Caravanning Market Trends Accelerating Luxury Travel Experience and Digital Transformation in RV Industry

Other |

2026-05-30 06:03:34

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present this executive primer to orient C-suite leaders, investors, and corporate strategists to the strategic choices that will define performance in the Waste Treatment Disposal market through this decade. Our full market study (base year 2025) models the sector across a seven-year forecast window (2026–2032), quantifying a compound annual growth rate (CAGR) of 5.98% and projecting total market expansion from a 2025 base to nearly USD 1.98 trillion by 2032. This primer explains why those headline numbers matter to 2026 decision-making — and what to prioritize now to capture disproportionate value.

Waste Treatment Disposal Market

Macro growth momentum: A sub-6% CAGR compounds into materially larger addressable opportunities for firms who align capacity and services to evolving demand drivers (infrastructure spending, regulatory updates, and corporate circularity commitments).

Waste Treatment Disposal Market

Regulatory recalibration: Recent and pending regulatory changes (EPA capacity assessments, permit model updates, and compliance deadline adjustments) create both risk and optionality for operators — especially those exposed to hazardous streams and combustion residuals compliance.

Waste Treatment Disposal Market

Industry consolidation and capability build-out: A flurry of strategic transactions and asset-level acquisitions has shifted competitive positioning in the U.S. hazardous and regulated waste space, altering national footprint and processing capacity maps.

Technology and circularity pressure: Accelerating investments in recycling, resource recovery, and alternative treatment technologies are changing lifecycle economics for waste producers and service providers alike.

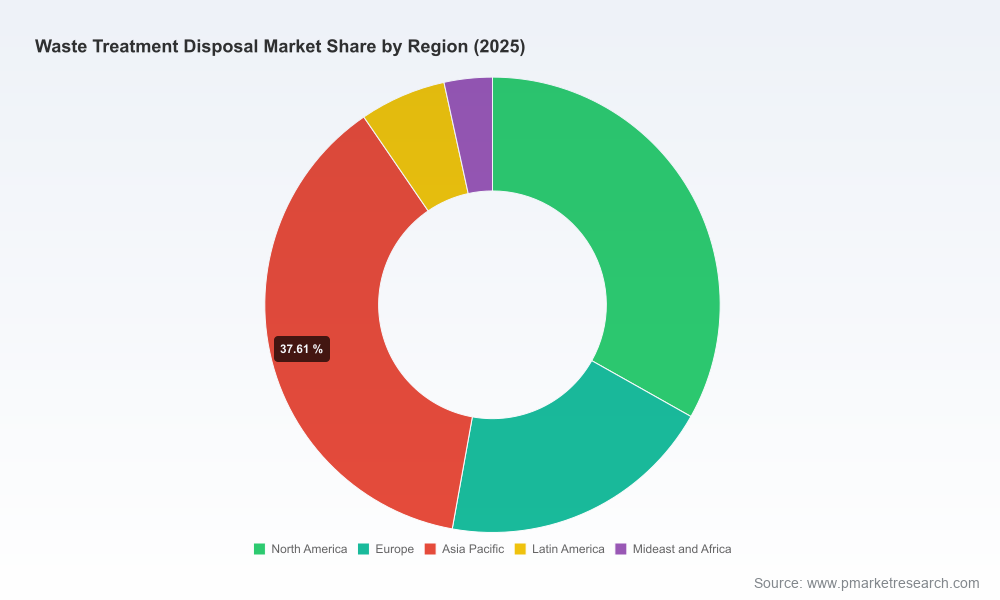

Our modeled market captures historical performance (2020–2025) and projects forward to 2032. At the aggregate level, the market is robust and growing: the 2025 base sits above the trillion-dollar scale and, under our base-case assumptions, expands to roughly USD 1.98 trillion by 2032 at a 5.98% CAGR. That trajectory reflects combined demand from municipal, industrial, hazardous, and specialty streams as well as service mix dynamics across collection, treatment, disposal, and resource recovery.

We stress-tested this baseline across conservative and upside scenarios to reflect regulatory shifts, large-scale infrastructure grants, and potential capacity shocks. Even under constrained scenarios, the market remains sufficiently large that strategically positioned firms can realize attractive returns through targeted investments, partnerships, and disciplined M&A.

Regulatory context: The U.S. EPA’s 2024 National Capacity Assessment and subsequent communications indicate adequate national hazardous waste treatment capacity through 2049 — a signal that near-term capacity scarcity risk is moderated, but that regional mismatches, permit timetables, and specialized stream bottlenecks will continue to create localized premiums. The EPA’s updates to RCRA model permit conditions and the proposed extensions for certain coal combustion residuals deadlines create a shifting compliance horizon firms must incorporate into their project and contract planning.

Infrastructure funding and recycling push: Federal grant programs and IIJA-related initiatives are accelerating investments in recycling and reuse infrastructure. This elevates the strategic importance of integrated service offerings that can capture higher-value recovered materials and reduce reliance on disposal revenue over the long term.

Demand composition: While aggregate growth is meaningful, the composition of that growth is changing — with rising attention on regulated medical and pharmaceutical streams, specialty hazardous waste, and electronic waste. These streams carry higher regulatory and service complexity and therefore higher margin potential for capable providers.

Operational convergence and capacity optimization: Recent transaction activity shows market leaders are expanding through targeted acquisitions that bring operating permits, incineration capacity, and regional logistics advantages. For many buyers, acquiring operating permits and licensed treatment assets is the fastest path to scale.

The market remains moderately fragmented — our concentration metrics indicate that the top three players account for less than one-fifth of market revenue, while the top five combine for roughly a quarter. That structure creates space for national champions to scale while leaving niches for regional specialists and service-focused challengers.

Veolia: Aggressive inorganic expansion in the U.S. hazardous space has reshaped Veolia’s North American positioning. Recent acquisitions (portfolio of regional hazardous specialists and a follow-on transformational deal announced in late 2025) materially increase permitted capacity and incineration capability — a strategic move to capture regulated waste flows and integrated treatment contracts.

Waste Management, Inc.: Post-acquisition integration of regulated medical and pharmaceutical disposal services strengthens WM’s end-to-end regulated waste offering and extends its route-to-market for specialty services. WM is leveraging scale to cross-sell higher-value compliance and treatment solutions into existing municipal and commercial accounts.

Republic Services and REMONDIS: Both players continue to emphasize integrated municipal and resource-recovery solutions, pursuing portfolio optimization and selective capacity investments to defend municipal solid waste volumes while growing recycling and recovery services.

SUEZ and REMONDIS (European incumbents with U.S. activity): These firms focus on combining water and waste service capabilities, aiming to win large industrial and municipal contracts where bundled service models provide competitive differentiation.

Clean Harbors and Triumvirate Environmental: Specialists in hazardous and industrial streams, these firms are executing bolt-on acquisitions to expand treatment footprints and compliance service breadth — consistent with the market trend favoring regulated-capable operators.

Stericycle (now integrated under WM’s healthcare solutions): The integration consolidates regulated medical waste expertise into a scaled provider, improving negotiating leverage with healthcare systems and pharma clients.

Consolidation for permit and capacity: Buyers are prioritizing acquisitions that deliver operating permits, incineration or specialized treatment assets, and local market control. These are value-creating when they reduce transportation costs, shorten lead times for regulated streams, and enable integrated service offers.

Scale plus specialization: Transactions show a two-track strategy — national players adding specialty capability and regional players consolidating adjacent service territories. Expect continued small-to-medium bolt-ons alongside occasional transformational deals.

Capital deployment discipline: Given the relative fragmentation, disciplined buyers will win — those who integrate acquired assets to drive operational synergies and cross-sell higher-margin services.

Our full study combines strategic narrative with highly actionable tools for decision-makers. Highlights include:

A reproducible market-sizing model (2020–2032) with scenario toggles for regulatory tightening, capex cycles, and recycling-adoption curves.

A regulatory tracker mapping likely permit, compliance, and reporting changes through 2030 and their expected impact on regional capacity and operating costs.

Detailed competitive dossiers covering strategy, footprint, key assets, and M&A pipelines for the leading players and relevant regional specialists.

Transaction playbook and valuation benchmark for M&A — including multiples by asset type, integration checklist, and repurchase/retention considerations for workforce and permitting continuity.

Investment cases and capex prioritization framework that translate market growth and scenario stress tests into actionable spend portfolios and expected payback ranges.

Commercial go-to-market templates for selling integrated waste + recycling solutions to municipal, healthcare, industrial, and energy clients.

Prioritize permit-light capacity augmentation in regions where logistics costs drive margins today, and pursue permit-rich acquisitions selectively to lock in regulated flows.

Integrate recycling and recovery pathways into legacy disposal businesses to capture margin uplift from secondary materials and to hedge disposal-volume downside.

Embed regulatory scenario planning in capital-allocation routines. Shorten capital approval timelines for modular, scalable treatment assets that can be deployed as compliance windows crystallize.

Invest in digital route optimization and asset monitoring to lower operational costs and improve permit compliance reporting — small efficiency gains compound at scale.

Design M&A diligence around permit portfolios and workforce continuity: the value of an acquired business often lies in its licensed permits and the trained operating teams that preserve them.

This primer intentionally emphasizes strategic context and headline market metrics while withholding granular regional and application-level splits, unit-level pricing, and proprietary segmentation detail. That granularity is core to tactical execution — influencing customer targeting, pricing strategy, and site-level capex decisions — and is available in the full report and underlying datasets. Our approach follows a “trailer” principle: provide enough insight to shape strategic direction, but require engagement for the operational blueprints that enable execution.

Board-level briefings: Use the headline growth profile and scenario outputs to test existing five-year plans for headroom and downside resilience.

M&A screening: Leverage our competitive dossiers to create a target shortlist and apply the report’s valuation benchmarks in initial offer modeling.

Capex reallocation: Apply the investment prioritization framework to 2026 budgets to accelerate modular, permit-accretive projects where internal rates of return exceed peer comparables.

Regulatory preparedness: Adopt the regulatory tracker into compliance roadmaps to anticipate permit windows and potential funding opportunities from federal programs.

For full access to the dataset, regional and application-level segmentations, company profiles, and executable playbooks, PW Consulting provides the complete Waste Treatment Disposal Market report and workshop packages. Those materials translate the macro view above into targeted initiatives you can operationalize in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Waste Treatment Disposal Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com