EMI Absorber Sheets & Tiles Market 2026: Strategic Imperatives for Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a high-level, decision-focused introduction to our full EMI Absorber Sheets & Tiles Market study. This briefing synthesizes the structural forces, technology inflections, competitive dynamics, and practical playbooks that will determine who wins and why between 2026 and the end of the forecast horizon.

EMI Absorber Sheets & Tiles Market

Executive snapshot

The EMI absorber sheets & tiles market reached approximately USD 778 million in our base year (2025). Our analysis projects a steady compound annual growth rate (CAGR) of 5.1% across 2026–2032, reflecting a mix of incremental demand from consumer electronics refresh cycles, step-changes in automotive electrification and ADAS architectures, and rising EMC compliance complexity as devices push toward higher-frequency operation. By the end of the forecast window, the market is set to cross the USD 1.1 billion threshold, underscoring sustained commercial opportunity for both component suppliers and systems integrators.

EMI Absorber Sheets & Tiles Market

Why this study matters for 2026 decisions

- Timing: 2026 is a pivotal year for capital allocation in EMI materials — design wins secured now shape multi-year revenue streams for materials suppliers and EMS/ODM partners.

- Regulatory inflection: EMC standards and certification regimes continue to tighten across bands up to 10 GHz, making absorber selection and test protocols a core go/no-go consideration for product launches.

- Margin preservation: Raw-material volatility (notably ferrites and conductive polymers) and labor-intensive converting steps mean small design or supply-chain errors amplify into margin leakage.

- M&A and partnerships: The market’s moderate concentration creates attractive tuck-in targets for larger materials houses and strategic buyers seeking market or technical verticalization.

Market dynamics: demand drivers, supply constraints, and risk vectors

Three clusters of dynamics will define competitive outcomes in 2026:

EMI Absorber Sheets & Tiles Market

- Demand-side sophistication: OEMs increasingly require tailored absorber performance across near-field and cavity-resonance scenarios. The consequence is higher value-add in product engineering (laminates, adhesives, die-cut complexity) and growing demand for integrated absorber + adhesive solutions.

- Raw-material and process constraints: Ferrites and conductive polymers represent the bulk of feedstock for absorber production. Price swings in these inputs and the labor/resource intensity of adhesive converting and die-cutting raise the bar for operational excellence and vertical integration.

- Regulatory and safety overlay: Mandatory compliance to EMC performance up to 10 GHz, coupled with RoHS and flame-retardancy requirements (e.g., UL94 V-0), is driving product reformulation and higher certification costs — a barrier for new entrants but an opportunity for incumbents with testing and qualification capabilities.

Technology and product trends

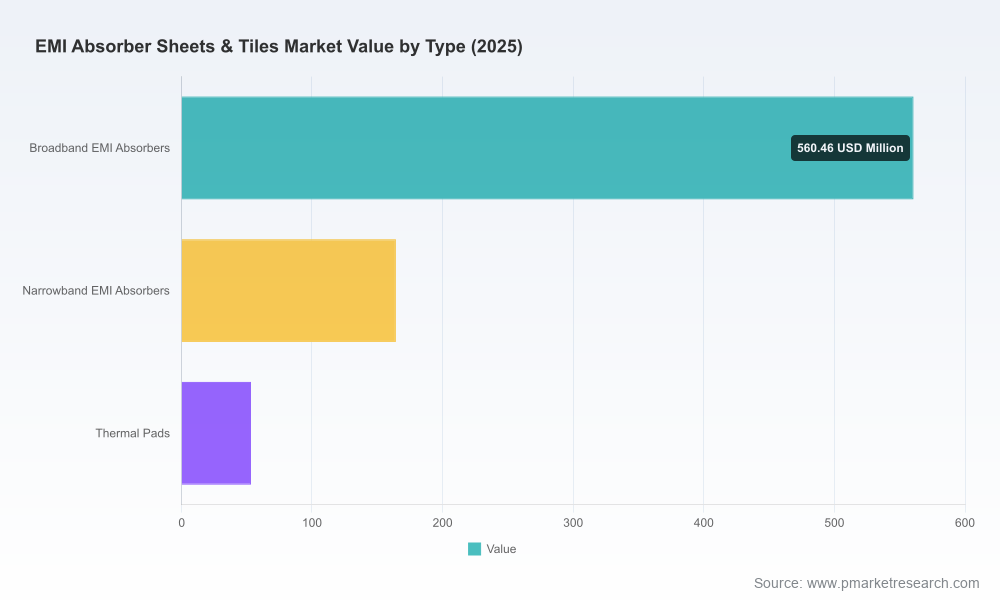

- Broadband vs narrowband differentiation: The market continues to bifurcate between broadband absorbers designed for wide spectral control and narrowband/targeted materials optimized for specific resonance problems. Product roadmaps in 2026 should articulate clear value propositions — cost per square centimeter is no longer the sole KPI.

- Integration of adhesives and films: Suppliers that can deliver absorber + adhesive + flame-retardant film stacks reduce assembly risk for OEMs and command price premiums. Expect partnerships between adhesive specialists and absorber manufacturers to accelerate.

- Thin, conformable formats: As devices shrink and thermal budgets tighten, demand for thin, pliable absorbers and thermal-capable pads will increase. Technical trade-offs between absorptive performance and thermal conduction are becoming a prominent engineering discussion.

- Test-first productization: Modular test protocols and near-field/cavity simulation services bundled with physical samples shorten OEM qualification cycles and become a differentiator in design-win contests.

Competitive landscape — what executives need to know

The competitive structure is moderately concentrated, with the top three players accounting for a significant portion of the market and the top five even more so — creating both scale advantages and acquisition opportunities for midsize players. The leading incumbents exhibit differentiated strategic postures:

- 3M Company (St. Paul, Minnesota) — Strengths: broad product portfolio spanning low-frequency to multi-GHz absorber series and deep channel access in consumer and industrial segments. Strategic focus on system-level solutions and standard compliance positions 3M well for OEM partnerships. Watch for continued investment in certification and application engineering capabilities.

- Laird Performance Materials (United States) — Strengths: thin elastomer absorbers and dispensable absorbers targeted at near-field and cavity-resonance problems. Laird’s advantage is engineering depth in customized form factors and active engagement with EMS partners. Competitive weakness may arise if raw-material costs rise sharply and conversion efficiencies are not improved.

- Fair-Rite Products Corp. (Wallkill, NY) — Strengths: ferrite components and absorber materials with tight integration into absorber sheet offerings. Fair-Rite’s legacy in ferrites gives it sourcing and material science leverage; the company’s updated product catalogues indicate a push into new end-markets like smart homes and medical devices.

- KITAGAWA INDUSTRIES (Japan) — Strengths: specialized ferrite absorbers and a clear focus on EMC applications. Recent catalog updates show a technology refresh that targets both broadband and narrowband needs. Advantage in APAC OEMs and industrial customers.

- Henkel AG & Co. KGaA (Düsseldorf) — Strengths: adhesives and EMI shielding films with scale in automotive electronics. Henkel’s late-2025 product launch highlights a deliberate move to combine cost-effective films with adhesive expertise to address automotive electronics demand.

Recent product updates and catalog releases by Henkel, KITAGAWA, and Fair-Rite illustrate a market in which incumbent suppliers are innovating at the product and go-to-market layers rather than disrupting the basic absorber chemistry. This environment favors buyers who require validated performance and suppliers who can demonstrate workflow compatibility and certification readiness.

Strategic implications & practical playbook for 2026

Executives evaluating strategy in 2026 should prioritize five practical moves. Each move is framed to be executable by procurement, R&D, or corporate development teams within 6–12 months.

- 1) Treat absorbers as system components, not commodities. Define absorber selection criteria that include manufacturability, adhesive integration, certification path, and repairability. Require suppliers to provide validated test protocols and sample-run data as part of RFQs.

- 2) Lock in raw-material options and conversion capacity. Negotiate multi-year supply agreements or dual-sourcing for ferrites and conductive polymers, and evaluate near-shore converting partners to mitigate labor and logistics risk. Small changes in converting yields can have outsized P&L impact.

- 3) Invest in front-loaded qualification. Fund early-stage co-engineering with strategic suppliers to accelerate design wins. Offer to co-fund certification where mutual lift accelerates time-to-market and defensibility.

- 4) Expand product families via modular offerings. Consider a “platform-and-kits” approach: a limited set of certified absorber modules that cover the majority of current use-cases, with add-on modules for edge scenarios (thermal, high-power RF, or unique form factors).

- 5) Use M&A and partnerships strategically. With the market concentration profile that favors scale, buyers with capital should prioritize bolt-on acquisitions that add converting capacity, adhesives capability, or proprietary ferrite grades — not just incremental revenue.

What the full PW Consulting report delivers (operationally focused)

Our comprehensive study goes beyond hypothesis to provide the operational intelligence teams can act on immediately. Highlights include:

- Market sizing and a transparent forecasting model (base year 2025), scenario runs and sensitivity to raw-material and adoption rates.

- Commercial playbooks for procurement and engineering including RFQ templates, supplier scorecards, and cost-to-serve matrices.

- Technical appendix with near-field and cavity-resonance testing protocols, recommended EMC compliance checklists up to 10 GHz, and qualification timelines for common OEM review cycles.

- Supplier diagnostics: strategic profiles, capability heatmaps, and negotiations playbooks for incumbent and challenger suppliers.

- M&A roadmap: target screening criteria, valuation guidance, and integration checklists tailored to absorber-sheet manufacturers and converting specialists.

- Case studies: two anonymized client engagements showing how early co-engineering and procurement redesign shortened qualification from 18 to 9 months and reduced single-source risk exposure.

Final perspective: where companies should place their bets in 2026

The EMI absorber market offers a classic combination of technological nuance and supply-chain leverage: it favors players that can marry material science with operational excellence. For OEMs and tier suppliers, the immediate priority is to convert absorber selection from an afterthought into a defined engineering and procurement pathway. For materials suppliers, the focus should be scaling conversion capability, deepening certification services, and forming alliances with adhesives and thermal-material specialists.

This introduction is deliberately selective — it outlines the strategic map and shows the pathways where value accrues. For the full data, granular segmentation, and executable templates that your teams can deploy this quarter, access the complete PW Consulting market study.

For detailed analysis of this topic, please visit the official page:EMI Absorber Sheets & Tiles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com