platform player) to benchmark real-world update latency and integration ease.

- Initiate an MMS sourcing review: evaluate leasing, JV, or contract-collection options by total cost of ownership and time-to-coverage.

- Establish a regulatory-mapping checklist for ISA and ODD compliance; map product roadmaps to expected regulatory milestones in target markets.

- Create a data-ops playbook: ingestion, labeling, QA thresholds, model retraining cadence, and rollback procedures — include cost-per-kilometer metrics and SLAs.

- Prepare an M&A/partnership screen: targets that deliver either geographic coverage, unique sensor-capture capability, or a proprietary live update engine.

Closing: why this preview should shift your Q2–Q4 2026 priorities

HD maps have transitioned from an engineering curiosity to a commercially decisive input for vehicle safety, automation, and software-defined features. The market’s rapid CAGR means early action in 2026 buys meaningful strategic optionality through 2030. Executives who clarify which part of the value chain they want to own — live runtime services, deterministic embedded maps, or data-collection infrastructure — will be able to translate that choice into clearer procurement specifications, partnership strategies, and capital plans.

PW Consulting’s full HD Map Market report contains the underlying models, segmented demand curves, vendor scorecards, and executable templates that boards and investment committees need to make those choices. For access to the complete dataset, financial models, and supplier playbooks — including the confidential segmentation tables and per-region, per-application forecasts omitted from this preview — please visit the source webpage linked in our release notice.

For detailed analysis of this topic, please visit the official page:HD Map Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com