Detonator Market 2026 Strategic Preview — What Executives Must Know

Executive snapshot

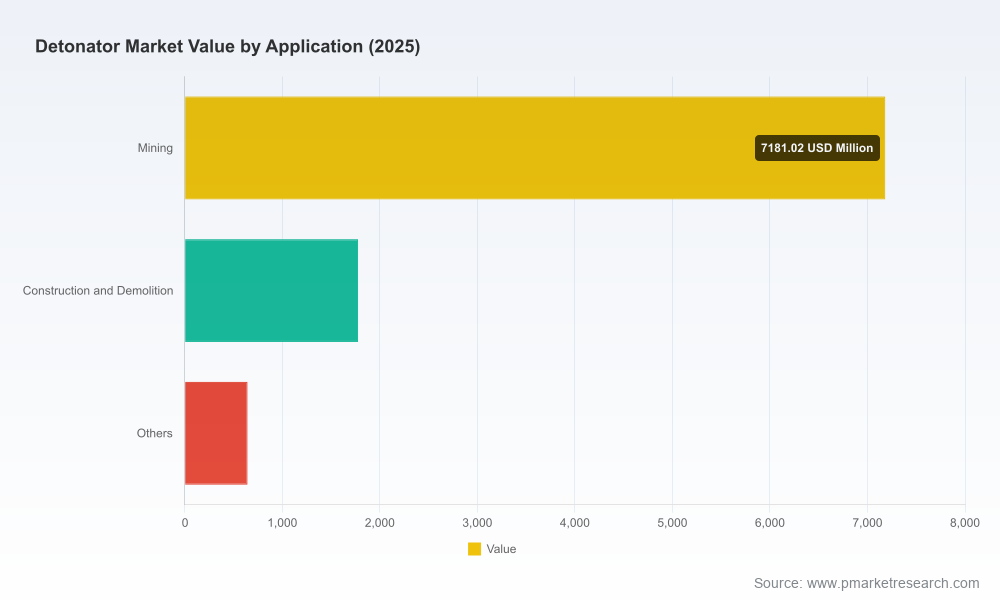

As companies plan capital allocation, procurement strategies, and M&A activity for 2026, the detonator market is moving from a defensive supply-focus to a strategic technology and sustainability play. Our latest PW Consulting Detonator Market study — base year 2025, historical window 2020–2025, forecast through 2032 — quantifies this transition. The global market, measured in USD Million, grew from a 2020 baseline of USD 7,900 Million to USD 9,600 Million in 2025. Under current assumptions, it is projected to expand at a compound annual growth rate (CAGR) of 3.42% across the 2026–2032 forecast period, reaching just over USD 12,000 Million by 2032.

Detonator Market

Why 2026 is a strategic inflection

- Structural growth with tactical inflections — a steady mid-single-digit CAGR masks important shifts: higher-value programmable and electronic initiation systems are rising in commercial and industrial adoption, while regulatory and sustainability pressures are accelerating technology replacement cycles.

- Supply-chain resilience has moved from vendor selection to site strategy. Recent greenfield and retrofit investments by major manufacturers highlight an industry prioritizing redundancy, onshore capacity, and energy efficiency in production.

- Margins and procurement risk are being re-sculpted by material substitution and labor specialization. Lead-free chemistries and precision-timed electronic components change cost structures and sourcing footprints.

Market trajectory — what the numbers hide (and why that matters)

The headline growth trajectory — USD 9.6 billion in 2025 to roughly USD 12.0 billion by 2032 at a 3.42% CAGR — is deceptively neat. Beneath it sits uneven adoption across product classes, accelerating certification-driven replacement in safety-sensitive environments, and pockets of faster-than-average demand tied to large mining investments and defense procurement cycles. For boardrooms and commercial teams, two practical implications follow: first, allocate discretionary capex toward modular, upgradable plant and production systems rather than one-off expansions; second, calibrate commercial offers to account for a bifurcated market where premium, programmable solutions command different contract terms and service obligations than legacy mechanical systems.

Detonator Market

Strategic implications for 2026 decision-making

- Capex and automation: Automated electronic detonator manufacturing and smart assembly lines materially reduce recurring labor exposure and enhance output quality. Recent industry investments demonstrate a clear ROI pathway for integrated automation plus renewable-energy overlays to reduce operating costs and regulatory risk exposure.

- Sustainability and compliance as commercial levers: Lead-free detonator technologies are transitioning from compliance nicety to procurement prerequisite in regulated markets. Certification progress for lead-free offerings and defense-qualification for specialized detonators is reshaping shortlists for large tenders.

- Supply-chain localization: New plants and capacity near end markets mitigate logistics, customs, and single-supplier risk. For buyers, this creates opportunities to negotiate more favourable SLAs and reduce inventory carrying costs.

- Talent and operations: Producing advanced electronic initiation systems requires skilled labor and rigorous quality control. Human-capital investments are now a part of the competitive barrier; firms that secure technical training pipelines and certification regimes will sustain yield and time-to-market advantages.

- M&A and partnership playbook: The market exhibits modest concentration; leading firms control a meaningful share but room exists for bolt-on acquisitions that add technology, regional footprint, or certified product lines. Strategic buyers should prioritise assets that deliver IP (programmable timing, ruggedization), compliance certificates, or local manufacturing licenses.

Competitive landscape — focused profiles and what they signal

Our competitive analysis covers global incumbents and regional specialists. The landscape is shaped by product differentiation (electronic vs. electric vs. non-electric initiation), regulatory credentials, and recent capital moves that signal strategic intent.

Detonator Market

- Dyno Nobel — a leader in industrial mining initiation systems — has invested in plant automation and energy resilience. Recent facility upgrades and renewable-energy integration indicate a push to lower operating cost per unit and improve continuity of supply for high-value electronic detonator lines.

- Orica Limited — a technology-led supplier, driving lead-free electronic solutions into regulated markets. Certification wins for lead-free systems reposition Orica for contracts where environmental compliance is a mandatory precondition.

- Austin Powder Company — combines traditional product depth with electronic offerings. Their product strategy highlights differentiated electronic timing systems designed for industrial blasting environments where integration with blast design software is a decision factor.

- MAXAM and Enaex — both demonstrate how legacy explosives firms shift toward programmable and non-electric solutions to defend large mining accounts while expanding regional manufacturing and service capabilities.

- Chemring and Excelitas Technologies — represent the defense- and aerospace-focused edge of the market, where qualification to military standards and precision initiation technologies create a distinct, higher-margin sub-market.

- BME Mining Canada and regional manufacturers — strategically opening local production to de-risk supply chains for nearby mines; these moves create negotiating leverage for domestic buyers and shorten lead times.

- Nelson Brothers, Kırlıoğlu, Ideal Mining Services, Teledyne — a mix of specialized electronics, regional manufacturing scale, and unique technologies (e.g., exploding-foil initiators) that supply niche and contract-driven demand.

Recent events that shape 2026 tactics

- Plant and capacity initiatives — multiple manufacturers have announced new or upgraded facilities focused on electronic detonator production and automation, signaling faster ramp capability and reduced supply fragility.

- Certification and compliance — lead-free product certifications and military qualifications are enabling access to previously closed tender pools and altering procurement shortlists.

- Energy and sustainability investments — operators integrating renewables at manufacturing sites to reduce cost volatility and improve ESG profiles, which increasingly matter to investors and public-sector buyers.

Report contents — what PW Consulting delivers to decision-makers

The full Detonator Market study is built to be directly operational for executives, procurement leads, and M&A teams. Highlights include:

- Robust market-sizing model (base-year 2025, historical 2020–2025, forecast 2026–2032) with sensitivity scenarios for commodity price shocks and regulatory acceleration.

- Adoption curves for programmable electronic systems vs legacy offerings, with payer mix and contract-structure guidance.

- Practical supplier due-diligence templates that incorporate certification checkpoints, capacity ramp timelines, and supply-chain continuity metrics.

- Capex decision tools and ROI calculators for factory automation, renewable energy retrofits, and localized assembly.

- Competitive benchmarking and supplier scorecards tied to commercial negotiation playbooks.

- Regulatory impact assessment and mitigation checklists for lead-free transitions and defense-related qualification requirements.

- Scenario-based M&A playbooks highlighting target profiles, valuation sensitivities, and integration-risk heatmaps.

Risk matrix and scenarios for 2026

We model three pragmatic scenarios in the report: a baseline consistent with the published CAGR, an accelerated-adoption scenario driven by rapid regulatory tightening and mining capex, and a downside scenario from prolonged raw-material dislocations or export controls. Key risks include specialized labor shortages for electronic assembly, certification delays, and commodity-driven cost shocks. Offense and defense actions are prescribed for each risk vector — from dual-sourcing strategies and contract hedges to rapid certification partnerships and targeted capex phasing.

Go-to-market and procurement playbook — a practical checklist

- Prioritise suppliers with certified lead-free offerings for regulated tenders.

- Negotiate capacity reservation clauses and tiered pricing tied to volume and certification timelines.

- Invest in local assembly or partner with regional manufacturers to shorten lead times and reduce customs exposure.

- Embed performance-based contracts that align supplier incentives with blast outcomes and safety metrics.

Conclusion — the tactical ask for 2026

The detonator market’s steady top-line growth masks a strategic battleground: sustainability and certification, automation and localization, and technology differentiation. For leaders making 2026 decisions, the imperative is twofold — protect operations by de-risking supply and invest selectively in technologies and local capacity that will define competitive advantage in the next cycle. PW Consulting’s full report supplies the granular segmentation, pricing curves, supplier-level metrics, and downloadable decision tools required to turn these strategic priorities into executable plans.

Next steps

This preview is deliberately high-level to preserve the commercial sensitivity of granular segment and supplier figures. For the full dataset, scenario models, and tailored advisory offers (including workshop facilitation and bespoke valuation work), access the full Detonator Market report on our web portal or contact PW Consulting to schedule a strategy briefing.

For detailed analysis of this topic, please visit the official page:Detonator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com