The Role of Subdivision Surveys in Edmonton in Managing Land Expansion Projects

Other |

2026-05-23 09:50:41

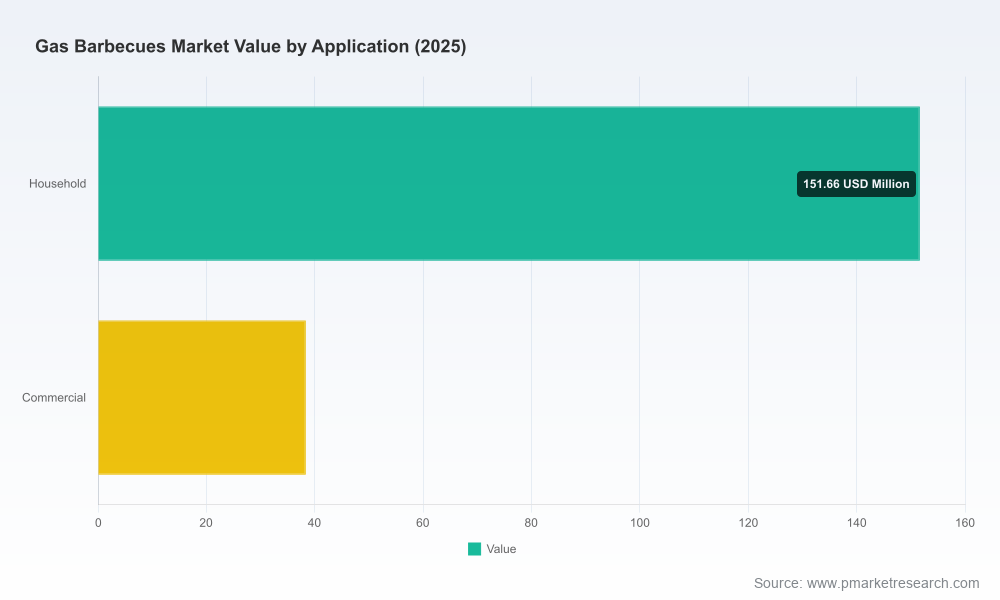

As companies finalize budgets and strategic plans for 2026, the gas barbecues market presents a distinct mix of steady expansion, concentrated supplier power, and pockets of technological and regulatory disruption. PW Consulting’s new market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes quantitative forecasts with practical go-to-market and product strategies designed for leadership teams intent on converting market growth into durable margin and share gains. The headline: the global market grew from approximately USD 153.0 Million in 2020 to USD 190.0 Million in 2025, and our mid-case projects compounded annual growth of about 5.1% across 2026–2032, reaching roughly USD 269.0 Million by 2032.

Gas Barbecues Market

Timing: 2026 is a hinge year — manufacturers are moving from incremental product updates to embedded connectivity and outdoor-kitchen ecosystems. Decisions taken in 2026 (capacity, premium/upstream investments, channel alignments) will determine who captures the higher-margin expansion through 2032.

Gas Barbecues Market

Risk calibration: Inflation, input-cost dynamics for stainless steel, and evolving fire-safety regulations mean that nominal demand growth will not translate one-for-one into margin growth. Our research decouples volume, ASP, and cost-to-serve so leaders can stress-test portfolios against three realistic scenarios.

Gas Barbecues Market

Market structure: The market shows meaningful concentration — our analysis indicates a CR3 of ~65% and a CR5 near 80% — which amplifies the effect of strategic moves by leading OEMs and creates both barriers and levers for challengers.

Demand composition: Consumer demand remains anchored in residential upgrades and outdoor-living trends, with commercial procurement steady but more cyclical. Premiumization is a persistent theme: buyers are trading up to higher-spec stainless systems and integrated outdoor-kitchen solutions.

Technology and features: Expect a sharper bifurcation between commodity freestanding grills and feature-rich built-in systems. Connectivity (Wi‑Fi/Bluetooth), precision ignition/temperature control, and hybrid fuel solutions are moving from differentiators to expected features in higher tiers.

Input and compliance pressures: 304 stainless steel continues to dominate as the preferred construction material for durability and heat tolerance, keeping material-cost sensitivity front-and-center. Meanwhile, regionally specific safety regulations — for example, state-level adoptions of NFPA-based fire-safety rules and local permitting regimes for gas appliances — introduce non-uniform compliance costs that should be modelled into 2026 capex and operating plans.

The market is led by several established players that combine brand equity with diversified channel footprints and product breadth. Each incumbent pursues different vectors of advantage:

Weber Inc. (Chicago, IL) — a leading manufacturer with iconic Spirit and Genesis lines; recent product cadence includes a 2025 Spirit refresh and a 2026 launch of smart-enabled Genesis and Spirit models integrating Wi‑Fi/Bluetooth and the Weber Connect ecosystem. Weber’s playbook emphasizes platform upgrades and U.S.-based manufacturing credibility.

Coleman Company (Wichita, KS) — positions on portability and value, with a focus on outdoor-recreation segments that require lightweight, portable gas grill solutions.

Bull Outdoor Products (Grand Rapids, MI) — targets the premium outdoor-kitchen segment with high-spec gas grills and accessory ecosystems that lock in higher ASPs and aftermarket spend.

Char-Broil LLC (Columbus, GA) — leverages technology such as proprietary flavor systems and a broad performance-series lineup to defend mid-market share.

Masterbuilt Grills (Columbus, GA) — combines multi-fuel portfolios with an emphasis on accessible innovation and retail distribution strength.

Onward Manufacturing (Canada), Lynx Grills, Traeger, and Napoleon Products — each plays a distinct role from high-end outdoor kitchens to hybrid pellet-gas platforms and aggressive promotional activity; Napoleon’s recent seasonal push underlines the importance of timed marketing and promotional cadence.

These firms collectively shape pricing, feature expectations, and distribution norms. The concentration statistics imply that a handful of strategic moves — new platform launches, channel consolidations, or aggressive margin plays — can materially re-shape competitive economics in short order.

Regulatory overlay: Several jurisdictions now reference NFPA editions for fire-safety minimums as they relate to gas appliances, and local utilities/authorities (for example, municipal gas-inspection policies) are tightening permit and inspection requirements for installed outdoor grills. For manufacturers and channel partners, this increases the value of compliance documentation, field-installation support programs, and certified installer networks.

Materials strategy: 304 stainless steel remains the default for mid-to-high tiers. Hedging strategies for stainless input costs, supplier diversification, and design choices that reduce stainless mass without sacrificing perceived quality are high ROI areas to pursue in 2026.

Aftermarket and service: As installations become more regulated, bundled service agreements and certified maintenance plans represent a defensible margin stream — particularly for built-in and premium models that require professional installation and periodic inspection.

Proprietary demand model with annualized forecasts across 2026–2032, scenario stress-testing, and sensitivity to ASP, input-cost inflation, and regulatory cost passthroughs.

Supply-chain mapping and cost-to-serve profiles by channel (retail, specialty, online, commercial), including build-versus-buy decision frameworks for key components and options for nearshoring/dual-sourcing.

Commercial playbooks: product roadmaps, pricing ladders, promotional calendars, and channel incentive structures tailored for both incumbents and challengers.

Detailed competitive benchmarking: product-feature matrices, technology adoption timelines, and M&A play scenarios focused on bolt-on acquisitions and capability buys.

Regulatory and installation risk registers by market, plus recommended compliance and installer-partner strategies to reduce time-to-revenue for built-in systems.

Investor-focused chapter: valuation-impact analysis under alternate market-growth and margin assumptions, useful for private-equity due diligence and corporate development teams.

Note: in keeping with the “trailer” purpose of this preview, we summarize directional insights here but withhold granular subsegment revenue splits and region-by-channel detail that are central to competitive moves and M&A diligence. The full dataset and model access are available on the report landing page.

Prioritize connectivity where it creates platform lock: For premium and upper-mid tiers, embed Wi‑Fi/Bluetooth and a serviceable ecosystem (apps, recipe/assist features, remote diagnostics). Our adoption curves show accelerating consumer willingness to pay for integrated experiences.

Re-evaluate channel economics: Online and direct-to-consumer sales reduce some downstream costs but raise installation and returns complexity. Hybrid channel approaches, with certified local installers and bundled warranties, mitigate friction for built-in systems.

Hedge materials strategically: Negotiate multi-year contracts on stainless and component forgings, and explore design optimizations that reduce stainless usage without compromising perceived quality. Small gains in material efficiency rapidly compound at scale.

Monetize services: Introduce certified installation programs, extended warranties, and periodic inspection subscriptions, especially in jurisdictions with stricter permitting regimes. These convert one-time sales into recurring revenue and improve customer retention.

Use promotional cadence as a defensive lever: As competitors roll product refreshes and seasonal promotions (e.g., Napoleon’s summer programs), align product launches with promotional windows and inventory-readiness to avoid margin-leak during peak buying seasons.

Assess M&A for capability vs. scale: Target acquisitions that bring service networks, connectivity platforms, or specialty manufacturing capabilities rather than only volumetric scale — these assets have higher value in a concentrated market where differentiation is key.

This article is designed to orient executive teams and corporate development groups to the high-impact issues shaping 2026 decisions. For product leaders, our product-feature timelines and customer willingness-to-pay analysis will sharpen roadmaps. For operations and procurement, our cost-to-serve and input-cost sensitivity modules provide actionable levers for margin protection. For strategy and M&A teams, the full competitive benchmark and scenario-model will quantify deal rationale and integration priorities.

To access the detailed models, subsegment breakouts, regional channel economics, and the full competitive dataset (including product-level feature matrices and timelines), please consult the full PW Consulting Gas Barbecues Market report. The granular intelligence and downloadable model are specifically designed to support budgeting, product planning, and transaction due diligence for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Gas Barbecues Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com