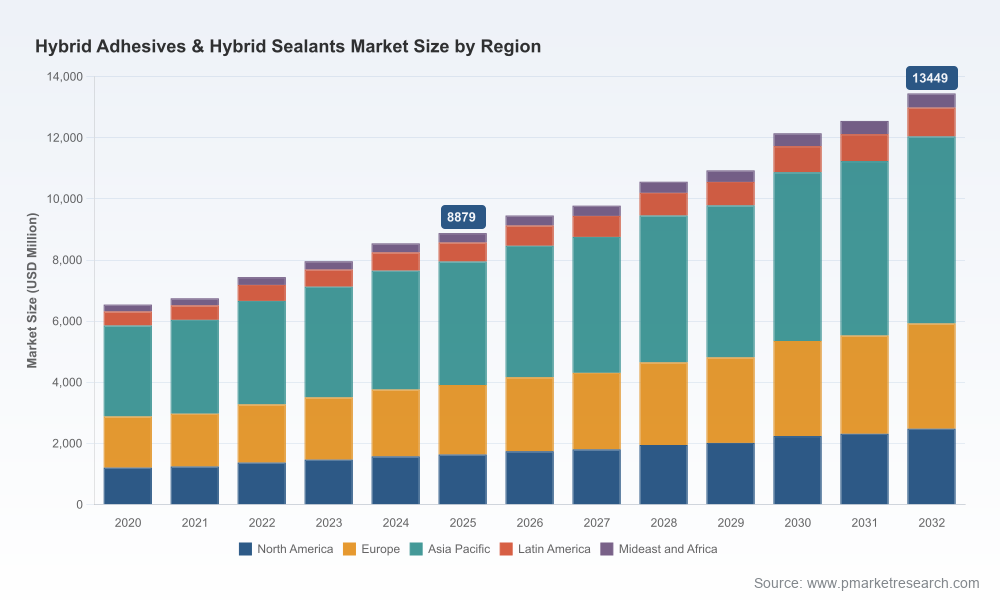

Hybrid Adhesives & Hybrid Sealants Market — Strategic Preview for 2026 Decision-Makers

PW Consulting’s latest market research on Hybrid Adhesives & Hybrid Sealants positions this sector as a resilient, innovation-driven segment of the broader adhesive and sealant industry. Anchored on a 2025 base year and a detailed historical review (2020–2025), our forward-looking model projects continued expansion through a 2026–2032 forecast window at a compound annual growth rate (CAGR) of 6.12%. The market has grown materially from the mid‑2020s and, by our baseline, is expected to move into a larger scale by the end of the forecast horizon — a dynamic that elevates strategic choices for manufacturers, raw-material suppliers, OEMs, and private-equity investors in 2026.

Hybrid Adhesives & Hybrid Sealants Market

Why this study matters for 2026 strategic planning

- Timing of inflection: Post‑pandemic recovery and structural demand drivers (construction modernization, automotive electrification, electronics miniaturization) are converging in 2026. This creates a narrow window for value capture before competitive and raw-material pressures intensify.

- Price, margin and sourcing volatility: Recent raw-material shocks — pronounced silicone and silane cost inflation and trade restrictions — are altering cost curves. Our analysis quantifies the profit sensitivity of common hybrid formulations and maps procurement levers that preserve margin without sacrificing performance.

- Product-and-channel differentiation: Low‑VOC and sustainability credentials, EV battery assembly suitability, and hybrid formulations that combine elasticity with structural strength are becoming minimum viable features for winning OEM contracts in 2026.

- M&A and partnership timing: With the market concentration metrics indicating top-tier firms controlling a meaningful but not overwhelming share of supply, 2026 is fertile ground for bolt‑on acquisitions, regional facility investments, or upstream tie‑ups that secure feedstock access.

Macro trajectory — what the headline numbers tell you (without the granular caveats)

Using 2025 as the base year, the global hybrid adhesives & hybrid sealants market exhibits a clear growth trajectory into the next decade. Our projections show continued expansion through 2032 at a 6.12% CAGR for the forecast period, reflecting both volume growth and value‑accretive premiumization (formulation upgrades and sustainability premiums). These headline dynamics create a strategic imperative: convert product and commercial innovation into scale before input-cost cycles or regulatory changes erode the margin pool.

Hybrid Adhesives & Hybrid Sealants Market

Report scope — practical, decision-ready deliverables

This study is designed as an operator’s playbook, not an academic survey. Core deliverables include:

Hybrid Adhesives & Hybrid Sealants Market

- Detailed market sizing and a robust forward model (2026–2032) with scenario toggles for raw-material price spikes and tariff regimes.

- Competitive landscape maps and capability matrices for leading suppliers, highlighting product portfolios, process expertise, distribution structures, and innovation pipelines.

- Supply‑chain risk heatmaps and procurement playbooks that quantify the effectiveness of hedging, vertical integration, and dual‑sourcing strategies specific to key feedstocks.

- Commercial go‑to‑market playbooks for OEM channels (construction, transportation, electronics) including sample pricing ladders, margin sensitivity analyses, and GTM roadmaps by customer archetype.

- R&D and product roadmaps, including formulation prioritization (e.g., low‑VOC, high‑temperature, EV‑grade adhesives), time‑to‑market estimates, and regulatory compliance checklists.

- M&A screening tools and a shortlist of strategic targets by capability and geostrategic fit (accretive capacity, specialty chemistries, distribution reach).

Competition snapshot — capabilities and strategic postures

The market is occupied by a mix of global chemical majors, specialized formulators, and regional players. Prominent global names operate with distinct strategic plays:

- Henkel AG & Co. KGaA — Leans on strong brand equity (Loctite, Teroson) and application engineering, pushing next‑gen MS polymer hybrids with an emphasis on automotive display bonding and sustainability features. Their recent new‑product introductions underscore a high‑R&D, customer‑centric approach.

- Sika AG — Deep penetration in construction and industrial waterproofing with product lines optimized for on‑site performance and logistics efficiency. Sika’s strength is application know‑how and channel reach.

- 3M Company — Focuses on hybrid adhesive‑sealant systems that combine material science with integration into industrial assembly processes. 3M’s differentiator is systems thinking — adhesives as part of an engineered interface.

- Dow Inc. — Plays to electrification and industrial bonding opportunities, with targeted development for EV battery assembly and high‑reliability joints.

- H.B. Fuller, Bostik, Wacker, RPM, Soudal and other specialist players — These firms combine niche chemistry, localized manufacturing, and channel intimacy. Wacker’s recent capacity investments reflect upstream integration moves; Bostik and H.B. Fuller continue to execute on application‑driven innovations.

- Smaller specialists and regional players — Provide agility in specialty formulations and local customer support; they are potential tuck‑ins for larger players seeking speed to market.

Market concentration is meaningful but not prohibitive: the top three and top five suppliers capture a significant portion of demand, leaving space for successful challengers that combine differentiated technology with targeted commercial execution.

Dynamics reshaping supplier economics in 2026

- Raw-material tightness & price shocks: Recent industry events — including material suppliers announcing sizable price increases and capacity ramps — have materially shifted cost assumptions for formulations. Elevated silane prices, selective tariffs, and spikes in catalyst costs are examples that compress margin unless passed through or mitigated by formulation changes.

- Trade and tariff risk: Duty barriers on specific feedstocks are forcing producers to reassess sourcing footprints and inventory strategies. Our scenarios quantify the cross‑border arbitrage threshold where regional production becomes superior to export economics.

- Product premiumization: Demand for low‑VOC, high‑durability, and EV‑compatible hybrids supports price premiums and faster adoption of higher‑margin SKUs; but adoption timing varies by channel and geographies.

- Regulatory trajectory: Emissions and chemical reporting requirements are tightening in key markets; compliance readiness can be a competitive advantage in tender processes.

Strategic playbook for 2026 — recommended actions

- Short‑term (0–12 months): Lock critical feedstock through forward contracts and strategic stockpiles; prioritize customer segments where higher margins offset raw‑material inflation; accelerate launch of low‑VOC SKUs that meet imminent regulatory tests.

- Medium‑term (12–36 months): Invest selectively in regional production capacity to de‑risk tariff exposure and shorten lead times; pursue bolt‑on M&A to acquire specialized polymers or distribution networks; formalize ODM/OEM co‑development agreements for EV and electronics subsegments.

- Long‑term (36+ months): Build integrated R&D pipelines targeting next‑generation chemistries (bio‑based silanes, catalyst‑light systems) and consider upstream partnerships with silicone and silane producers to secure preferential access or co‑investment opportunities.

Risk scenarios and contingency triggers

Our scenario bank models three high‑impact events (pronounced raw‑material price surge, accelerated regulatory tightening, and a competitor’s disruptive product launch). For each, the report prescribes specific trigger points and a graded response matrix — for example, a 20% feedstock price increase triggers a predefined mix of passing through partial costs, accelerating premium SKU rollouts, and initiating supply‑side diversification.

Methodology & credibility

The study synthesizes primary interviews with manufacturing and procurement executives, proprietary pricing elasticity models, plant‑level cost build‑ups, and a bottom‑up market sizing that reconciles demand drivers across construction, transportation, electronics and other industrial uses. We validate forecasts against historical shipment and revenue trends for 2020–2025 and stress‑test them under alternative macroeconomic and input‑cost assumptions.

Recent market signals you cannot ignore

- Upstream production investments: Recent starts of hybrid polymer production indicate supplier commitment to capacity expansion and an intent to capture higher‑value hybrid blends—this changes bargaining dynamics in select regions.

- Product innovation cycle acceleration: Leading formulators are shipping next‑gen MS polymer and other hybrid variants optimized for EV and display assembly—moves that push adoption curves and require competitive responses.

- Raw‑material volatility persists: Public announcements of price hikes and the lingering impact of tariffs on critical feedstocks mean procurement strategy must be elevated to a board‑level topic in 2026.

What we withhold — and why

To preserve the integrity of our commercial instrumentation and to ensure this preview functions as a decision trigger, this article deliberately omits the granular segmentation outputs (region‑by‑region shares, application splits and unit pricing ladders) that are included in the full report. Those detailed datasets — which underpin procurement stress tests, customer‑level margin models, and target lists for acquisition — are available through the PW Consulting client portal and the public report page.

Next steps for 2026 leaders

- If you are a manufacturer: prioritize immediate actions on feedstock risk mitigation and accelerate premium product commercialization plans.

- If you are an OEM: re‑evaluate your approved‑supplier list with an eye to hybrid formulations tailored for electrification and display assembly; demand detailed cost transpositions from suppliers.

- If you are an investor or acquirer: use the report’s M&A screening and synergy calculators to identify targets that close capability or geographic gaps before competitors do.

PW Consulting’s full Hybrid Adhesives & Hybrid Sealants Market study provides the datasets, playbooks, and transaction tools necessary to convert the 2026 market inflection into durable advantage. For access to the complete report, granular forecasts, and bespoke advisory engagements, please visit our report page or contact your PW Consulting lead.

For detailed analysis of this topic, please visit the official page:Hybrid Adhesives & Hybrid Sealants Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com