The Rise of Industrial Safety Footwear Market Demand Surges

Other |

2026-06-22 11:13:40

As global electrification accelerates, the electrolyte—the often overlooked yet mission‑critical component in lithium‑ion cells—has migrated from a commodities corner to the center of strategic supply‑chain planning. PW Consulting’s latest market research synthesizes five years of historical dynamics and a seven‑year forecast to 2032, delivering the market context that senior executives, investors, and policy teams will need to make high‑stakes decisions in 2026.

Lithium Ion Battery Electrolyte Market

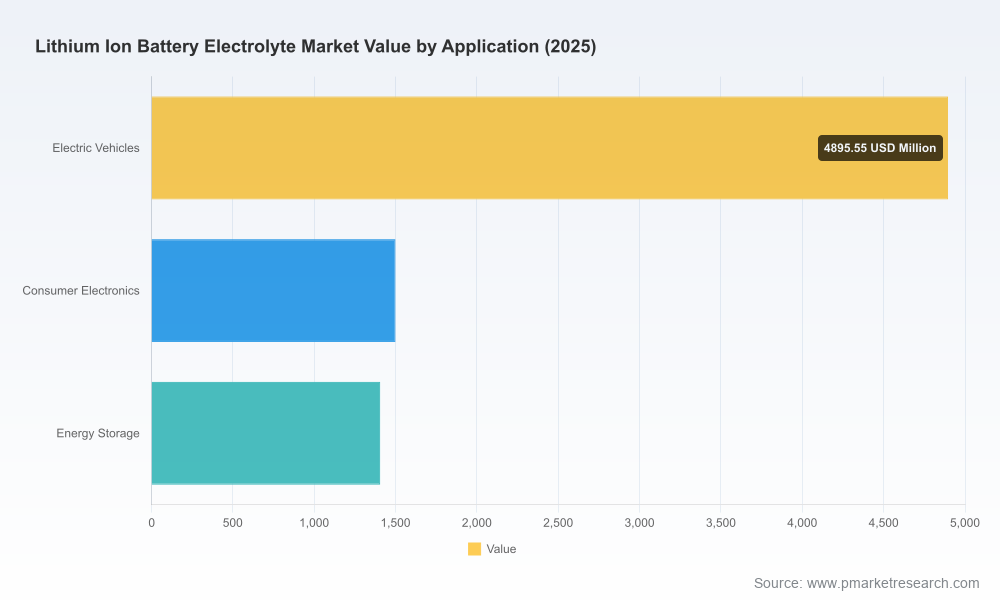

Macro momentum: The market nearly doubled from the start of the decade; our modelling shows growth from roughly USD 3.8 billion in 2020 to about USD 7.8 billion by the 2025 base year, and projects continued expansion into the early 2030s, with the market passing the USD 17 billion mark by 2032 under our central scenario. The forecasted mid‑late decade compound annual growth rate reflects a sustained, structurally driven upward trajectory.

Lithium Ion Battery Electrolyte Market

Risk density: Volatility in critical upstream inputs and a fracturing of legacy supply geographies mean that electrolyte strategy can no longer be an afterthought. Firms that treat electrolyte sourcing as a strategic lever—not merely a procurement line item—will secure competitively decisive advantages.

Lithium Ion Battery Electrolyte Market

Strategic inflection in 2026: Policy shifts (notably regional industrial incentives and content rules), recent capacity re‑allocations and M&A activity, and raw material price volatility create a narrow window in 2026 for decisive moves—capacity commitments, offtake deals, and targeted M&A—to lock in advantaged positions for the rest of the decade.

This is a working playbook for executives, combining market modelling with implementation-ready tools. Highlights include:

Robust market sizing and forward curves (historical 2020–2025 baseline; granular monthly and annual forecasting through 2032), with sensitivity bands to stress‑test alternative adoption, technology and regulatory pathways.

Supply‑demand modelling that integrates cell chemistry shifts, EV and ESS buildouts, and component‑level pass‑through mechanics—allowing you to link electrolyte demand to specific manufacturing ramps and battery chemistries.

Raw‑material cost modelling and hedging templates: scenario runs for major salts and solvent inputs, and decision frameworks for when to hedge, when to verticalize, and when to pursue secured long‑term contracts.

Competitive benchmarking and capability matrices: plant footprints, technology differentiators (e.g., purification processes, specialty additives), and strategic positioning across the value chain.

Regulatory and incentive playbooks: how to align capacity siting and product specifications with regional content rules and subsidy programmes to maximise qualifying volumes.

Transaction and partnership guidance: acquisition target profiles, due‑diligence scorecards, integration roadmaps and earn‑out structuring templates that reflect the unique technical and regulatory risks of electrolyte assets.

Risk heatmaps and mitigation plans: practical steps to reduce exposure to supply shocks, quality failures, and evolving ESG requirements across production and logistics.

The market sits in a moderately concentrated competitive structure: the top three and five suppliers control a material majority of reported commercial volumes. That concentration produces two practical realities for 2026 decision‑makers.

First, scale and technological differentiation matter. Large incumbent chemical groups and specialized electrolyte players command premium access to high‑purity production techniques and purification technologies that are increasingly table stakes for automotive and industrial battery customers.

Second, the consolidation of high‑capacity incumbents creates both entry barriers and M&A opportunities. For corporates seeking to secure supply, partnership or acquisition of regional assets is often more time‑efficient than greenfield build‑outs—but only when aligned with rigorous technical and regulatory due diligence.

Key company behaviours we profile in the report (and that will shape 2026 outcomes):

Strategic capacity plays by integrated chemical majors and specialist makers to service automotive battery programs and large energy‑storage projects;

Targeted downstream integrations—additive formulation and purification capabilities—by players seeking margin accretion and differentiated product portfolios;

Cross‑border asset consolidations and selective regional onshoring to meet content and subsidy rules.

Acquisitions and asset transactions: There has been active reshaping of the European and North American asset base through selective acquisitions of manufacturing facilities—moves that materially affect where qualifying electrolyte capacity will be available to cell makers and OEMs.

Large greenfield and brownfield investments: New plant ground‑breakings and capacity commitments in North America and elsewhere indicate a shift from just‑in‑time sourcing to strategic stockpiling and regional production, driven by regulatory incentives and supply‑security priorities.

Raw‑material volatility: Prices for principal electrolyte salts have exhibited meaningful upward and volatile swings over recent months, a pattern that has real P&L implications for both commodity and specialty electrolyte suppliers. Understanding and modelling those swings is a central, recurring module in the full report.

Project cancellations and rationalizations: The sector is pruning non‑viable large projects; a tighter project pipeline will affect medium‑term availability and bargaining dynamics.

Immediate (0–12 months): Secure flexible offtake agreements with escalation clauses linked to raw‑material indices; pursue minority stakes in regional producers to guarantee supply without bearing full greenfield risk; and initiate technical audits of preferred suppliers to verify purification metrics and quality controls.

Medium term (12–36 months): Prioritise investments into additive formulation and high‑purity processing capabilities, or structured partnerships that encode technology transfer. Where subsidy regimes reward regional production, synchronise capex decisions with incentive timelines and content compliance requirements.

Portfolio moves for investors: Target bolt‑on acquisitions that provide both technical differentiation and local market access; avoid scale‑only plays absent demonstrable quality or feedstock position. Build exit assumptions that account for regulatory resets and potential re‑rating of strategic assets.

We design our work to convert market intelligence into executable strategy. The report couples deterministic market projections with scenario planning and executable tools: supplier scorecards, capex prioritisation matrices, contract templates and a live M&A watchlist. Importantly, we omit granular public extraction of proprietary segment‑level and regional shares in this preview—those detailed splits, unit economics and facility‑level maps are part of the subscription report and the accompanying datasets available on the PW Consulting portal.

Electrolytes are no longer a fungible commodity line that buyers can source opportunistically. The interplay of demand acceleration, input volatility, regulatory reshaping and concentrated supply has turned electrolyte strategy into a lever for competitiveness across the battery value chain. Firms that move early in 2026—aligning capacity, offtake and technical capability—will convert forecast growth into durable advantage. Those that defer will face compressed choices and higher entry costs.

For those preparing board briefs, capital allocation proposals, or M&A strategies this year, our research provides the market shape, decision frameworks and operational toolkits you need to act with conviction. To access the full models, granular regional and application splits, facility maps, and the detailed competitor scorecards that we intentionally leave out of this preview, please consult the full PW Consulting Lithium‑Ion Battery Electrolyte Market report and datasets.

For detailed analysis of this topic, please visit the official page:Lithium Ion Battery Electrolyte Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com