Video Editing Software Market 2026: Strategic Preview for Executive Decision-Makers

Introduction — Why this preview matters for 2026 strategies

As video transitions from a marketing tactic to a ubiquitous communications medium, the software that enables editing, post-production and distribution has become a strategic asset across industries. This preview—prepared by PW Consulting’s senior industry analysts—summarizes the essential strategic takeaways from our full Video Editing Software Market study (base year 2025, historical window 2020–2025, forecast 2026–2032). It is designed to equip CXOs, product leaders and corporate development teams with a concise, actionable orientation to shape investments, partnerships and market-entry plays in 2026. The full report contains the granular segmentation, vendor scorecards, financial models and playbooks that underpin the recommendations below.

Video Editing Software Market

Market snapshot: trajectory and structure

The market has shown steady expansion through the past half-decade, growing from a modest market size in 2020 to a substantially larger base in 2025 (reported in USD, revenue unit: Million). From that 2025 base, our model forecasts the market to continue expanding at a compound annual growth rate (CAGR) of approximately 5.6% over the 2026–2032 forecast horizon. By 2032 the market is expected to be materially larger than today’s base, reflecting continued adoption across creator economies, enterprise video workflows, and broadcast/post-production modernization.

Video Editing Software Market

Importantly, the market is neither fragmented nor monopolistic: the top three vendors capture just over half of overall revenues, while the top five account for close to two-thirds. That concentration profile creates dual strategic dynamics—dominant platforms set technical and commercial norms, while a second tier of nimble suppliers exploit specialization and niche workflows to grow share.

Video Editing Software Market

What this means for corporate strategy in 2026

- Prioritize platform interoperability and AI acceleration: With hardware vendors and cloud providers pushing accelerated AI inference for video workflows, investors and in-house product teams must plan integrations that reduce friction for GPU-accelerated editing, automated asset tagging and generative content augmentation. Partnerships with infrastructure vendors and careful benchmarking of AI throughput are table stakes.

- Distinguish between creator-first and enterprise-grade pathways: Market demand bifurcates between intuitive, lower-cost editing for broad creator communities and high-margin, feature-rich suites for broadcast/post-production. Market participants should map product roadmaps and go-to-market models to one of these poles (or define a credible play for a hybrid positioning) rather than stretching resources across both without clear differentiation.

- Reframe pricing strategy around recurring value: The shift to subscription and blended monetization models continues. For incumbents with installed bases that include perpetual licenses, consider hybrid offers that combine one-time purchase options with add-on subscriptions for AI features, cloud collaboration, or premium codecs. For new entrants, subscription-first with clear time-to-value metrics reduces churn risk.

- Invest in workflow integrations and collaboration: Remote production, cloud editing and distributed review cycles are driving demand for collaborative editing features and asset management. Vendors and adopters should focus on low-latency proxy workflows, version control for timelines, and secure link-based review systems that integrate with MAM and DAM platforms.

- Targeted M&A and vertical plays: Given the market concentration, strategic acquisitions of specialized tooling (VFX, real-time rendering, cloud transcoding) can accelerate capability-building faster than organic development. Corporates should prioritize tuck-ins that close clear functional gaps and deliver customer retention synergies.

Operational priorities for product, engineering and GTM teams

- Benchmark AI feature economics: Implement internal scorecards to quantify user value from AI features—time saved, quality uplift, and changes in engagement—rather than chasing feature parity alone. This will inform pricing and packaging decisions.

- Optimize for multi-modal content lifecycles: Support multi-resolution proxies, metadata-first pipelines and standards-based interchange formats. These investments reduce friction in distributed editorial environments and increase stickiness for enterprise customers.

- Design for discovery and education: Certification programs and learning pathways materially affect adoption among professional users. Vendor and partner certification costs and requirements are becoming part of procurement considerations; designing accessible learning and certification options can be a differentiator.

- Monitor regulatory and standards drift: From content provenance to AI-output disclosure, emerging regulatory expectations will influence feature design and compliance workflows—anticipate these shifts in product roadmaps.

Report contents — practical playbooks and tools included

Our full study is intentionally action-oriented. It contains:

- Executive decks and one-page memos customized for board and investor briefings.

- Financial models and scenario analyses (2026–2032) that allow users to stress-test price, feature and adoption curves against the 5.6% CAGR baseline.

- Vendor scorecards and feature matrices covering editing, color, VFX, audio post, collaboration and AI capabilities—designed for procurement and RFP shortlisting.

- Go-to-market playbooks for market entry, product-led growth and channel distribution (including partner profiles and channel economics).

- Use-case blueprints for enterprise verticals (education, corporate communications, media & entertainment, and creative agencies) with sample ROI calculations and deployment checklists.

- M&A screening criteria, deal valuation comparables and integration roadmaps for rapid capability acquisition.

- A technical appendix describing test harnesses, benchmark methodology and data sources so clients can replicate or extend our analysis.

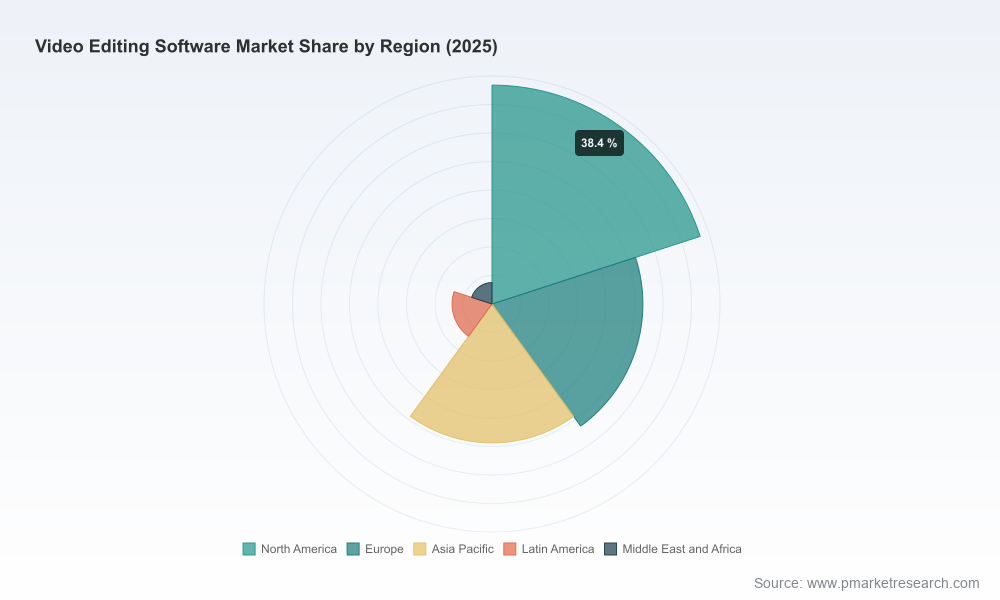

Note: In keeping with our “trailer” approach, this preview omits the detailed sub-segment tables and regional splits present in the full report. Those granular datasets and interactive dashboards are available via the source portal.

Competitive landscape — positioning and tactical moves

The competitive topology combines large platform incumbents, ecosystem specialists and agile challengers. Key companies profiled in the report include Adobe, Apple, Blackmagic Design, Avid, Corel, Sony, Wondershare, CyberLink, TechSmith and Magix. Each occupies a distinct space along the axes of professional feature depth, ease-of-use, pricing model and ecosystem lock-in.

- Adobe Inc. remains the reference professional platform, leveraging deep integrations across creative cloud assets and expanding generative/AI automation. Its strategic advantage is the embedded ecosystem and enterprise licensing relationships; its challenge is balancing innovation with perceived subscription fatigue among some customer segments.

- Apple Inc. nails an optimized, high-performance experience within its hardware-software ecosystem and is pursuing hybrid monetization with recent moves to subscription offerings for creator tools. Its strength is platform optimization; its limitation is naturally narrower hardware reach.

- Blackmagic Design continues to consolidate editing, color grading, VFX and audio in a single suite and has pushed significant AI and content discovery features in recent releases—appealing to both independent professionals and high-end post houses.

- Avid Technology holds strong enterprise and broadcast credentials with media asset management and collaborative workflows; it is the go-to for regulated broadcast pipelines where provenance, security and scale matter.

- Mid-market and consumer-oriented vendors such as Wondershare, CyberLink, Corel and Magix compete on ease-of-use, lower price points and rapid feature iteration—important feeders into the professional segment and valuable for volume-based monetization.

Recent platform and ecosystem developments are accelerating competitive dynamics. Hardware and AI vendors demonstrated accelerated workflows and generative features at industry shows, while major editing suites released AI-driven automation and collaborative capabilities in late 2025. These moves raise the bar for performance and automation as competitive differentiators in 2026.

Market dynamics and regulatory context

Several non-product factors are shaping adoption pathways:

- Certifications and professionalization: Vendor-sponsored certification programs are evolving from marketing badges to procurement considerations for enterprise buyers. Certification requirements and fees—now benchmarked across several vendors—affect training budgets and talent pipelines in client organizations.

- AI governance and content provenance: As generative features become commonplace, buyers increasingly demand traceability for AI-assisted edits and clear metadata trails for provenance and rights management. Product teams must architect compliance hooks early to avoid costly retrofits.

- Infrastructure shifting to edge-cloud hybrids: Real-time collaboration and low-latency review cycles are incentivizing hybrid edge-cloud deployment. Vendors that offer flexible deployment options and predictable operational economics will have an advantage.

- Standards and interoperability pressures: Cross-vendor interchange formats and APIs are becoming decisive purchasing criteria for enterprise customers who must integrate editing tools into wider media supply chains.

How to use this preview — next steps

- For investors: use the report’s financial scenarios to prioritize targets that demonstrate clear SaaS migration pathways, AI-driven differentiation, and enterprise revenue stickiness.

- For product leaders: adopt the report’s benchmarking templates to audit your product roadmap against demonstrated time-to-value metrics and AI throughput targets.

- For corporate development teams: apply the M&A screening checklist to triage acquisition targets that close capability gaps within 12 months.

Final note — what’s behind the curtain

This executive preview distills the strategic implications of our comprehensive Video Editing Software Market report. It highlights the market’s overall growth trends (historical and forecast), structural concentration, vendor positioning and the operational levers that will matter most in 2026. To access the full data tables, regional and application segmentation, vendor benchmarking matrices and downloadable financial models that informed these conclusions, please consult the full report on our portal. The detailed sub-segment intelligence is intentionally retained in the primary product to preserve the integrity and utility of the analysis for subscribers and clients.

PW Consulting stands ready to brief your leadership team on targeted implications for your business and to execute tailored deep dives—ranging from technical due diligence to 100-day integration plans—derived from the study’s proprietary datasets.

For detailed analysis of this topic, please visit the official page:Video Editing Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com