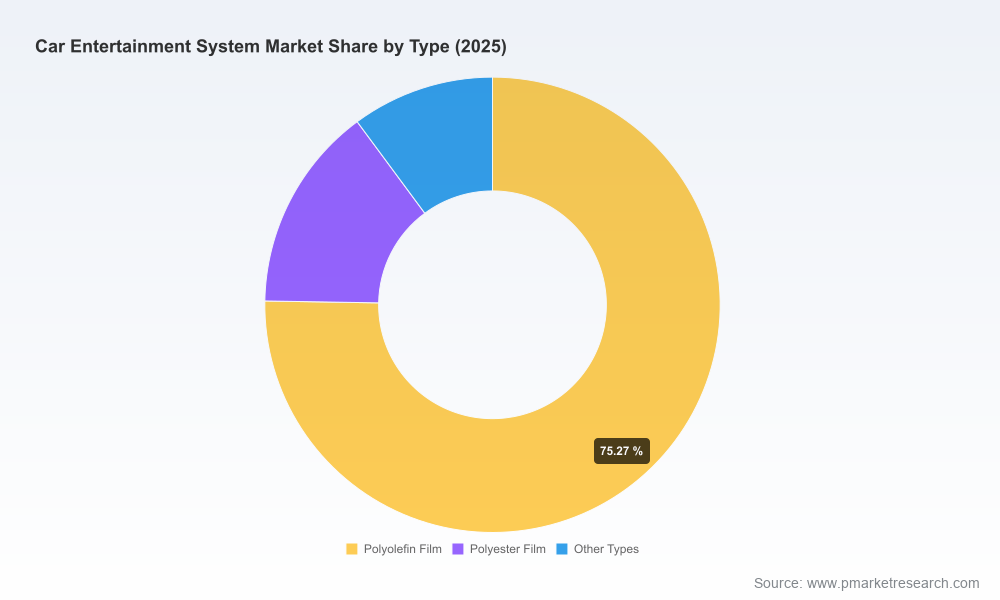

Car Entertainment System Market — 2026 Strategic Preview

As global mobility redefines the in-cabin ecosystem, the Car Entertainment System market is entering a decisive phase for corporate strategy. PW Consulting’s latest industry briefing frames that inflection: after rising from roughly USD 163.2 Million in 2020 to USD 215.0 Million in our 2025 base year, the market is forecast to expand at a compound annual growth rate (CAGR) of 6.98% through the 2026–2032 horizon, reaching an estimated USD 345.4 Million by 2032. For leaders planning 2026 investments, product roadmaps, and M&A activity, this trajectory creates both opportunities and time-sensitive risks. This preview outlines the strategic value of our full study and the highest-impact decisions our analysis supports.

Car Entertainment System Market

Why this study matters for 2026 decision-makers

- Capital allocation under acceleration: Moderate, sustained growth means decisions taken in 2026 will compound materially across the forecast window — influencing platform selections, R&D prioritization, and partnership economics for the rest of the decade.

- Platform and software risk: The shift from hardware-centric to software-driven experiences amplifies regulatory, certification, and licensing exposures that can materially affect time-to-market and total cost of ownership.

- Competitive timing: Product feature cycles (spatial audio, HDR in displays, integrated cockpit SoCs) are compressing; first-mover advantage in platform integration and certification can translate into durable OEM relationships.

- Business model pivots: Recurring revenue options (connectivity subscriptions, content partnerships, OTA feature monetization) turn entertainment systems into strategic revenue streams rather than one-time hardware sales.

What the full report delivers (executive summary of scope)

- Market sizing and historical trend analysis (2020–2025), with a transparent forecast model spanning 2026–2032 and scenario variants for high/low adoption pathways.

- Detailed segmentation across product types, application classes, and regional markets, with unit economics and price elasticity models to support pricing and product decisions.

- Supplier scorecards: capabilities, roadmap alignment, integration risk, and M&A suitability for Tier‑1s, semiconductor IP owners, and software platform providers.

- Go-to-market playbooks for OEMs, aftermarket vendors, and software-first entrants, including channel economics and partner selection matrices.

- Regulatory and certification map: testing pathways, compliance timelines, and recommended mitigation strategies for platform-driven risks.

- Operational exhibits: supply-chain bottleneck analysis, component lead-time scenarios, and cost build-ups to model margin sensitivity.

Market dynamics: Drivers, friction points, and inflection events

- Experience-first consumer expectations: Spatial audio, immersive displays, and seamless device convergence are shifting buyer preference from basic infotainment to branded in-cabin experiences. Landmark product introductions in early 2026 — including Dolby Atmos integration into aftermarket receivers and automotive HDR certification — underscore this trend.

- Software-platform consolidation: A growing portion of innovation is occurring at the OS and middleware layer. The industry is responding with standardized testing and certification regimes to tame variability in quality and security; independent labs now play an established role in validating Android Automotive implementations.

- Compute convergence: Suppliers are consolidating infotainment, cluster, and ADAS workloads onto common SoCs, changing supplier bargaining power and elevating software integration as a key differentiator.

- Connected services monetization: OEMs and suppliers are experimenting with subscriptions, content bundles, and data-driven services — converting entertainment systems into long-term customer touchpoints.

- Aftermarket vs OEM balance: Aftermarket innovation remains a testbed for premium audio and spatial features, but OEMs are increasingly integrating equivalent capabilities during platform design, compressing aftermarket room for differentiation.

Competitive landscape — strategic positions and tectonics

The market remains populated by a mix of electronics conglomerates, specialist audio brands, and automotive suppliers. Each player brings different assets to bear: audio IP and brand equity, direct OEM relationships, or systems-integration competencies. Our profiling highlights not just capability, but strategic intent — who is investing in software platforms, who is consolidating supply chains, and who is positioning for recurring revenue.

Car Entertainment System Market

- Harman International (Stamford, CT) — leveraging premium audio heritage into connected-system leadership. Recent certifications and platform moves indicate a clear push to own the in-cabin UX layer and anchor OEM partnerships with validated HDR and spatial solutions.

- Pioneer Corporation (Tokyo) — balancing aftermarket strength with an OEM play; notable for rapid feature-driven product launches that validate new audio formats and user interaction models in real-world settings.

- DENSO TEN Limited (Kobe) — conveys an automotive-first engineering DNA, focused on robust audio-visual and navigation suites designed for integration across vehicle architectures.

- Panasonic Automotive Systems (Yokohama) — pursues premium, integrated infotainment systems, with an emphasis on long-cycle OEM relationships and in-cabin platform continuity.

- Mitsubishi Electric Automotive America (Northville) — targets cockpit integration and rear-seat ecosystems, pertinent for OEMs prioritizing multi-zone entertainment strategies.

- Bosch (Stuttgart) — shifting toward SoC-level consolidation, demonstrated by public integrations combining infotainment and driver-assistance workloads — a development that materially changes supplier architecture roadmaps.

- Continental AG (Hanover) — focuses on information management and connected services, bridging the divide between traditional automotive electronics suppliers and software-centric service providers.

Recent product launches and demos — from HDR certification wins to combined infotainment/ADAS demonstration platforms — are not mere marketing: they are leading indicators of capability migration that will shape supplier selection and OEM platform strategy across 2026.

Car Entertainment System Market

Regulatory and certification headwinds — a practical reality

Software platform certification has transitioned from a best practice to an operational necessity. Third-party laboratories are now standard participants in the Android Automotive certification ecosystem, creating new gatekeepers and timelines that must be budgeted into product cycles. For decision-makers this means: allocate calendar and capital for external validation early; avoid rework by baking certification requirements into system architecture; and consider lab partnerships as part of the vendor pre-qualification process.

Actionable strategic playbook for 2026

- Prioritize platform interoperability over proprietary optimization: Given the increasing role of standardized OS stacks and certification regimes, interoperability reduces integration risk and shortens time-to-market.

- Lock in certification pathways early: Incorporate independent lab testing into product development timelines; certification bottlenecks are a recurring source of launch delays.

- Invest selectively in differentiated UX capabilities: Spatial audio and HDR-capable displays are now meaningful purchase drivers; invest where they map to your target buyer economics.

- Design for over-the-air and service monetization: Treat the entertainment stack as a platform for recurring revenue; map the feature roadmap to identifiable subscription or usage-based models.

- Model supply-chain consolidation scenarios: SoC and component consolidation materially affect cost curves; stress-test sourcing strategies under lead-time and price-volatility scenarios.

- Consider bolt-on acquisitions for software talent: Acquiring middleware or UX teams can be faster and less risky than in-house development when time-to-market is critical.

- Adopt a partnership-first aftermarket strategy: If pursuing aftermarket channels, align product launch calendars with certification milestones and premium content partners to accelerate consumer adoption.

What this preview does not disclose — and why you’ll want the full report

This introductory briefing is intentionally selective: it demonstrates the report’s strategic depth but omits granular segmentation tables, regional and application-level splits, proprietary supplier scoring matrices, and the detailed financial models that power our market scenarios. Those elements include precise unit economics, price elasticity curves, and segment-by-segment revenue trajectories that materially affect investment sizing and go-to-market sequencing. Access to the full dataset and appendices will allow you to build executable business cases and scenario-specific valuations tailored to your organization.

How PW Consulting can support your 2026 agenda

- Custom diligence: carve-outs of target supplier scorecards and integration impact studies for M&A or JV decisions.

- Roadmap alignment workshops: prioritize feature investments and certification timelines to hit revenue inflection points efficiently.

- Commercial modelling: generate subscription economics, partner revenue share frameworks, and break-even analyses under multiple adoption scenarios.

Next steps: Use this preview to align executive debate around the most consequential trade-offs — platform choice, certification investment, and monetization model — then consult the full PW Consulting Car Entertainment System Market Study to convert those strategic choices into executable programs. The complete report includes the full quantitative annex, supplier scorecards, and tactical playbooks essential to making high-confidence decisions in 2026.

For detailed analysis of this topic, please visit the official page:Car Entertainment System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com