Video Intercom Devices and Equipment Market — Strategic Preview for 2026 Decisions

As PW Consulting’s Senior Strategy Consultant and Chief Industry Analyst, I present a concise yet strategically rich preview of our new Video Intercom Devices and Equipment Market study. This is a “trailer” — designed to demonstrate the analytical depth and decision-grade framing embedded in the full report, while intentionally withholding granular segment returns and regional line items to guide commercial, procurement, and corporate development teams to the source for full licensing.

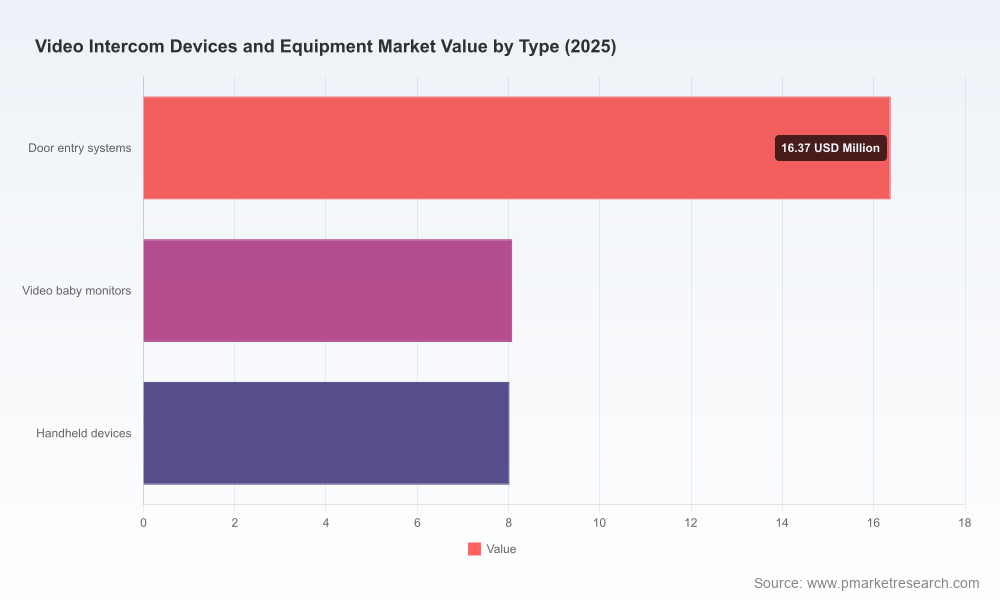

Video Intercom Devices and Equipment Market

Executive snapshot: why this market matters in 2026

Video intercoms have evolved from point products at doorways into software-defined components of building security and occupant experience layers. The market has shown resilient expansion through the pandemic recovery and enterprise digitalization waves: total industry revenues rose materially from the early 2020 base and, with a 2026–2032 forecast underpinned by a 12.45% compound annual growth rate (CAGR), are projected to more than double over the next seven years. This trajectory makes the category a must-watch for security integrators, real-estate owners, smart-building platforms, and cloud infrastructure investors planning capital allocation in 2026.

Video Intercom Devices and Equipment Market

What decision-makers will gain from deploying this intelligence

- Investment prioritization: quantitative growth paths and scenario-tested returns to guide CAPEX and M&A stakes.

- Procurement timing: supplier roadmaps and regulatory overlays that affect total cost of ownership (TCO) across cloud and on-premise architectures.

- Go-to-market plays: product-positioning, channel incentives, and partnerships tailored to the multi-ecosystem nature of modern deployments.

Market trajectory — a data-driven high-level view

The industry has moved from niche hardware to integrated hardware + software platforms. Our base-year analysis (2025) captures this inflection: the installed base and recurring cloud services now constitute a larger share of supplier economics than in 2020. The forecast to 2032 anticipates sustained double-digit growth — a signal that buyer budgets and technology adoption reinforce each other, with cloud-native offerings, AI-enabled features, and multi-tenant solutions serving as the principal accelerants.

Video Intercom Devices and Equipment Market

Importantly, market concentration is moderate. The top three vendors account for a meaningful but non-dominant share of category revenues, and the top five widen that share further — creating an oligopolistic dynamic where emergent specialists can still carve growth through differentiated software experiences, verticalization, or unique integration offers.

Technology and product dynamics to watch

- Cloud-first vs. hybrid deployments: Cloud services unlock feature velocity (mobile directories, live translation, remote provisioning) but expose buyers to energy, data-center, and policy risk; hybrid systems remain strategically attractive in energy-constrained or regulated facilities.

- AI and analytics: Face, voice, and behavior analytics — and emergent deterrence modes — are moving from experimental to productized capabilities; vendors that operationalize these with a clear privacy and governance model will command premium pricing.

- SIP/IP convergence: SIP-native and IP-based intercoms ease integration with unified communications and access control stacks, raising switching costs for platform-committed customers.

- Install model innovation: “No-wiring” and mobile-only provisioning approaches reduce deployment friction in retrofit and multifamily projects, accelerating addressable market velocity for wireless-enabled vendors.

Competitive landscape — positioning and strategic moves

The market features a mix of long-established hardware specialists, fast-growing cloud-native entrants, and platform-focused integrators. Several archetypes emerge:

- Heritage hardware specialists expanding into cloud management — exemplified by firms that pair legacy intercom product lines with new remote management services.

- Cloud-native disruptors targeting multifamily and commercial retrofit projects with low-install friction and subscription economics.

- Security-platform integrators that bundle intercom, camera, and access-control services into an enterprise-grade security stack with centralized analytics.

Representative players and strategic postures we analyze in the full report include:

- Aiphone — leveraging cloud remote management to transition long-standing hardware credibility into service-led value.

- ButterflyMX — a mobile-first, low-install friction model that accelerates adoption in multifamily and commercial retrofit segments.

- Verkada — integrating camera, access, and AI with rapid feature releases (e.g., AI deterrence and live translation) to target enterprise accounts.

- AXIS, DoorBird, 2N, Comelit, Mircom — each pursuing IP-native or hybrid pathways to serve distinct verticals from residential to critical infrastructure.

- Hikvision and Dahua — broad product portfolios and scale are tempered by procurement restrictions in certain markets, creating both channel limitations and opportunity vectors for alternative suppliers.

Recent product activity underscores vendor competition on several fronts. For example, AI-driven communication features and translation capabilities announced in early 2026 signal product maturity and differentiation shifting toward software experiences rather than purely hardware specs. Integration modules enabling third-party access-control compatibility expand addressable enterprise opportunities and reduce end-customer friction.

Regulatory, supply-chain and infrastructure implications

Regulation and infrastructure policy are now central strategic variables — not peripheral compliance checkboxes. The most consequential dynamics we model for 2026 decisions include:

- Procurement restrictions: Certain vendors face explicit bans from U.S. federal procurement, reshaping vendor eligibility and long-term roadmap choices for multinational integrators and public-sector projects.

- Data-center energy and reporting mandates: New EED obligations in Europe and state-level requirements in the U.S. force providers of cloud-managed intercom services to disclose and optimize power and water footprints — altering supplier selection criteria for environmentally conscious customers.

- Local infrastructure rules: Jurisdictions requiring long-term power purchase agreements or cost-shift transparency for high-load data centers create additional contractual and financial complexity for platform operators relying on cloud infrastructure.

- Component volatility: Upstream volatility in LCD panels, cameras, and plastics is producing 15–20% swings in component cost lines; suppliers are responding with product modularization, hedging, and selective vertical integration strategies.

These forces converge to make vendor due diligence indispensable. Procurement teams should request not only product specs but also supply-chain resilience plans, regulatory compliance attestations, and long-term service-level commitments tied to energy or data-location constraints.

How the PW Consulting report supports executable choices

Our full study is built as a practical playbook for 2026 decision-makers. Highlights include:

- Market sizing and forward-looking scenarios calibrated to technology adoption curves and policy pathways, enabling NPV and IRR calculations for product and platform investments.

- Go-to-market blueprints for vendors and integrators, including channel economics, go-live checklists for multifamily/commercial verticals, and pricing-levers analysis for subscription offers.

- Vendor benchmarking and product scorecards that evaluate integration readiness, cloud capabilities, AI maturity, and compliance posture — essential for procurement RFP structuring.

- Deployment playbooks that map OPEX impacts (cloud, connectivity, energy) and CAPEX trade-offs (on-premise vs hybrid architectures) over realistic lifecycle horizons.

- Regulatory and energy risk matrixes tied to regional policy scenarios — enabling strategic hedging and procurement timelines that minimize rework and sunk costs.

- M&A and partnership opportunity maps that identify bolt-on adjacencies (analytics, access control, property management systems) with modeled returns and integration complexity ratings.

Immediate actions for executives and buyers

- For security and facilities leaders: start supplier pre-qualification that includes energy and data-center risk disclosures, not just feature checklists.

- For integrators: re-evaluate pricing models to incorporate recurring software revenue, lifecycle maintenance, and energy-compliance services.

- For investors and corporate development teams: prioritize targets with differentiated software stacks, robust integration APIs, and defensible route-to-market in regulated public-sector channels.

Next step — how to get the full strategic playbook

This preview demonstrates the analytical scaffolding and decision-oriented outputs embedded in PW Consulting’s full Video Intercom Devices and Equipment Market report. The comprehensive study contains the granular segment economics, regional splits, vendor revenue shares, and executable templates that enterprise buyers, integrators, and investors must have to act with confidence in 2026.

For executive summaries, scenario models, or to license the full report and supporting datasets, please visit our research page. Access will provide the detailed segmentation and vendor-level figures that we intentionally leave out of this preview to preserve the “trailer” effect — you will receive the full evidence base and implementation playbooks needed to convert insight into action.

— PW Consulting, Industry Analysis Team

For detailed analysis of this topic, please visit the official page:Video Intercom Devices and Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com