Percutaneous Nephroscope Market Overview: Key Drivers and Challenges

Other |

2026-04-17 03:57:37

As the automotive industry accelerates towards lighter, safer and more circular vehicle architectures, the car bumpers market is undergoing a measured but structurally significant transition. Our PW Consulting analysis places the global market at approximately USD 16.5 billion in the 2025 base year, following a trajectory that expands at a steady compound annual growth rate (CAGR) of 4.2% through our 2026–2032 forecast window. By 2032 the addressable market is projected to exceed USD 22 billion, driven by a mix of OEM specification shifts, aftermarket demand dynamics and regulatory pressure around material recyclability and end-of-life handling.

Car Bumpers Market

Policy momentum: Policymakers in major auto markets are moving from discussion to implementation on plastics recycling and landfill diversion measures. The European Commission’s late‑2025 policy analysis and regional landfill bans are already changing supplier economics and procurement specifications.

Car Bumpers Market

Supply-chain reconfiguration: Raw-material price volatility and feedstock availability are prompting automotive OEMs and tier suppliers to revisit source strategies, material choices and inbound inventory models.

Car Bumpers Market

Aftermarket resilience: While new-vehicle cycles moderate, aftermarket and replacement segments continue to provide a predictable revenue pool—attractive to manufacturers and distributors looking to offset OEM cyclicality.

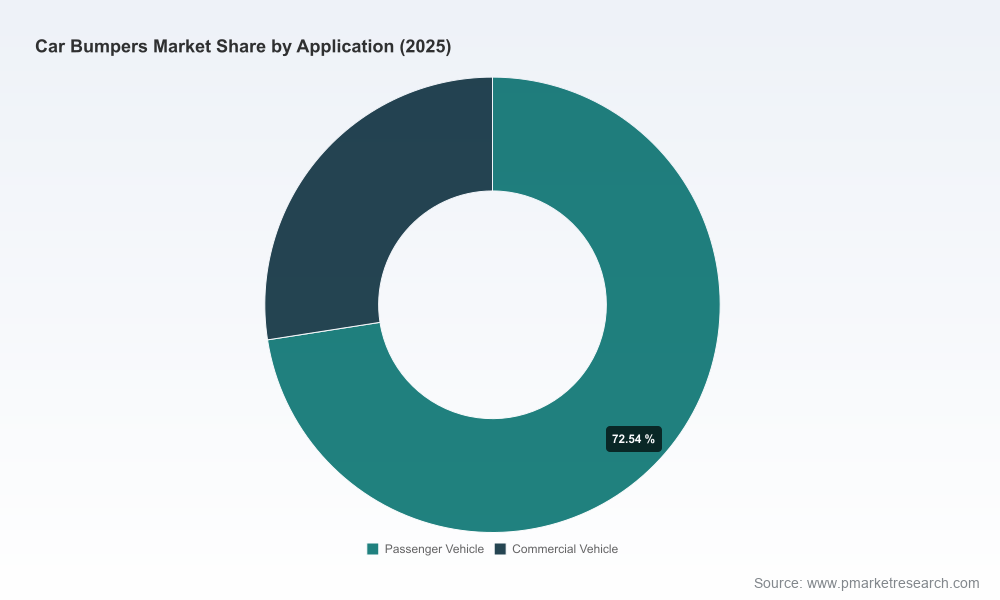

Translating macro trends into commercial impact: the global car bumpers market expanded from roughly USD 14.1 billion in 2020 to USD 16.5 billion in 2025. Under PW Consulting’s central-case scenarios, the market grows to about USD 16.7 billion in 2026 and continues to increase to just over USD 22.0 billion by 2032, reflecting a 4.2% CAGR for the forecast period. These headline figures mask differentiated dynamics underneath—material substitution, regional vehicle parc evolution and aftermarket penetration all create pockets of higher and lower growth that will substantially affect mid‑market and niche players.

Material economics and lightweighting: Polypropylene remains the dominant bumper polymer—used in the vast majority of modern bumpers due to its low density and impact resistance. Recent feedstock cycles have driven short‑term price relief in regions like Northeast Asia, easing immediate cost pressures for OEMs and converters. However, the long-term premium for low‑emission and recyclable formulations is widening, creating opportunities for specialty resins and hybrid material solutions.

Regulatory and circularity push: European-level policy options released in late‑2025, together with local landfill bans in select geographies, are turning recyclability from a “nice‑to‑have” into a procurement criterion. Companies that can demonstrate closed‑loop material credentials or offer validated recycled‑content bumpers will have a competitive edge in several priority markets.

Aftermarket and specialty demand: The aftermarket remains a strategic hedge. Demand for painted, CAPA‑style and heavy‑duty steel bumpers—particularly in light truck and SUV segments—continues to attract dedicated manufacturers and niche aftermarket platforms targeting vehicle personalization and utility use cases.

Vertical displacements and service models: Recycling initiatives and remanufacturing pilots are enabling new service models—repair‑and‑return programs, take‑back schemes and retrofit offerings—that alter lifetime economics and customer lifetime value (CLV) calculations for OEMs and distributors alike.

The market concentration is meaningful: the top three players account for nearly half of the market by revenue, and the top five approach three‑quarters of share, signaling both scale advantages and acquisition opportunities for mid‑tier suppliers. Against this backdrop, a diverse set of companies is carving differentiated positions:

Buckstop Truckware (Prineville, Oregon) — A focused producer of heavy‑duty steel bumper assemblies and winch bumpers for trucks and SUVs. Their recent facility relocation (completed in mid‑2026) underscores an operational scaling move designed to capture aftermarket and regional fleet opportunities where robust, plated steel solutions remain preferred.

Expedition One (Ogden, Utah) — Specialist in precision‑built 4x4 off‑road bumpers and overland accessories. Their value proposition is built on modularity, fitment breadth and brand cachet among enthusiast communities—attributes that translate to stronger aftermarket margins and resilient demand even in softer new‑vehicle cycles.

Fab Fours (Lancaster, South Carolina) — Premium domestic manufacturer of steel truck and SUV bumpers and accessories. Their “made in USA” positioning and product breadth make them a natural partner for retailers and distributors targeting premium restoration and enhancement segments.

Partify (Warren, Michigan) — A supplier of painted auto body replacement parts with CAPA/OEM‑style offerings and lifetime warranties. Their strengths lie in supply chain integration with collision repair networks and warranties that reduce consumer resistance to aftermarket parts.

Operational moves: Buckstop’s facility relocation signals capacity and logistics optimization that will matter for short lead‑time aftermarket programs.

Recycling programs: Initiatives by material processors to collect and reprocess end‑of‑life polymer bumpers are beginning to create upstream feedstock pools of recycled PP, lowering the effective cost of recycled content for converters and raising the bar on traceability and quality assurance.

Policy nudges: Public sector analysis and municipal bans are increasing the financial and reputational downside of inaction on bumper recyclability, especially for companies operating in or exporting to regulated jurisdictions.

Reframe procurement into a resilience question: Locking in material supply is no longer only about price. Procurement leaders must balance feedstock predictability, recycled‑content certification and supplier decarbonization commitments. This will likely reweight supplier selection models away from lowest unit cost toward total cost of ownership (TCO) and compliance risk.

Pursue targeted M&A and JV options: Given the market’s mid‑to‑high concentration and the push toward recycling and specialized aftermarket products, acquisitions of converters with validated recycled‑content capabilities or aftermarket brands with strong channel access can be accretive both to margin and growth.

Differentiate through service and assurance: Warranty and fitment guarantees, repair‑and‑return logistics, and validated recycled content traceability are practical differentiators that align with fleet, OEM, and insurer buyer preferences.

Test hybrid material architectures at pilot scale: Where aluminum and composite bumpers make sense for premium applications, pilots should focus on manufacturability, repairability and downstream recyclability to avoid stranded assets and warranty liabilities.

Our Car Bumpers Market report is designed as a decision‑ready toolkit for 2026 strategy cycles. The deliverables include granular market sizing and scenario-based forecasts, regional and application segmentation (presented with interactive dashboards), a raw‑material cost model linked to polypropylene and alloy price scenarios, supplier heatmaps, technology adoption curves, and a deal pipeline that identifies high‑probability M&A and partnership targets. Importantly, the report couples quantitative models with implementation playbooks—commercial frameworks, procurement RFP templates, and a three‑stage roadmap for transitioning to higher recycled content without undue supply risk.

Quarterly planning: Incorporate our TCO model into vendor negotiations to evaluate recycled‑content premiums versus long‑term compliance risk.

Product roadmaps: Identify two candidate platforms for material substitution pilots—one aftermarket and one OEM—to validate manufacturing readiness and warranty exposure within 12 months.

M&A screening: Use our heatmaps to shortlist acquisition targets that close capability gaps—recycling capacity, aftermarket retail presence, or specialty steel fabrication.

Stakeholder alignment: Brief procurement, product engineering and sustainability teams with our scenario decks to align capital allocation with policy‑driven risk windows.

Our multidisciplinary team combines automotive engineering, polymer economics and corporate strategy to translate headline forecasts into executable actions. We provide not only a precise view of market size and growth—grounded in data from 2020 through our 2025 base year and extended across 2026–2032 under multiple scenarios—but also the operational and commercial playbooks that turn insight into measurable business outcomes.

We deliberately present this article as a focused briefing: it showcases the report’s analytical depth while withholding proprietary segment breakdowns, scenario matrices and company‑level revenue tables that are included in the full study. For procurement scorecards, the interactive supplier map and the step‑by‑step recycled‑content transition plan, please contact PW Consulting or visit our report page to access the complete Car Bumpers Market research suite.

For detailed analysis of this topic, please visit the official page:Car Bumpers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com