Chromated Copper Arsenate Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a concise but incisive preview of our new Chromated Copper Arsenate (CCA) Market study — built to inform executive decisions across commercial wood treatment, utilities, infrastructure, and specialty chemical supply chains in 2026. This preview follows a “trailer” logic: it surfaces rigorous, actionable insight while intentionally reserving core, segment-level tables and models for the full report. Decision-makers who need immediate, high-confidence guidance will find the themes and recommended plays below directly applicable; teams requiring transaction-grade inputs and granular demand scenarios should consult the complete study on our site.

Chromated Copper Arsenate Market

Market Trajectory at a Glance

- Base/Reference year: 2025 (historical series 2020–2025; forecast window 2026–2032).

- Observed growth: the global CCA market expanded steadily through 2020–2025, rising from the low‑400s to the mid‑500s (USD Million) as the industry adapted to regulatory pressure and shifting end‑use demand.

- Near‑term momentum: our forecast period (2026–2032) projects continuation of modest expansion, driven by commercial, industrial and utility applications, with a compound annual growth rate (CAGR) of 3.8%.

- Market structure: concentration is moderate — the top three players account for roughly one‑third of the industry by revenue, with the top five nearing half of the market, underscoring opportunities for niche specialization and strategic consolidation.

Why This Matters for 2026 Decision Cycles

2026 marks a pivot year for incumbents and potential entrants. Regulators, customers and procurement authorities have clarified expectations around worker safety, labeling and disposal — imposing both compliance obligations and indirect cost pressure. Meanwhile, alternative preservatives and treatment technologies are commercially available but carry a measurable cost premium. For executives planning capex, pricing, sourcing, or M&A in 2026, three strategic implications stand out:

Chromated Copper Arsenate Market

- Risk‑adjusted cost planning is now table stakes. Alternatives to CCA increase treatment costs by a meaningful margin; buyers and suppliers must model total landed cost under multiple regulatory scenarios, not just material cost per unit.

- Regulatory compliance is a competitive moat — if managed proactively. Interim worker protection measures and ongoing registration reviews mean firms that can demonstrate advanced occupational controls and compliant labeling will face lower disruption risk and secure preferred customer status in industrial procurement.

- Selective consolidation and capability build‑outs create value. With moderate market concentration, well‑executed bolt‑on deals or strategic partnerships (e.g., logistics, specialty treatment capacity) can accelerate access to differentiated end‑markets while diluting regulatory and disposal risk across a larger revenue base.

Regulatory Dynamics: Constraints and Strategic Responses

Regulatory developments through late 2025 have crystallized the landscape. Key takeaways that should drive your 2026 strategy:

Chromated Copper Arsenate Market

- The U.S. EPA’s registration review of chromated arsenicals has introduced interim mitigation measures focused on worker protection. These are operationally consequential — they affect training, PPE, monitoring, and plant layout requirements.

- CCA products remain approved solely for commercial, industrial, and non‑residential uses; residential applications have been out of scope for years. This constrains end‑market expansion but clarifies permissible demand streams.

- The EPA identifies worker health risks (cancer and non‑cancer endpoints) as the primary concern, with no identified population‑level risk for the general public. For operators, this elevates occupational health programs from compliance checklist to strategic capability.

- Waste management must be factored into lifecycle economics: hazardous‑waste determinations and state‑specific disposal guidance may lead to variable end‑of‑life costs across jurisdictions.

Strategic responses we recommend: accelerate investments in industrial hygiene and engineering controls; standardize contractual clauses to shift remediation and disposal liabilities; and run scenario budgets for alternative‑preservative adoption across key customers.

Competitive Landscape — Who Matters and Why

The sector combines legacy chemical producers and specialized treatment operators. The report’s competitive analysis profiles leading players, their geographic footprints, and commercial positioning. Representative firms include:

- Koppers Performance Chemicals Inc. (Pittsburgh, Pennsylvania) — a vertically integrated manufacturer and supplier of CCA preservative chemistries and treated lumber for commercial, industrial, agricultural, marine, and utility pole applications.

- Goodfellow Inc. (Canadian operations with treatment facilities in eastern provinces) — a producer and applicator of CCA for commercial and industrial pressure treatment of poles, posts, and timber, serving regional markets with localized treatment capabilities.

- Chemical Specialties, Inc. (CSI) (Charlotte area) — a producer of CCA‑treated wood and preservative blends, focused on commercial, industrial and agricultural customers.

Implication: incumbent scale matters, but so do localized service capabilities (rapid turnaround, bespoke treatment specifications, disposal routing). Our benchmarking shows top players combine manufacturing scale with treatment networks and compliance programs — a combination that is difficult and costly for pure new entrants to replicate quickly.

Operational Playbook: Actions That Move the Needle in 90 Days

For commercial leaders and plant managers, the full report organizes executable initiatives into a 30/60/90 day roadmap. High‑impact short‑term moves include:

- 30 days: compliance triage — audit worker protection measures, update training, and map state disposal requirements for your top production sites.

- 60 days: cost re‑modeling — run TCO comparisons between CCA and available alternatives (include disposal and worker‑safety capex), and refresh supplier contracts with pass‑through clauses for regulatory‑driven cost changes.

- 90 days: commercial alignment — reprice long‑term bids to reflect compliance investments; prioritize accounts where customers value certified occupational controls and disposal assurance.

These are pragmatic steps that reduce immediate regulatory exposure while preserving commercial optionality as the landscape evolves.

Report Contents — Practical Tools You Can Deploy

The full PW Consulting study is structured to be operationally useful, not just descriptive. Highlights include:

- Scenario‑based demand models covering 2026–2032 with sensitivity runs for regulatory tightening, alternative substitution rates, and price pass‑through assumptions.

- Supplier and treatment‑facility scorecards (capex, throughput, compliance maturity) that you can use in procurement negotiations or M&A screening.

- Workforce and plant‑level mitigation playbooks: engineering control checklists, monitoring templates, and training curricula aligned to current EPA interim measures.

- Commercial impact matrices and pricing playbooks that translate cost‑and‑risk inputs into margin management strategies across customer segments.

- Disposal compliance guide with decision trees for hazardous‑waste determinations and state variability mapping, plus recommended contractual language for customers and waste vendors.

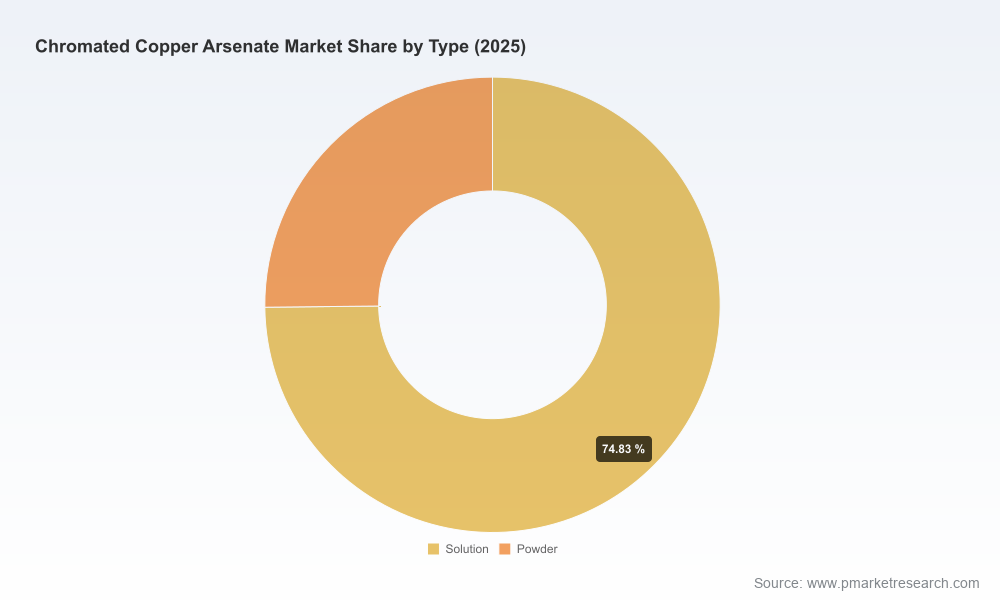

Note: while the preview discusses high‑level segmentation themes and market concentration, detailed segment tables (regional, application, and type splits) and full numeric models are available exclusively in the full report.

Strategic Scenarios — What Winning Looks Like

Based on the forecast baseline and the 3.8% CAGR through 2032, we model three pragmatic pathways for market participants:

- Defensive Optimization: minimize regulatory and disposal cost volatility through process upgrades and contracting, maintaining volume while protecting margins.

- Value Migration: selectively introduce higher‑margin alternative preservatives to capture customers prioritizing non‑CCA solutions, accepting near‑term margin compression for longer‑term portfolio resilience.

- Scale and Integrate: pursue consolidation or strategic alliances to spread compliance and disposal fixed costs over a larger revenue base — an effective approach where market share gains are feasible without large incremental capex.

Which path is optimal depends on your current market position, balance‑sheet flexibility, and customer mix. Our full suite of tools helps quantify the tradeoffs.

How PW Consulting Supports Executives in 2026

We deliver both the strategic narrative and the executional artifacts: customized scenario workshops, transaction diligence packages, and operational playbooks keyed to regulatory compliance. Our objective is to convert the admittedly complex regulatory and technical dynamics into prioritized, time‑bound actions that protect enterprise value and open selective growth avenues.

Next Steps

This preview is designed to equip leadership teams with the strategic framing necessary for 2026 planning cycles. For the full forecast models, segment level forecasts, supplier scorecards, and downloadable operational templates, consult the complete Chromated Copper Arsenate Market report on PW Consulting’s research portal. If you would like a tailored briefing for your executive team or a rapid 30‑day diagnostic of your production and compliance posture, our analyst team is available to support an accelerated engagement.

For detailed analysis of this topic, please visit the official page:Chromated Copper Arsenate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com