US Cast Polypropylene Packaging Films Market: Meeting High-Performance Food and Medical Barrier Requirements

Other |

2026-06-24 13:57:10

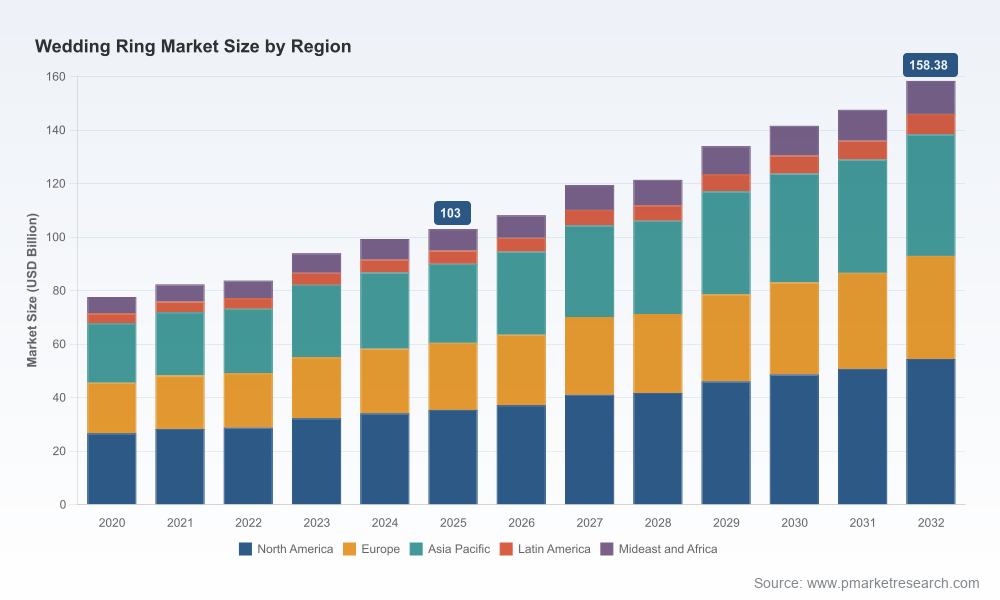

PW Consulting’s 2026 Wedding Ring Market study (base year 2025; historical 2020–2025; forecast 2026–2032) provides a decision-quality view of a market that has returned to robust expansion after pandemic-era disruption. At a macro level, the global market exceeds USD 100 Billion in 2025 and is modeled to grow at a compound annual growth rate (CAGR) of approximately 6.5% across the 2026–2032 forecast window, driving the sector toward a materially larger opportunity by 2032. Market concentration is meaningful — the top three and top five suppliers account for a dominant share of industry revenues — a structural feature that shapes competition, margins, and M&A dynamics going into 2026.

Wedding Ring Market

Capital allocation and product strategy: The report converts headline growth into investable opportunities — identifying where premiumization, personalization, and channel mix will deliver the fastest returns on new product development and inventory commitments.

Wedding Ring Market

Supply chain and raw-material risk management: With raw-material price volatility and evolving ethical sourcing regulations, the study maps exposure and presents mitigation pathways (hedging, strategic sourcing agreements, and vertical partnerships).

Wedding Ring Market

Channel optimization and digital transformation: We translate shifting consumer behavior into concrete omnichannel roadmaps that protect margins while scaling online acquisition and experiential in-store conversion.

M&A and partnership playbook: For buyers and sellers, the report provides transaction-ready diagnostics — concentration metrics, target archetypes, and integration risk profiles tailored to 2026 market realities.

The wedding ring market’s growth is not uniform; it is being pulled by several concurrent forces. Demographic cohorts entering marriageable age, premiumization of ceremonies, and a persistent appetite for personalized product formats (customizable and stackable designs) underpin structural demand. At the same time, raw-material dynamics are a major near-term friction: record-high gold prices in 2025 have tightened gross margins for conventional formulations and accelerated supplier re-negotiations and design innovation to preserve price-value for consumers. Parallel to input-cost pressure, regulation and consumer scrutiny around ethical sourcing are not peripheral: sustainability commitments and responsibly mined materials have moved from brand differentiator to table-stakes in many developed markets.

On channels, physical retail remains a crucial conversion venue for high-consideration purchases, while online platforms are expanding reach and enabling new business models (direct-to-consumer, virtual try-on, and pre-configured customization). The combined effect over the forecast window is a market that grows in headline size but becomes more complex to manage operationally — winners will be those who align assortment, pricing, and distribution with evolving consumer journeys without surrendering margin integrity.

How should you rebalance assortment between legacy precious-metal designs and alternative materials that reduce cost exposure while preserving perceived value?

What is the optimal channel mix across digital, wholesale, and experiential retail to maximize lifetime value and minimize inventory write-offs?

Which operating model — vertically integrated manufacturing vs. asset-light sourcing — delivers the best trade-off between margin control and agility in a volatile raw-material environment?

Where should M&A capital be allocated: scale-accretive retail roll-ups, vertical capabilities (manufacturing/finishing), or digital-native brands with high-margin direct channels?

Our study is structured as a working toolkit for strategy teams, commercial leaders and investors. Highlights include:

Proprietary market-sizing and forecasting models (2020–2032) with scenario analysis and sensitivity to raw-material price paths and channel-shift scenarios.

Go-to-market playbooks for incumbents and challengers: pricing architecture, assortment rationalization, and omnichannel conversion frameworks.

Supply chain stress-tests and mitigation templates: supplier risk scoring, hedging playbooks, and nearshoring vs. outsourcing decision matrices.

Commercial diligence checklists for M&A and JV activity, including integration readiness, margin leverage assumptions, and revenue-synergy blueprints.

Consumer-behavioral segmentation and journey maps that translate trend signals into product and marketing priorities (note: full segmentation tables and market splits are available in the complete report).

Regulatory and ESG roadmap: compliance triggers, audit protocols, and supplier engagement strategies tailored to jewelry value chains.

The competitive field is characterized by a mix of heritage manufacturers, digitally-native ethical brands, specialty performance jewelers, and wholesale producers. The sector’s concentration (top-three and top-five metrics noted earlier) indicates that scale and brand equity still confer considerable advantage, particularly in premium segments.

Artcarved (New York, USA; https://artcarvedbridal.com/): Long-established manufacturer with deep expertise in carved and comfort-fit bands. Their heritage craftsmanship is an asset in service-driven retail environments; for incumbents, Artcarved-style capabilities suggest paths to product differentiation through fit engineering and design depth.

Brilliant Earth (San Francisco, USA; https://www.brilliantearth.com/): A high-profile exemplar of ethics-led positioning and vertical direct-to-consumer execution. Their emphasis on responsibly sourced materials and transparent supply chains offers a playbook for converting ESG commitments into consumer willingness-to-pay.

Tacori (California, USA; https://www.tacori.com/): A premium, American-made customizer of engagement and wedding rings. Tacori highlights the margin and loyalty benefits of customization at scale and the premium achievable through “made-in” narratives.

Whiteflash (New York, USA; https://www.whiteflash.com/): Focused on performance metrics (e.g., cut quality, light return) to command premium pricing — a reminder that technical differentiation (not just raw-material storytelling) can underpin pricing power.

Shane Co. (Minneapolis, USA; https://www.shaneco.com/): A family-owned omni-channel retailer with integrated inventory and local footprint advantages — instructive for players balancing experiential retail investments with online scale.

JewelPin (USA; https://www.jewelpin.com/): A global manufacturer and wholesaler of ready-to-ship rings. Their model underscores the continuing strategic importance of wholesale and B2B channels to absorb demand variability and optimize unit economics.

Across these profiles, several common strategic levers emerge: brand differentiation (heritage vs. ethics vs. technical performance), channel choreography (how to pair physical touchpoints with digital acquisition), and supply-side control (manufacturing and sourcing). The full report includes comparative capability matrices and go-to-market scenarios for each archetype.

Key downside scenarios assessed in the study include severe raw-material price spikes, accelerated channel cannibalization as online penetration increases, and tightening regulatory requirements on sourcing disclosures. Recommended mitigations are pragmatic and staged: short-term hedging and supplier lock-ins to stabilize unit costs; medium-term product engineering to reduce precious-metal content without diluting perceived value; and long-term investments in traceability and brand storytelling to insulate pricing against ethical scrutiny.

Week 1–3: Rapid diagnostics — run our “50-question revenue & margin” checklist to identify the highest-impact levers in your P&L.

Month 1–2: Tactical moves — adjust assortment, pilot lower-cost material mixes, and deploy targeted digital acquisition tests in high-ROI cohorts.

Month 3–6: Strategic moves — negotiate multiyear supplier agreements, build a sustainability compliance program, and evaluate bolt-on acquisitions or partnerships using our transaction screen.

This introduction demonstrates the kind of actionable intelligence PW Consulting delivers: market-sizing grounded in transparent methodology, scenario-based forecasts that stress-test assumptions, and practical playbooks that link strategic choices to measurable financial outcomes. We intentionally keep detailed regional and material splits, and company-level metrics, in the full report to preserve the analytical narrative and provide you with the complete datasets and models needed to execute. For teams preparing budgets, negotiating supply contracts, or evaluating M&A in 2026, the full Wedding Ring Market study is the tool that converts market momentum into executable advantage.

Access the full report for the detailed segmentation, granular forecasts, downloadable financial models, and the ready-to-use commercial templates that will inform decisions across your organization.

For detailed analysis of this topic, please visit the official page:Wedding Ring Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com